Fact-checked and reviewed by MetaCounts.co, a Vancouver-based cryptocurrency accounting firm staffed by Chartered Professional Accountants (CPAs).

Airdrops and forks sit in one of the least tidy areas of Canadian crypto tax. CRA now has dedicated crypto pages for transactions, valuation, recordkeeping, and mining and staking, but it still does not publish a standalone page that cleanly answers how airdrops and hard forks should be taxed. That means taxpayers usually have to apply CRA’s general crypto rules first, then use a careful facts-and-circumstances analysis where CRA is silent.

That is why this topic feels so confusing. Some receipts look closer to business income because they are tied to services, promotion, or organized activity. Others look more like unsolicited windfalls, especially where a taxpayer simply held a coin and later found new tokens in the wallet after a fork or an unsolicited airdrop. The later sale of those tokens is much clearer: once you dispose of them, the profit or loss still has to be reported as either business income or a capital gain or loss, depending on the facts.

This guide keeps the focus on the core rule, the reporting line, and the practical cost-basis issue that usually matters most.

Key takeaways

- CRA does not currently publish a dedicated airdrops-and-forks page, so the analysis starts with its general crypto rules on business income, capital gains, valuation, and records.

- If an airdrop or fork receipt is tied to business-like activity, services, or organized effort, the case for income on receipt is stronger.

- For ordinary investors who receive tokens unsolicited, Canadian tax commentary often treats the receipt as potentially non-taxable on arrival, with tax arising more clearly when the tokens are later sold or exchanged.

- If you did not include any amount in income when the tokens arrived, the tax cost may effectively be nil. If you did include the receipt as income, that amount generally becomes the starting tax cost.

- Capital-account disposals generally flow through Schedule 3 and line 12700. Business-account results generally flow through Form T2125.

Table of contents |

No credit card required

Why airdrops and forks are tricky in Canada

Most crypto tax questions start with a transaction you chose to make. Airdrops and forks are different because the receipt can happen without a clear purchase, without a cash price, and sometimes without any real effort on your part. That makes the first tax question less obvious. Before you can ask whether the later sale is taxable, you have to ask what the receipt itself was in the first place.

This is also why the common question “Do I owe tax if I never sell?” does not have one universal answer. If the receipt itself is characterized as income, tax can arise before sale. If the receipt is not treated as income on arrival, the more obvious tax point is usually the later disposition. So the answer depends less on the token label and more on the facts behind how and why it was received.

How CRA’s general framework applies to airdrops and forks

CRA does not publish a specific bulletin for airdrops and hard forks, so this analysis has to be built from CRA’s general crypto framework rather than from a dedicated CRA position on these receipts. CRA’s current crypto guidance begins with a broad split: crypto results are either business income or loss, or capital gains or losses, depending on the circumstances. CRA also lists the main factors that can point toward business treatment, including frequency of transactions, short holding periods, market knowledge, time spent, financing, and conduct similar to that of a trader or dealer. Those are the same core factors you have to use when analyzing airdrops and forks, because CRA does not give a separate test just for these receipts.

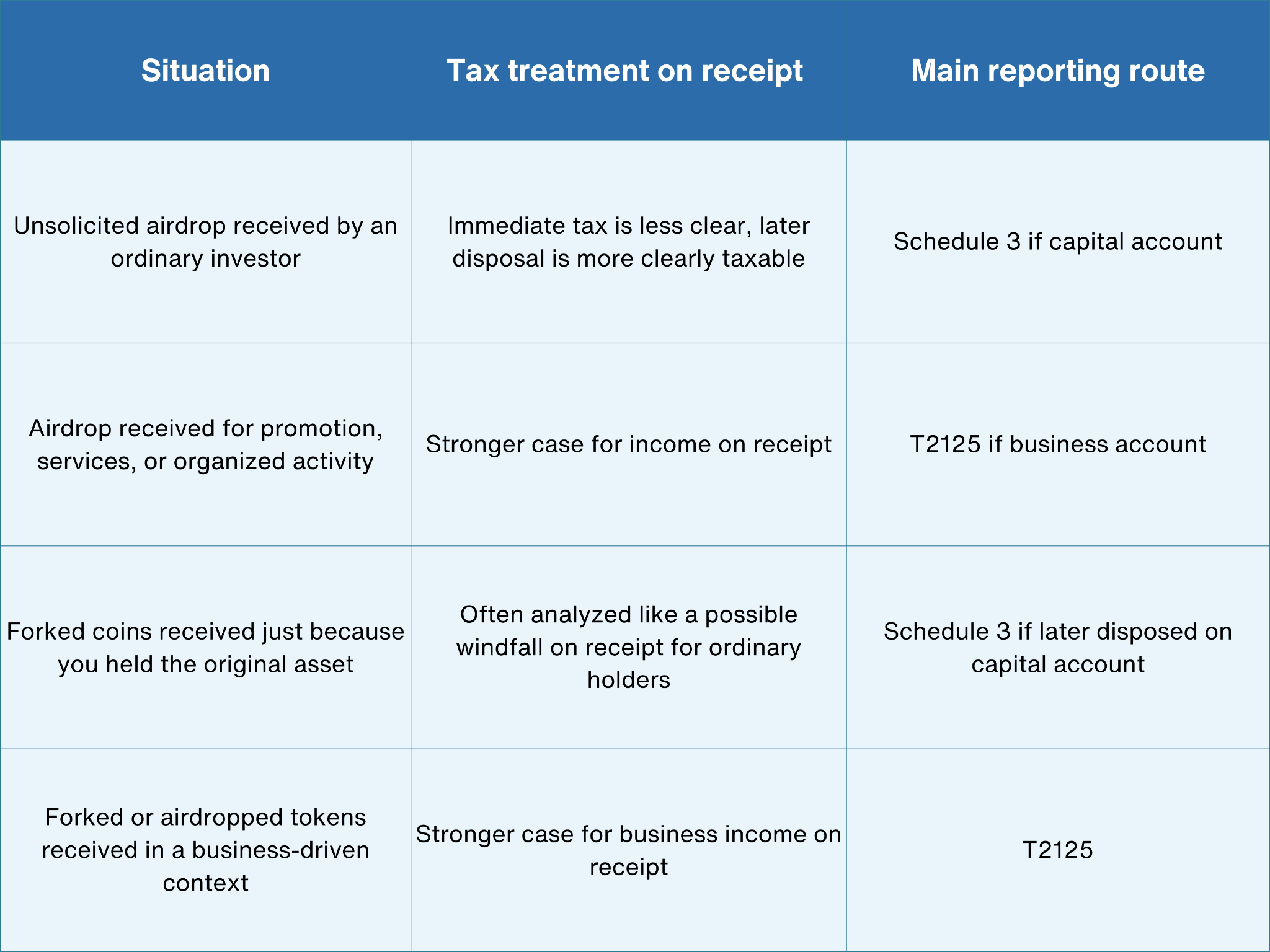

A practical way to read the main scenarios is this:

The reason this table is framed as a “practical starting point” is that CRA’s silence leaves room for interpretation. Canadian tax commentary is fairly consistent that unsolicited receipts are harder to treat as income on arrival than receipts tied to business activity or services. But that is still an interpretation built on general tax principles, not a neat CRA airdrop bulletin.

When an airdrop may be taxable

The clearest case for tax on receipt is where the airdrop functions like payment or business income. If someone receives tokens because they promoted a project, performed services, or carried on a business activity that made the receipt part of a profit-making pattern, the income-on-receipt argument is much stronger. Canadian tax commentary makes this point directly, and it also fits CRA’s broader business-income framework.

For ordinary investors, the picture is different. Canadian commentary on airdrops often treats unsolicited receipts as potentially non-taxable when received because they do not necessarily arise from a source of income. That is especially true where the taxpayer did not perform services, did not solicit the tokens in a business-like way, and had no enforceable claim to receive them. In that reading, the later sale becomes the clearer tax point.

This also answers one of the most common practical questions: what if you receive an airdrop and never sell it? If the receipt is not treated as income on arrival, there may be no immediate tax merely because the tokens landed in your wallet. But if the receipt was tied to business activity or compensation-like facts, you should not assume “not sold” means “not taxable.” The character of the receipt still matters.

How hard forks are usually analyzed

Hard forks are often easier to describe than airdrops because the taxpayer usually held the original coin first and then received new units after a chain split. For ordinary holders, Canadian legal commentary has long suggested that forked coins can look like a possible tax-free windfall on receipt where the holder had no role in creating the fork, no organized effort was required, and the receipt did not arise from an income-producing source.

That said, the result does not apply universally. The same commentary points out that if a person was actively involved in creating or driving the fork, or received forked coins in a business-like context, the receipt looks much more like taxable business income. That distinction is important because it keeps the analysis tied to facts rather than to the simple label “hard fork.”

For most ordinary investors, the main tax event still becomes the later sale or exchange of the forked coin. Even if the receipt was not taxed on arrival, the disposition is not ignored. Once you sell or swap the forked token, CRA’s general business-versus-capital framework takes over just like it would for any other crypto disposition.

Cost basis and reporting

Cost basis is where these files often go wrong.

CRA’s valuation page says you need to determine the value of crypto-assets when transactions occur, use a reasonable method, and apply it consistently. Its general crypto page also makes clear that gains and losses are computed using proceeds and adjusted cost base. The problem with airdrops and forks is that the tax cost depends on whether you treated the receipt itself as income.

Canadian tax commentary is quite clear on this practical point. If the airdropped or forked tokens were treated as a tax-free windfall on receipt, the tax cost may effectively be nil. If the receipt was included in income on arrival, that reported amount generally becomes the starting tax cost for the tokens. That difference can completely change the size of the later gain.

A simple airdrop example shows why this matters.

Suppose you receive an unsolicited airdrop of tokens and do not treat the receipt as income because the facts support a windfall-style position. A year later, you sell all of those tokens for C$1,200. On that approach, the later gain is much larger because there may be little or no acquisition cost to deduct. By contrast, if the same tokens had been reported as C$800 of income when received in a business context, that C$800 would generally become the starting tax cost, and the later sale at C$1,200 would produce a much smaller additional gain.

For reporting, the route itself is relatively straightforward once the characterization is settled:

- If the later disposition is on capital account, the gain or loss generally flows through Schedule 3 and then line 12700.

- If the receipt or later sale is on business account, the result generally flows through Form T2125.

The complicated part is not the form. It is documenting why you chose capital or business treatment, what value you used, and how you tracked cost basis from receipt to sale.

CRA’s recordkeeping page is especially important here. It says taxpayers should keep the number of units, date and time, value in Canadian dollars, the nature of the transaction, wallet addresses, and beginning and ending balances, as well as exchange trade and transfer ledgers where applicable. Airdrops and forks often look minor when they arrive, but they can create major reporting problems later if the receipt date and valuation are not preserved.

How cryptact helps

Airdrops and forks create exactly the kind of file that becomes messy at year-end. There may be no purchase invoice, no obvious acquisition cost, and no clean reminder of what the token was worth when it first appeared. Then months later the token is sold, swapped, or moved across wallets, and the taxpayer is trying to reconstruct the entire history backwards.

That is where cryptact helps in a practical way. It brings exchange and wallet records together, keeps the receipt history easier to review, and makes it much easier to support the value used at receipt and the gain used on later disposal. For users dealing with airdrops, forks, and similar “crypto received but not bought” situations, that structure matters because the hardest part is usually not the concept. It is the record trail.

Conclusion

A clean airdrops-and-forks analysis in Canada starts with one simple question: why did you receive the tokens? If the answer points toward business activity, services, promotion, or organized effort, the case for income on receipt is stronger. If the answer is simply that you held a coin and new tokens appeared without action or payment on your part, the immediate tax treatment is much less clear, and the later sale often becomes the more obvious tax point.

That is why the safest workflow is characterization first, cost basis second, and reporting form third. Once you know whether you are dealing with business income or a capital disposition, the form choice is much easier. That is also where cryptact adds real value. It helps keep the receipt history, valuations, and later disposals organized enough that your final CRA reporting is far easier to prepare and defend.