Fact-checked and reviewed by MetaCounts.co, a Vancouver-based cryptocurrency accounting firm staffed by Chartered Professional Accountants (CPAs)

If you're mining or staking crypto in Canada, you're likely wondering how the CRA taxes it. The short answer? It depends on what you're doing and how you’re doing it. The Canada Revenue Agency (CRA) doesn’t treat all crypto activity the same. Your tax bill changes based on whether you're just dabbling or running a full-fledged operation.

Mining crypto is considered income in Canada when it’s done with a profit motive. Understanding how staking and mining rewards are taxed can help you stay compliant and avoid costly mistakes.

It may sound daunting, but don’t worry. This guide explains everything about staking vs mining tax in Canada, including when earnings count as business income or capital gains, and how to report these amounts. It also covers staking rewards tax treatment in Canada, GST/HST considerations, audit red flags, and notes on provincial taxes. Use this as a clear roadmap to understand your crypto tax duties in Canada!

If you’d like to learn more in detail about crypto taxes in Canada, check out our Canada Crypto Tax Guide.

Table of contents |

No credit card required

Hobby or Business? How the CRA Views Your Mining or Staking Activity

The CRA looks at your mining or staking activity as a whole. If you're mining or staking often or making good money from it, they'll likely treat it as a business. They decide if it’s a hobby or a business based on things like how big your operation is, what your goals are, and whether you're trying to make money.

If you say it’s just a hobby but it looks like a serious mining or staking setup, that’s a red flag.

For example, in general, if you mine now and then with one computer and don’t earn much, it may count as a hobby. But if you buy lots of rigs and mine regularly for profit, the CRA will treat it as a business. This is a key distinction when considering staking vs mining tax Canada and how your activity fits within the CRA’s expectations.

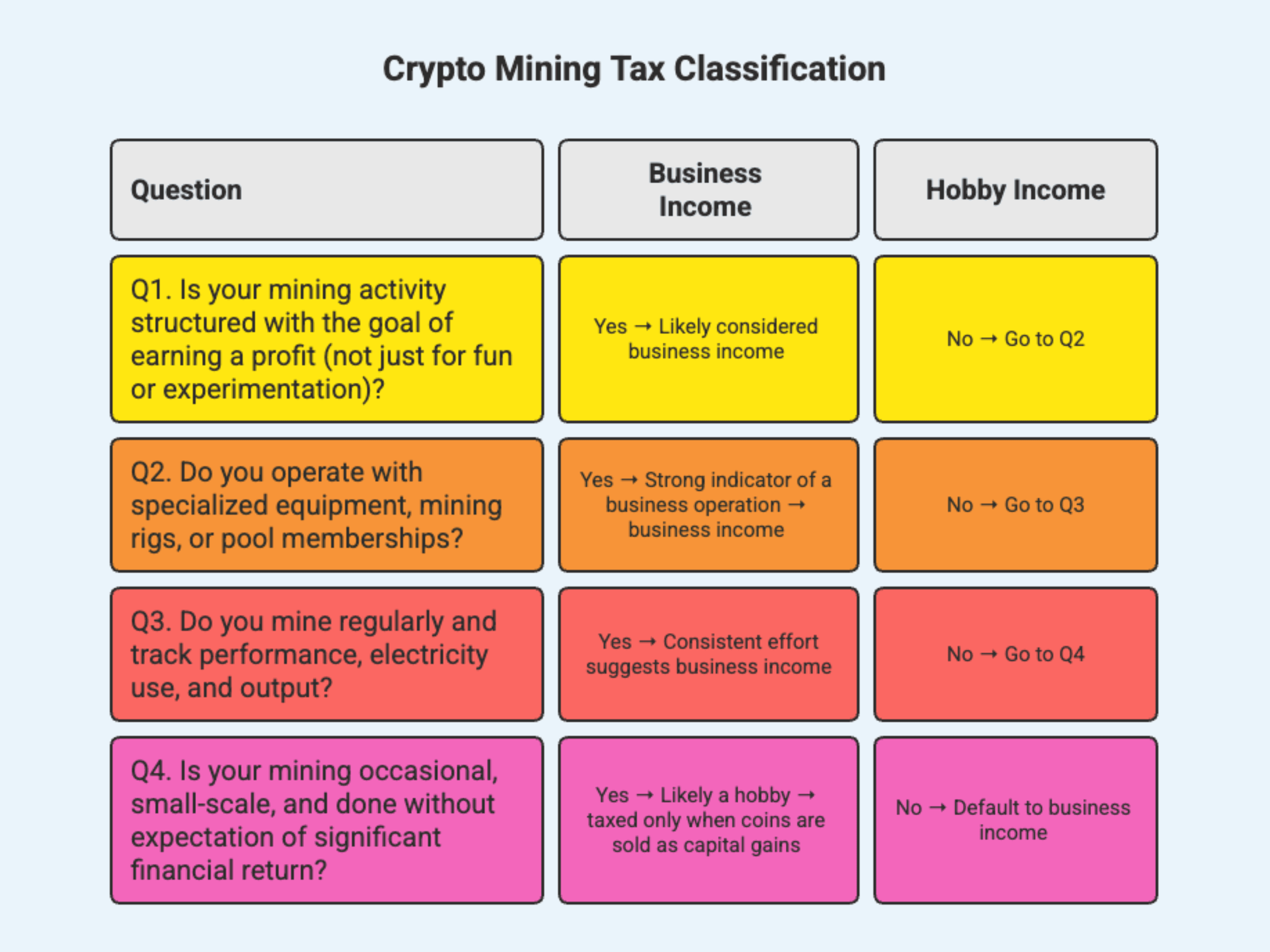

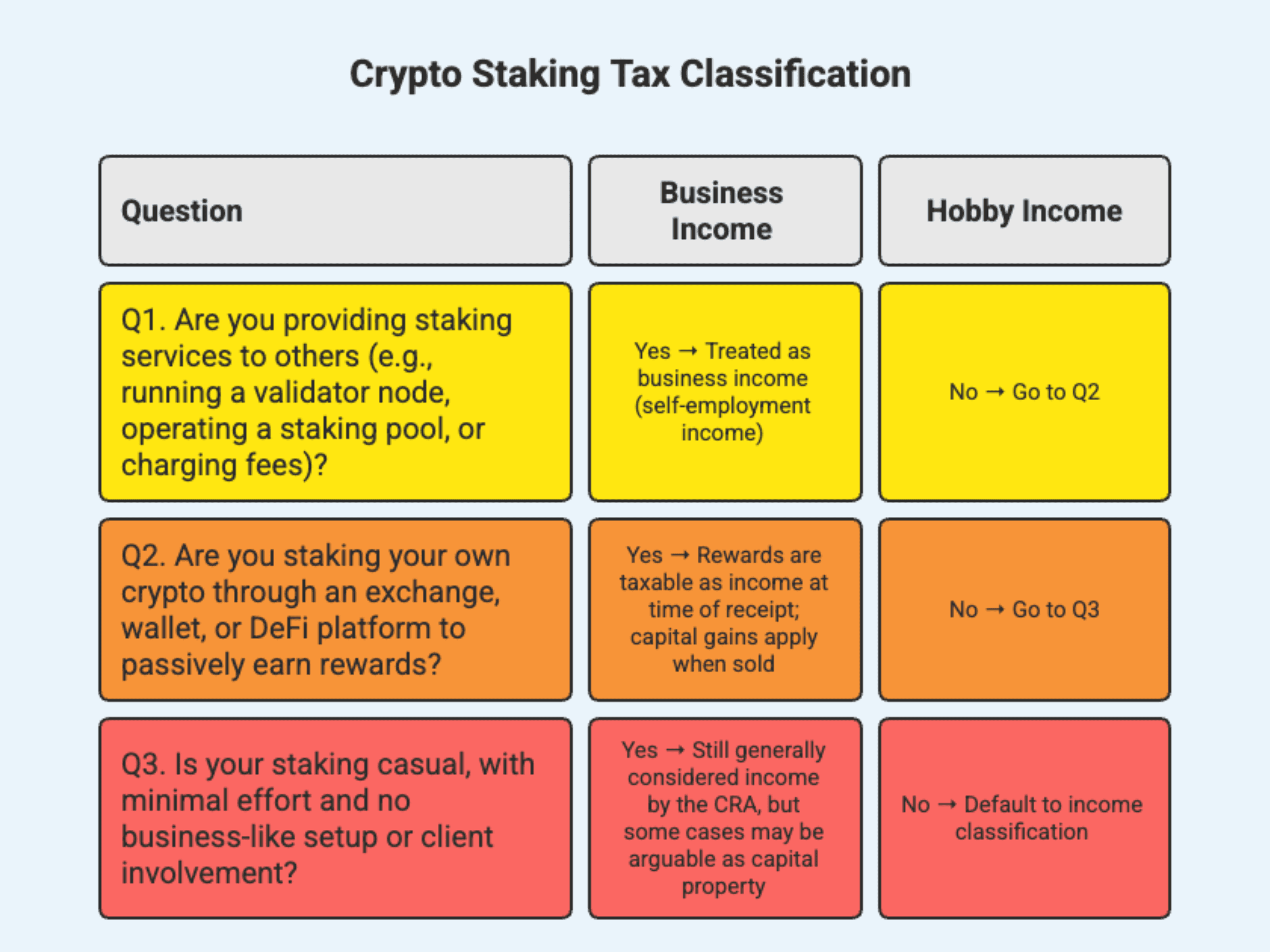

Not sure how your mining or staking income will be taxed? Answer these quick questions to get a better idea of how the CRA is likely to classify your activity. Keep in mind, this provides a general guideline and not a definitive ruling.

Mining classification

Staking classification

Quick Overview: Staking vs Mining Tax in Canada

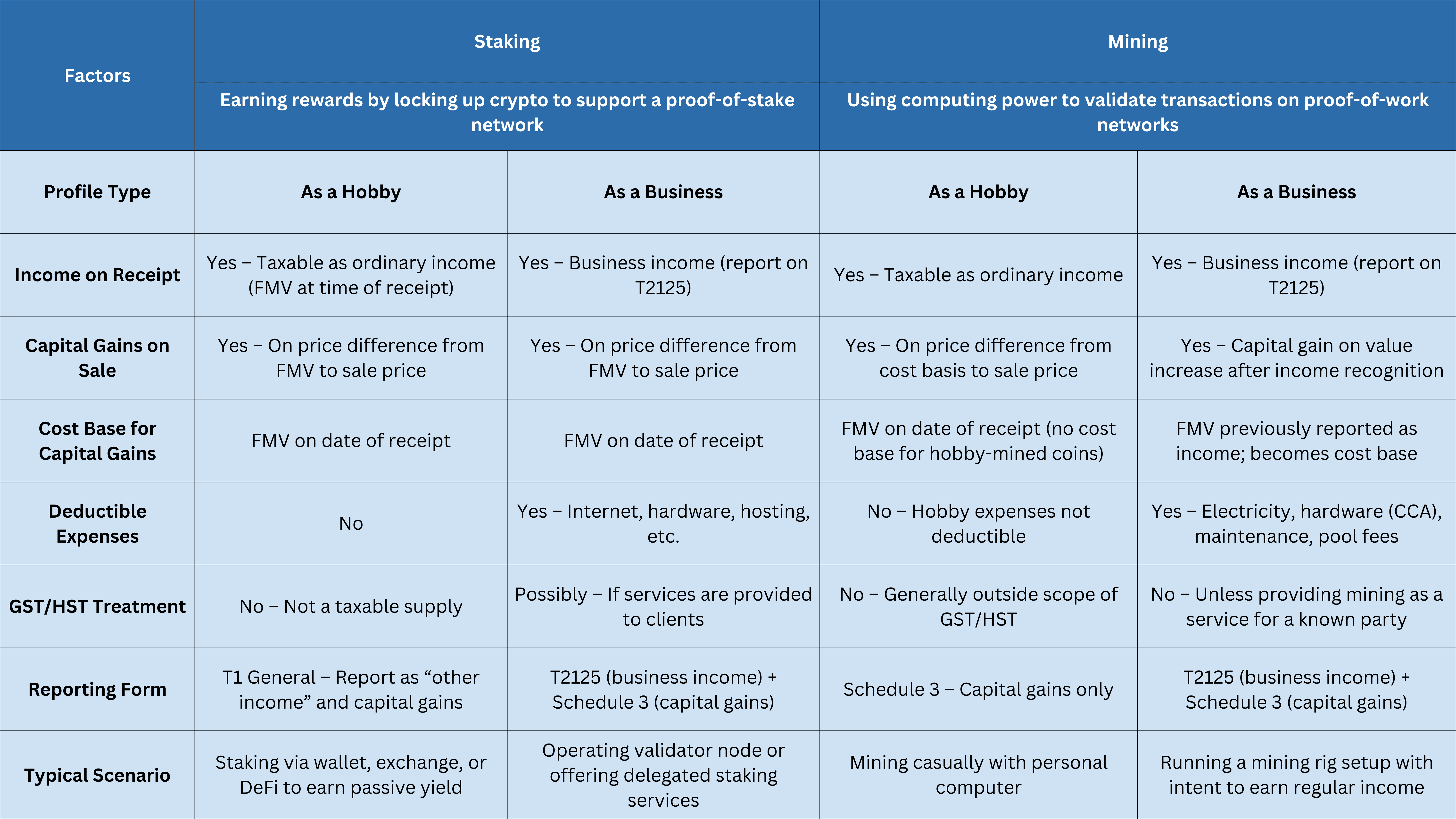

Let’s look at the CRA’s general stance on crypto tax on staking income vs mining through a quick summary. It will help you get a gist of the difference between staking and mining tax.

Crypto Mining: Tax Implications in Canada

Mining involves using computing power to validate blockchain transactions and receive cryptocurrency as a reward. The CRA applies different tax rules depending on whether you mine as a hobby or as a business. Let’s take a look at both the cases for crypto mining tax.

When does capital gains tax apply?

If you mine casually (perhaps to learn or out of personal interest, without a commercial intent) the CRA may consider your mining activity a hobby.

In this case:

- You don’t pay Income Tax when you receive the mined coins.

- You do pay Capital Gains Tax when you eventually sell, trade, spend, or gift them.

- Because the cost base of mined coins is considered to be zero, the entire sale amount is treated as a capital gain. Only 50% of that gain is taxable.

Example: You mine 0.1 BTC and later sell it for $5,000. Since the cost base is $0, the full $5,000 is a capital gain, and you’ll pay tax on $2,500 (50% of the gain).

Note that you cannot deduct mining-related expenses (such as electricity or equipment costs) when mining is treated as a hobby.

When does income tax apply?

So, is mining crypto considered income Canada? If you mine with the intention of earning a profit (for example, you’ve invested in multiple mining rigs or operate regularly) the CRA will likely consider this a business activity.

In that case:

- The value of each coin at the time of receipt is considered business income and must be reported accordingly, on a T2125 form (Statement of Business Activities) as part of your tax return. Platforms like cryptact can help you maintain detailed records of your crypto transactions and estimate taxes across multiple exchanges. This is especially helpful if you're dealing with assets across different jurisdictions.

- You’ll also pay Capital Gains Tax when you dispose of the coins, based on any change in value since receipt.

- The mined cryptocurrency is classified as inventory, not capital property. The CRA allows two methods to value your crypto inventory at year-end. Note that you must apply the same method consistently year after year:

- Value each coin individually at either its acquisition cost or its fair market value (FMV) at year-end, whichever is lower.

- Value the entire inventory at its FMV at year-end.

Example: You mine 1 ETH when it’s worth $3,000. You report $3,000 as income. Later, you sell it for $3,500. This $500 increase is a capital gain for crypto mining tax purposes.

Expense Deductions

As a business, you can deduct expenses related to mining, including:

- Electricity

- Mining hardware (depreciated over time)

- Maintenance

- Mining pool fees

- Internet or hosting costs

However, you must allocate expenses on a per-coin basis and maintain proper documentation.

Crypto Staking: Tax Implications in Canada

As you know, staking is the process of locking up cryptocurrency (on a Proof-of-Stake network) to help validate transactions and earn rewards. It’s becoming increasingly popular with networks like Ethereum, Cardano, Solana, and Avalanche.

So, is staking income or capital gains Canada? As of now, there’s no explicit guidance by the CRA, or any specific rules, that talk about crypto staking tax rules. However, note that the CRA places emphasis on intent. If your goal in staking was to generate profit (which is usually the case, since people stake to earn more crypto), they might lean toward calling it income.

When does income tax apply?

All in all, the CRA generally considers staking rewards as a form of income when you receive them (similar to interest or dividends). Staking rewards tax treatment Canada shows they are considered capital gains when you dispose of them. So, if you stake through a protocol, an exchange, or a DeFi platform:

- The value of the rewards at the time of receipt is taxable as income.

- You must use the fair market value in Canadian dollars on the date of receipt.

Example: You receive 10 DOT tokens as a staking reward when DOT is trading at $5 each. You must report $50 as income.

Make sure to keep a simple record which clearly shows the date, amount, token, and value in CAD.

When does capital gains tax apply?

When you later sell, trade, or spend staking rewards, any increase (or decrease) in value is treated as a capital gain or loss. For crypto staking tax purposes, then:

- Your cost base is the FMV on the date you received the tokens.

- The proceeds of disposition are the value when you sell or trade the tokens.

- The difference is your capital gain or capital loss.

- Only 50% of capital gains are taxable.

Example: You received 10 ADA as rewards, valued at $10 in total. You later sell them for $15. You have a $5 capital gain, and $2.50 is taxable.

Staking as a Business

Most individuals stake as part of a long-term investment strategy. But if you:

- Run a validator node,

- Operate a staking pool, or

- Provide staking services for clients…

...the CRA may treat your activity as a business.

In this case, as per staking rewards tax treatment Canada:

- All staking rewards are business income.

- Just like with mining, you can deduct operating expenses related to running staking infrastructure.

- You must report income on Form T2125 as self-employed income.

Reporting Crypto Mining and Staking Income

The CRA requires you to report all cryptocurrency earnings, including from mining and staking, whether they’re treated as business income or capital gains. You must be wondering, do I report staking and mining differently? Let’s see how to report each correctly:

Business Income Reporting

If your mining or staking activity is classified as a business:

- Form to Use: File Form T2125 – Statement of Business or Professional Activities along with your T1 personal tax return if you are a sole proprietor or operate an unincorporated business.

- What to Report on T2125:

- Total income earned (in CAD) at the time of receiving the crypto.

- All allowable business expenses (e.g., power, equipment, fees).

- Net business income (income minus expenses).

- Where It Goes on the T1: Net income is reported under the self-employment income section, typically lines 13500 to 14300, depending on the business type.

Additional Requirements: You may also be required to pay CPP contributions on your self-employment income.

Capital Gains Reporting

You must be wondering, what CRA form do I use for staking rewards? And what about my earnings via mining? If your mining or staking is treated as capital in nature (including hobby or investment):

- Form to Use: Report the transaction on Schedule 3 – Capital Gains (or Losses).

- What to Report on Schedule 3:

- Proceeds of disposition (CAD value when the crypto was sold).

- Adjusted cost base (ACB) – usually the value of the crypto when received.

- Outlays and expenses (e.g., fees related to selling).

- Taxable Amount: Only 50% of the net capital gain is included in your taxable income.

- Where It Goes on the T1: Total taxable capital gains are entered on line 12700 of your return.

Additional Note: If you have multiple crypto dispositions, you can summarize them on Schedule 3 and attach a detailed statement or report from crypto tax software.

Fair Market Value (FMV) Requirement

In both business and capital reporting:

- You must determine the fair market value in Canadian dollars at the exact time you received the mined or staked crypto.

- Use a consistent and reasonable valuation method (e.g., exchange rate at receipt time or an average from multiple exchanges).

- Maintain detailed records, including timestamps and valuations.

GST/HST Considerations

Along with the common question of how is crypto mining taxed in Canada, people also wonder about GST/HST. Note that:

- Mining and staking rewards are generally not subject to GST/HST as they are not considered taxable supplies.

- If you accept crypto as payment for goods or services in a business context, you must charge and remit GST/HST based on the CAD value at the time of payment.

- All crypto-related amounts must be converted to Canadian dollars for tax purposes. The CRA does not accept crypto-denominated reporting.

Keeping Records and Documentation

As per CRA crypto tax rules for staking and mining, you need to maintain detailed records for all crypto activities. You must maintain accurate, time-stamped records to support your tax filings and defend against audits. Keep:

- Transaction Logs: Record the date, time, type, and amount of each crypto transaction, its CAD value, purpose (e.g., mining, staking, trade), and counterparty info (e.g., wallet address or exchange).

- Wallet Info: Track all wallet addresses, and record yearly opening/closing balances for each asset.

- Exchange Data: Download and store account statements, trade histories, and transfer records regularly.

- Mining Records: Keep receipts for hardware, electricity, pool fees, repairs, and document hardware specs, operation times, and agreements.

- Staking Records: Log platforms used, fees/commissions, deposit/withdrawal activity, and terms of service.

- Valuation Method: Use a consistent source (e.g., exchange rate or price index) to determine CAD value at time of each transaction.

- Cost Base & Holding Period: Track adjusted cost base (ACB) using the average cost method for each type of crypto asset.

- Retention: Keep all crypto-related records for at least 6 years after the tax year.

It is advisable to use crypto tax software or organized spreadsheets. Platforms like cryptact help you track mining and staking income, wallet balances, and transaction values. This simplifies tax reporting and keeps you aligned with CRA rules. From mining rigs to DeFi staking, cryptact keeps your tax reporting audit-ready. Sign up here.

Endnotes

A common question among Canadians that dabble in crypto is, how are staking and mining rewards taxed? If you earn crypto through mining or staking in Canada, it is important to understand how the CRA treats each type of activity.

The difference in staking vs mining tax can affect how much you owe and what forms you need to file. Your tax obligations depend on whether you are doing it as a hobby or as a business.

Clear records, consistent reporting, and the right forms can help you stay compliant. Platforms like cryptact can also help by organizing your transactions and making tax time easier. Stay informed, stay organized, and don’t let crypto taxes catch you off guard.