Fact-checked and reviewed by MetaCounts.co, a Vancouver-based cryptocurrency accounting firm staffed by Chartered Professional Accountants (CPAs).

Crypto mining tax in Canada usually becomes a deductions question only after one bigger issue is settled first: are you actually carrying on a business. CRA’s current mining guidance says that, in most cases, mining activities will be considered a business because of the scale and resources involved. It also says that if you are in the business of mining, the value of the crypto-assets you receive for mining must be included in business income when it is earned.

That business-versus-personal split matters because the deduction rules do not start with electricity or hardware. They start with the nature of the activity. CRA’s mining tax tip says mining is taxed differently depending on whether it is a personal activity, often described as a hobby, or a business activity, and that this is decided case by case. If the activity is genuinely a business, the normal business-income and business-expense framework comes into play. If it is only personal, the path to claiming business deductions becomes much weaker.

This guide focuses on the core rule, the main deductions miners usually care about, the reporting route, and the one hardware point that CRA now states directly: ASIC miners and GPU rigs used in a mining business may qualify for capital cost allowance under Class 50.

Key takeaways

- CRA says that, in most cases, crypto mining activities will be considered a business because of the scale and resources involved.

- If you are mining as a business, the crypto you receive from mining must be included in business income when it is earned.

- Electricity and similar utility costs may be deductible if they were incurred to earn business income, but only the business portion is claimable.

- Mining rigs are usually not deducted all at once as a current expense. CRA says ASIC miners and GPU rigs used in a mining business may qualify for CCA under Class 50. The rate is 55%, but the first-year claim is generally reduced by the half-year rule.

- Business-account mining income and deductions generally flow through Form T2125.

- GST/HST has its own crypto-mining rules. In many cases, mining payments received after February 4, 2022 are deemed not to be a supply for GST/HST purposes, and miners are generally not eligible for input tax credits on related purchases, subject to limited exceptions.

Table of contents |

No credit card required

Business or hobby comes first

CRA’s public mining guidance does two things at once. First, it says mining can be a personal activity or a business and that the answer depends on the facts. Second, its more detailed mining and staking page says that, in most cases, mining activities will be considered a business because of the scale and resources involved. Read together, those two points tell you how CRA is approaching mining now: hobby treatment is still possible, but many real-world mining operations will be pushed toward business treatment.

That matters because the deduction discussion in this article assumes you are on the business side of the line. CRA’s T4002 business guide says income or losses from business activities involving crypto-assets, including mining, belong in business income. Once you are in that framework, you can start applying the normal rules for reasonable current expenses, capital cost allowance, and business-use-of-home costs where relevant.

For a small at-home miner, the practical question is not whether the setup feels casual. It is whether the activity has enough regularity, scale, and income-earning structure to support business treatment. CRA’s mining tax tip says business activity normally involves some regularity or repetitive process over time, and that one transaction can sometimes still be a business activity.

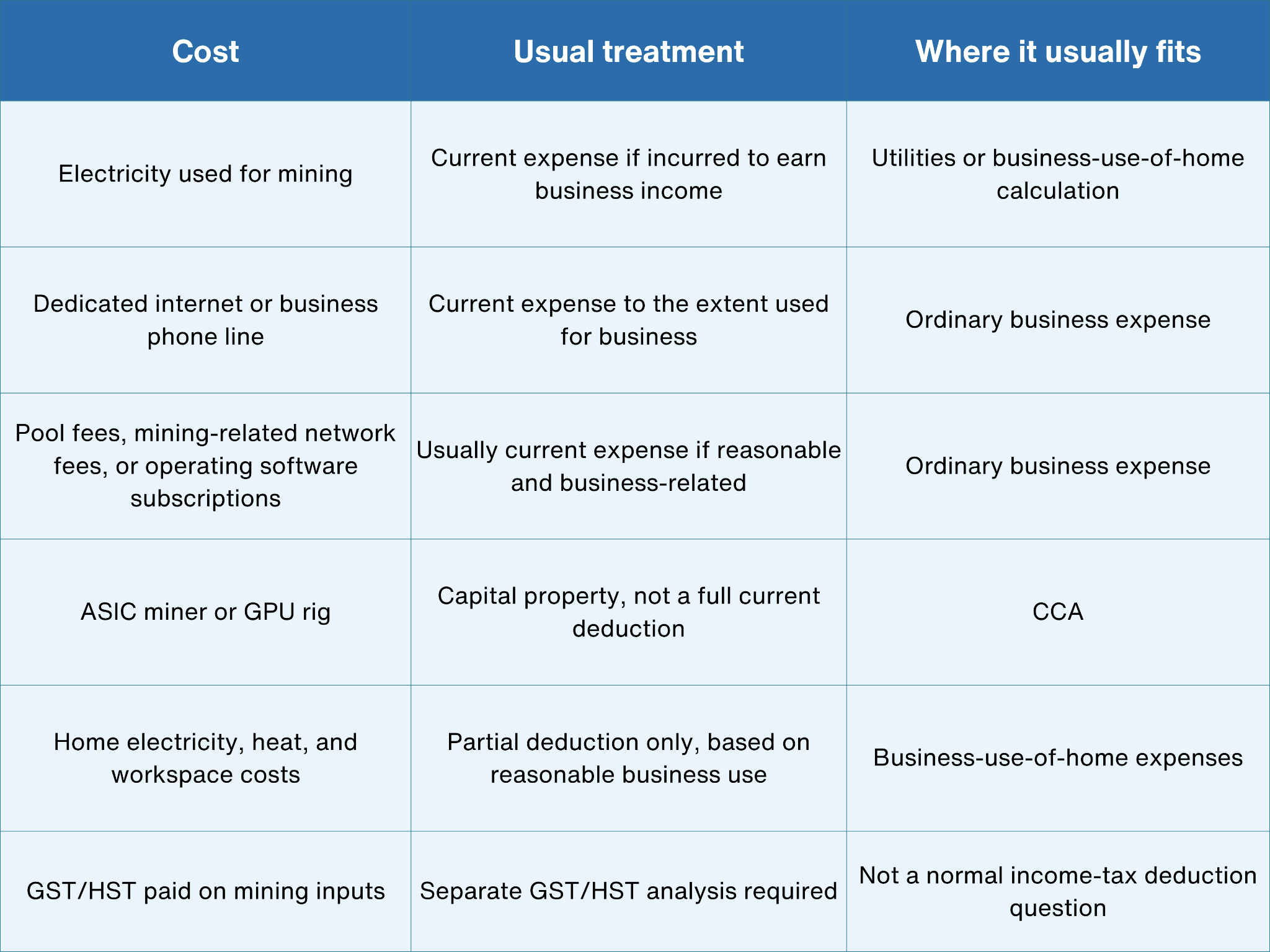

Which mining costs are usually deductible

If your mining is a business, CRA’s general rule is that you can deduct any reasonable current expense you incur to earn income, but you cannot deduct the cost of capital property as an ordinary current expense. That is the line that separates electricity from mining rigs. Electricity is usually a current expense. A mining machine is usually a capital asset.

This is the practical breakdown most miners need:

CRA’s utilities guidance says you can deduct expenses for utilities, including electricity, if you incurred them to earn income. If the mining is happening from home, CRA’s business-use-of-home guidance says you may deduct part of heating, electricity, insurance, maintenance, mortgage interest, property taxes, rent, and certain other costs using a reasonable basis, such as the workspace area divided by the total home area.

That is why “Can you deduct electricity for crypto mining in Canada?” is really two questions. If you operate a mining business, electricity is often one of the clearest deductible current expenses. But you still need to support the business-use portion. If you are mining from a room in your home, claiming one hundred percent of the household power bill is usually much harder to defend than claiming a documented business portion tied to the mining setup.

How CRA treats mining hardware

Mining hardware is where many taxpayers over-claim in the first year. CRA’s capital cost allowance guidance says you cannot deduct the cost of depreciable property all at once when calculating business income. Instead, you deduct the cost over time through CCA once the property is available for use.

CRA’s current mining and staking page now says this directly for crypto miners. If you own mining equipment such as ASIC miners or GPU rigs that you use in your crypto-mining business, you may be able to claim CCA for that equipment. CRA also says that ASIC miners and GPU rigs can meet the conditions to fall within CCA Class 50. Class 50 currently carries a fifty-five percent rate for qualifying general-purpose computer hardware and related systems software acquired after March eighteen, two thousand seven, if not included in another class.

That means the basic rule is straightforward:

- you do not deduct the full cost of the rig as a current business expense

- you place the qualifying equipment in the proper CCA class

- you claim CCA over time, subject to the normal rules such as the available-for-use rule and, in many cases, the half-year rule

CRA’s CCA guide says property usually becomes available for use when it is first used to earn income, when it is delivered and capable of producing a saleable product or service, or at certain other statutory points. It also says that, in the year you acquire depreciable property, you can usually claim CCA on only one-half of the net additions to the class because of the half-year rule.

This is one area where miners should resist the temptation to simplify too much. The “hardware depreciation” question is not just about whether the rig is deductible. It is about claiming it in the right way.

A simple mining example

Suppose you run a small Bitcoin mining operation from home and CRA’s facts support business treatment. During the year:

- you earn C$12,000 worth of mined crypto when it is earned

- you pay C$3,600 of electricity clearly tied to the mining setup

- you incur C$900 of pool fees and software costs

- you buy a new ASIC miner for C$8,000

On an income-tax view, the C$12,000 generally starts as business income from mining. The electricity and pool fees are the easier current expenses to analyze, assuming the business-use portion is properly supported. The ASIC miner is not usually deducted all at once. Instead, it generally goes into CCA treatment, with CRA’s mining page indicating that qualifying ASIC and GPU equipment can meet Class 50.

That example shows the core difference miners need to remember: electricity is usually about business-use support, while hardware is usually about capital cost allowance.

How to report crypto mining income in Canada

If the activity is a business, CRA’s T4002 guide says business income or losses from crypto mining belong in business income. For a sole proprietor, that usually means Form T2125, which is the form CRA uses to calculate business or professional income and expenses.

The reporting sequence is usually:

- include the value of mined crypto in business income when it is earned

- deduct reasonable current business expenses

- claim CCA separately for qualifying equipment

- keep clear records of valuation, expenses, and hardware purchases

CRA’s mining and staking page is explicit that, if you are in the business of crypto mining, the value of the crypto-assets you receive for mining must be included in business income at the time it is earned. That timing point matters because many miners only look at what they sold later and forget that the mining reward itself is already part of the income story.

The recordkeeping side is equally important. CRA’s general crypto valuation guidance says you must determine the value of crypto-assets when transactions occur, use a reasonable method, apply it consistently, and keep a record of how the value was established. For miners, that means documenting the Canadian-dollar value of block rewards and fees when earned, not just the later sale proceeds.

A short GST/HST note for miners

GST/HST is now its own separate issue for crypto mining. CRA’s current Notice 324 says that section 188.2 of the Excise Tax Act applies to mining activities in respect of cryptoassets. In many cases, where a person receives a mining payment for performing a mining activity, the provision of the mining activity is deemed not to be a supply for GST/HST purposes, so the person is not required to charge GST/HST on that mining activity.

The trade-off is that CRA also says the miner is generally not eligible to claim input tax credits for property or services acquired for use in those mining activities after February four, two thousand twenty-two, subject to limited exceptions. So for many miners, the GST/HST answer is no longer “charge GST and claim ITCs as normal.” It is a more specialized regime that should be checked separately from the income-tax deduction analysis.

Because your blog is mainly about deductions, the practical takeaway can stay simple: do not assume that an expense deductible for income-tax purposes also produces a normal GST/HST input tax credit result in crypto mining.

How cryptact helps

Crypto mining files usually become messy in three places: valuing mined coins when earned, separating current expenses from capital hardware costs, and keeping the later sale of mined coins from getting mixed up with the original mining income.

That is where cryptact helps in a practical way. It brings transaction history together, makes it easier to track when crypto was earned, and helps keep later dispositions organized against the original mining record. For miners dealing with electricity claims, hardware purchases, and later sales across multiple wallets or platforms, that structure makes CRA reporting much easier to prepare and much easier to defend.

Conclusion

A strong crypto mining tax Canada analysis starts with one issue before anything else: is this a business. CRA’s own guidance says that, in most cases, mining activities will be considered a business because of the scale and resources involved, and once that business framework applies, the rest of the deduction discussion becomes much easier to map. Electricity and similar operating costs are usually current expenses to the extent they were incurred to earn income. Mining rigs are usually capital property and generally belong in CCA, not in a one-year write-off.

The reporting route is also relatively clear once the facts are in order. Business-account mining income and expenses generally flow through T2125, while the mined crypto itself has to be valued when it is earned. That is where cryptact adds real value. It helps keep the income, expense, hardware, and later sale records organized enough that the final CRA reporting is much easier to manage.