Fact-checked and reviewed by Scott Lynch (Beanstalk Accountants), Chartered Accountant.

Crypto trading and investment have skyrocketed in popularity in recent years, bringing with them a crucial need to understand the tax implications.

If you’re involved in the Crypto market in Australia, navigating the tax landscape effectively is essential.

This comprehensive guide will explore the key aspects of Crypto taxation in Australia, ensuring you’re well-prepared to meet your tax obligations.

Key takeaways

- Both investors and traders pay tax on crypto in Australia, but investors are taxed under Capital Gains Tax while traders are taxed on business income.

- Crypto held for more than 12 months can qualify for the 50% CGT discount.

- Common taxable events include selling crypto, swapping one crypto for another, spending crypto, and earning crypto through mining or staking.

- The ATO runs a crypto data-matching program, so all crypto activity should be reported.

- Net capital gains are taxed at your individual income tax rate, and keeping accurate records (or using a tool like cryptact) makes filing easier.

No credit card required

Basic knowledge of tax for crypto

Understanding the tax implications of Crypto transactions is crucial for compliance and financial planning. This includes knowing whether crypto trading is legal, and how it is regulated.

Is crypto legal?

Yes. Crypto trading is not just popular but also perfectly legal in Australia. The Australian Taxation Office (ATO) has established clear guidelines to ensure transparency and fair practices in the world of digital assets.

How much and what tax do you pay?

For those investing in cryptocurrencies, it’s important to be aware that Capital Gains Tax (CGT) or income tax apply depending on transactions you made. When you report your gains and losses in your Income Tax Return, you will need to pay Income Tax on your net gains. If you hold an asset for over a year, you can benefit from a 50% CGT discount.

The good news is that Income Tax only applies once your total income exceeds $18,200 a year.

Can ATO track?

The ATO’s crypto assets data-matching program has sophisticated tracking capabilities for Crypto transactions, ensuring compliance with tax laws. This means it is vital to declare all Crypto-related activities in your tax return, especially if you have sold, traded, or earned crypto in the past financial years.

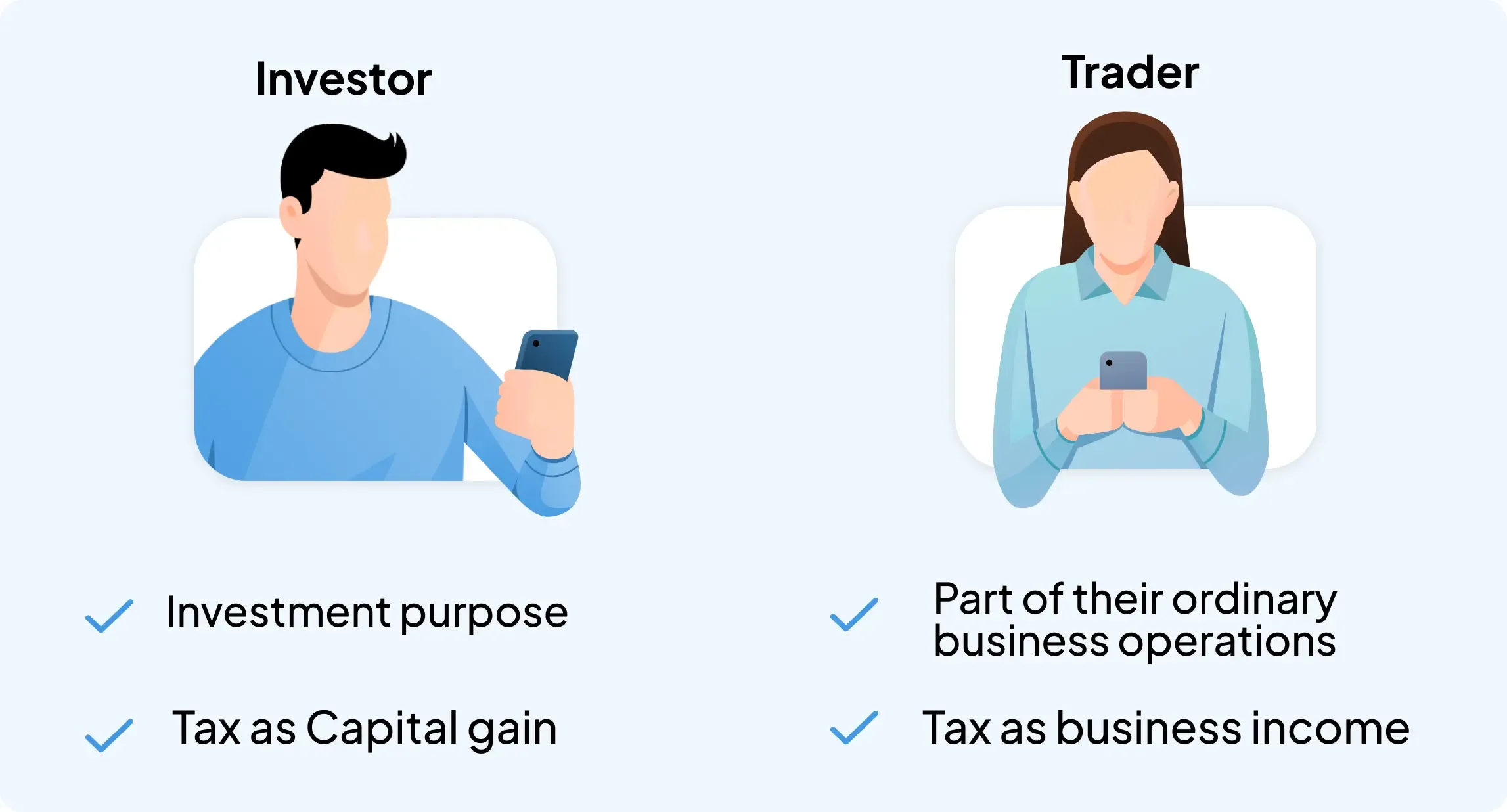

How Taxation Differs Between Traders and Investors

Understanding whether you are classified as a trader or an investor can significantly impact how your Crypto income is taxed. However, since there are no strict criteria for defining who is a trader, please use the following as a guideline.

Investors

Investors typically buy and hold digital assets for long-term gains. Their cryptocurrency income is taxed as capital gains, which can benefit from a 50% CGT discount if the assets are held for more than 12 months. This classification suits those who see cryptocurrency as a long-term investment.

Traders

Traders, on the other hand, engage in buying and selling cryptocurrency frequently, treating it as stock in trade. Their crypto income is taxed as business income, which may be subject to different rates and deductions. This classification is for those who approach cryptocurrency as a business.

Capital Gains Tax

Capital Gains Tax (CGT) is a significant component of cryptocurrency taxation in Australia.

The rate at which CGT is applied depends on your total income and the duration for which the asset was held. Assets held for more than 12 months qualify for a 50% CGT discount, providing a substantial tax advantage.

If you incur a capital loss, this can offset capital gains in the same financial year or be carried forward to future years, helping to reduce your overall tax liability.

In unfortunate cases where cryptocurrency is stolen or hacked, you might be able to claim a capital loss. However, you must provide sufficient evidence, and the event must meet specific criteria set by the ATO.

Taxable Events in Crypto (timing of the CGT event)

Several activities in the Crypto space trigger taxable events, which means they need to be reported for tax purposes.

Buying and selling cryptocurrency

Buying and selling cryptocurrency results in capital gains or losses. These transactions must be reported, whether you’re converting to fiat or another digital currency.

Swapping or exchanging of different cryptocurrencies

Frequent trading activities that result in you being declared a trader are considered business transactions and are taxed accordingly. This includes any swapping or exchanging of different cryptocurrencies.

Infrequent swapping or exchanging of one crypto for another that result in you being declared an investor are considered capital gains and are taxed accordingly.

Pay for goods and services

Using crypto to pay for goods and services is generally a taxable event. When you spend crypto, you are not taxed on the purchase of the good or service itself. You are taxed on the gain in value of the crypto you disposed of to make the payment.

There is one exception. If your crypto is a personal use asset, the capital gain may be exempt from CGT. Crypto is treated as a personal use asset when you acquire it and use it within a short period mainly to buy items for personal use or consumption, and it costs $10,000 or less to acquire. Crypto held as a longer term investment will not usually qualify, and any capital loss on a personal use asset is ignored.

Income generated from mining and staking

Income generated from mining and staking activities is also taxable and must be reported as income. This includes any rewards or earnings from these activities.

These activities are taxable events. The first three, buying and selling Crypto, swapping or exchanging different cryptocurrencies, and paying for goods and services, are considered capital gains. In contrast, income generated from mining and staking is classified as ordinary income. Those are just examples, so check out ATO announcements or ask your accountant if you have any other transaction types. There are more events in the Crypto space that trigger taxable events.

A few other common transactions are worth knowing about:

- Gifting crypto to another person is treated as a disposal and is subject to CGT.

- Moving crypto between wallets you own is not a taxable event, although a fee paid in crypto for the transfer counts as a disposal.

- Receiving an airdrop is usually taxed as ordinary income at its market value on the day you receive it. Initial allocation airdrops (issued before they are able to be traded) are an exception and are instead treated as a $0.00 purchase. CGT applies as normal when they are sold.

- DeFi activity, NFTs, and staking rewards can trigger either CGT or income tax depending on the transaction, so check the latest ATO guidance or ask your accountant.

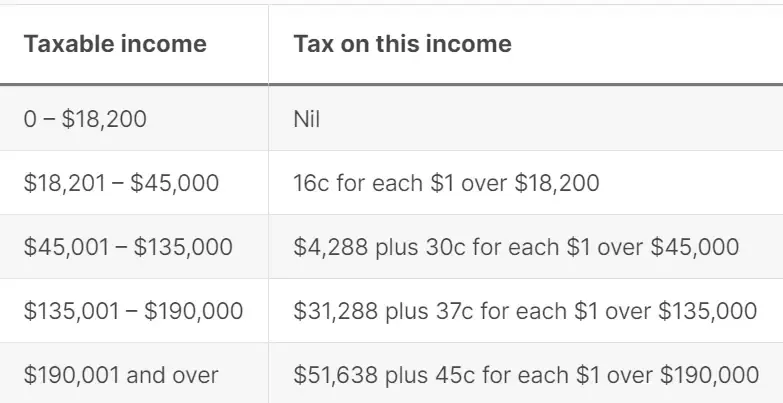

ATO individual income tax rate 2024-25 and 2025-26

In Australia, the net capital gains are taxed according to your Income Tax rate. This rate varies based on your total income for the tax year.

These rates apply to both the 2024-25 and 2025-26 financial years. From 1 July 2026 (the 2026-27 year), the lowest bracket is set to fall from 16% to 15%.

Source: ato.gov.au

How to Calculate Your Crypto Taxes

First of all, maintaining detailed and accurate records of all Crypto transactions is essential for tax reporting and compliance.

The ATO requires you to keep detailed records of transactions for 5 years after you ’prepared or obtained the records’, or ’completed the transactions or acts those records relate to’, whichever is later.

Free crypto tax tools like cryptact can help you to record all of your transactions without hassle.

Check out Free crypto tax & portfolio management tool: cryptact

Accurate records ensure you can substantiate your claims and comply with tax obligations. These records should include transaction dates, amounts, and values in AUD at the time of the transaction, and the purpose of each transaction.

After collecting all transaction data, to calculate crypto capital gains, follow these steps:

1. Determine the Cost Basis: This is the original value or purchase price of the Crypto, including any associated fees.

2. Determine the Selling Price: This is the amount you received when you sold or exchanged the Crypto, minus any selling fees. Calculate the Capital Gain or Loss: Subtract the cost basis from the selling price.

If the result is positive, you have a capital gain; if negative, you have a capital loss.

Capital Gain (or Loss) = Selling Price - Cost Basis

3. Consider the Holding Period: If you held the Crypto for more than 12 months, you might qualify for the 50% CGT discount which has the effect of making the tax rate on long-term capital gains half the rate that applies to short-term gains.

4. Apply the Appropriate Tax Rate: Use the applicable tax rate based on your total income and the holding period to determine the tax owed.

Calculating your capital gain can be complex, especially if you are trading several coins in several places.

However, tools like cryptact simplify the process.

As an investor, you can generally choose FIFO, HIFO, or LIFO to work out your capital gains, as long as you can identify your individual crypto assets. If you are classed as a trader, the trading stock rules apply and you use FIFO. Cryptact uses FIFO by default and lets you adjust easily if needed.

Using cryptact to calculate your taxes involves a few straightforward steps:

- Sign up for a free account on cryptact.

- Select Australia as your base country and AUD as your currency.

- Connect cryptact to your wallets and exchanges. cryptact integrates with Binance, CoinSpot, CoinJar, Kraken, Coinbase, and more!

- Let cryptact process your transactions.

- Upgrade to a paid plan to download your report.

- Use the report to complete your ATO submission or share it with your crypto accountant.

How to File Your Crypto Tax

Filing your cryptocurrency taxes can be done through various methods.

myTax is the online portal provided by the ATO for filing your tax return, including cryptocurrency transactions. It’s user-friendly and ensures all necessary details are captured.

The Australian tax year runs from 1 July to 30 June. If you lodge your own return through myTax, the deadline is 31 October. If you lodge through a registered tax agent, you usually have until around 15 May the following year.

For those who prefer traditional methods, paper forms are also available for filing taxes. This can be suitable for individuals who are not comfortable using online services.

Penalties for Non-Compliance

Non-compliance with cryptocurrency tax regulations can result in significant penalties.

Penalties for failing to report cryptocurrency transactions can include fines, interest on unpaid taxes, and possible criminal charges for severe breaches. The severity of the penalty depends on the nature and extent of the non-compliance.

To avoid penalties, ensure timely and accurate reporting of all cryptocurrency transactions and maintain proper records. Staying informed about your tax obligations and adhering to them is the best way to avoid any issues.

Strategies for Minimizing Cryptocurrency Taxes

Several strategies can help minimize your cryptocurrency tax liability legally.

Legal Tax Minimization Strategies: Utilize legal methods to reduce your tax liability, such as the 50% CGT discount for assets held over a year.

Deducting Cryptocurrency Mining Expenses: If you operate as a business, you can deduct mining-related expenses. Hold onto an Asset for More Than 12 Months: Benefit from the 50% CGT discount by holding assets for longer periods.

Donate Your Crypto to Charity: Donations to organisations with deductible gift recipient (DGR) status can be claimed as a deduction at the market value of the crypto on the day you donate, in most cases you will still need to report the capital gain on the crypto donated, as if it were a normal sale event, but the tax deduction you get for donating will offset any tax payable on the gain made, and any excess can reduce your other taxable income.

Seeking Professional Advice: Consult with a tax professional who specializes in cryptocurrency to ensure you’re maximizing deductions and complying with all regulations.

Conclusion

Understanding and navigating cryptocurrency taxation in Australia requires diligence and accurate reporting.

By leveraging tools like cryptact, maintaining meticulous records, and seeking professional advice, you can ensure compliance and optimize your tax obligations.

Staying informed about the latest regulations and adopting strategies to minimize your tax liability effectively will help you manage your cryptocurrency investments confidently.

Take the hassle out of filing taxes on your crypto gains with cryptact for free!