Fact-checked and reviewed by MetaCounts.co, a Vancouver-based cryptocurrency accounting firm staffed by Chartered Professional Accountants (CPAs).

Crypto traders often think tax starts only when they sell into Canadian dollars. CRA does not use that rule. If you swap one coin for another, you usually dispose of the coin you gave up, and that step can create a gain or loss right away. CRA’s crypto guidance even includes a worked example for trading one crypto-asset for another. This disposition logic applies whether you trade on a centralized exchange, a DEX, or an in-app convert feature. The label does not change the tax result.

That misunderstanding drives many crypto tax reporting errors in Canada. Some investors export only fiat-denominated sales, skip pair trades, or miss ACB changes after conversions. This guide gives you the practical path from trade history to reporting, with plain-language examples for swaps, stablecoin conversions, and common trading pairs.

Key Takeaways

- CRA can tax crypto-to-crypto trades in Canada even when you do not cash out to CAD, because a swap or conversion can trigger a disposition.

- You need the fair market value in CAD at the time of each trade to calculate gains, losses, and your ongoing ACB.

- Wallet transfers between wallets you own do not create a taxable disposition, but you still need records to prove ownership and match transfers.

- Most retail investors report capital gains on Schedule 3 and line 12700, while business-like trading activity can move reporting to business income rules and T2125.

- cryptact helps you consolidate exchange and wallet data, track ACB across pair trades, and prepare CRA-ready reports.

No credit card required

How CRA views crypto-to-crypto trades in Canada

For Canadian tax purposes, crypto-assets are generally classified as property rather than currency, and CRA looks at dispositions, not only cash withdrawals. In CRA’s crypto guidance, the agency shows that a trade from one crypto-asset into another can create a capital gain or capital loss when you hold the disposed asset on a capital account.

CRA also draws a line between capital activity and business activity. CRA lists factors like transaction frequency, short holding periods, market knowledge, time spent, and financing when it decides whether you carry on a business. CRA reviews your facts case by case.

That matters because CRA taxes the result in two different ways:

- Under capital treatment, you include 50% of net capital gains in income.

- Under business treatment, you report the full profit or loss as business income (or loss).

If you search for crypto swap tax Canada rules, CRA crypto swaps guidance, or crypto-to-crypto taxable event Canada explanations, this capital vs. business split usually causes confusion. The swap can trigger tax under either route. Your trading pattern decides the route.

Where “barter” fits and where it does not

Many people see “barter” in CRA crypto articles and apply it to every crypto trade. CRA uses “barter” when you use crypto to pay for goods or services, because you exchange value without government-issued currency.

For crypto-to-crypto trades, CRA still taxes the transaction through disposition rules. So if you trade ETH for USDT, you do not need barter labels to know that a tax event can happen. You still calculate proceeds, ACB, and gain or loss on the coin you disposed of. CRA’s worked example for trading one crypto-asset for another shows exactly that. For pure crypto-to-crypto trades, you can apply the standard disposition framework without focusing on the barter label.

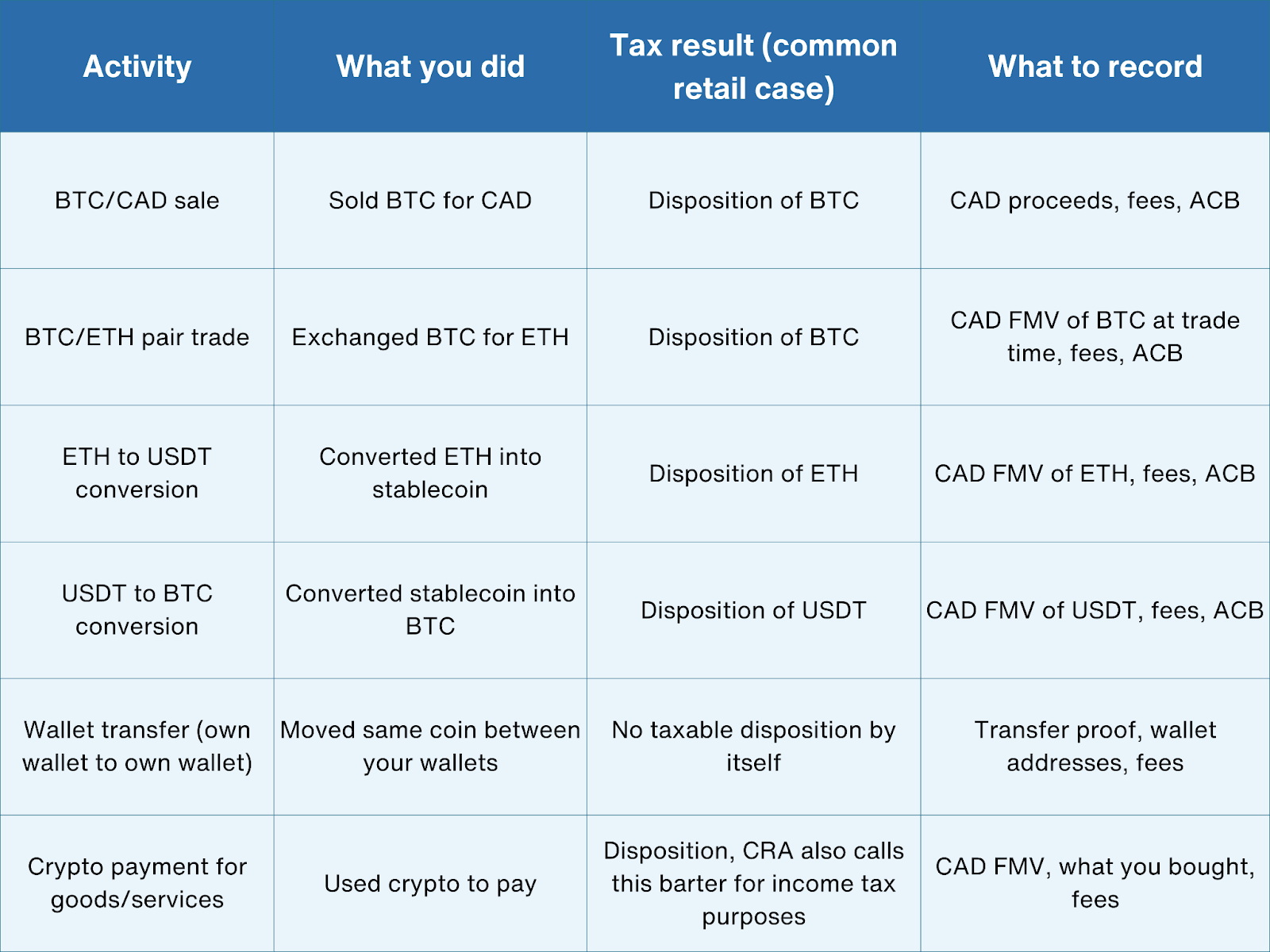

What counts as a swap, conversion, or pair trade

Crypto traders use different words on exchanges and wallets. CRA focuses on what you gave up and what you received.

Here is a simple map for crypto trading pairs tax in practice.

This table assumes you hold these assets on capital account. If CRA treats your trading as business activity, the tax result and reporting forms change even when the underlying transactions look the same.

Moving crypto between wallets that you control is generally not considered a disposition, provided ownership does not change. CRA also says you must keep records that identify wallet addresses, transaction details, and balances, which helps you prove that a movement was your own transfer and not a disposal.

Example that clears up “conversion” confusion

A lot of people ask about crypto conversion tax Canada rules for simple in-app conversions.

Example:

- You convert 1 ETH to USDT on an exchange

- The exchange labels it “Convert,” not “Trade”

- You never touch CAD

CRA still looks at the economic result. You gave up ETH and received another asset. That step can create a taxable gain or loss on the ETH you disposed of. The platform label does not change the tax result. The agency’s guidance focuses on the disposition itself.

How to calculate tax on crypto swaps and conversions

This section usually creates the biggest errors in crypto trading cost basis Canada calculations. You need 3 things for each swap.

1) Determine the fair market value in CAD at the time of the trade

Use a reasonable method to determine fair market value in CAD at the time of each transaction and apply it consistently year over year. CRA accepts fair market value for crypto tax reporting in most cases and expects you to record values in Canadian dollars.

If your platform reports values in USD, convert to CAD using the exchange rate for that date. CRA’s capital gains guidance asks you to report gains and losses in Canadian dollars and use the transaction-day rate, or an annual average in appropriate cases. Keep a defensible method and consistent records.

2) Calculate the gain or loss on the asset you disposed of

For capital treatment, you compare:

- Proceeds of disposition (usually the CAD fair market value at the time of the swap)

- Minus adjusted cost base (ACB) of the units you disposed of

- Minus outlays and expenses for the disposition (such as fees, where applicable)

CRA’s crypto tax tip and CRA’s crypto income page both describe this framework for capital gains and losses from crypto dispositions. It also notes that half of the capital gain becomes a taxable capital gain.

3) Update ACB for the asset you received

After the swap, the coin you received enters your records with a cost based on the trade value and fees. For many retail investors, the hard part comes next because later swaps depend on this updated ACB. CRA’s 2024 crypto tax tip refers to adjusted cost base as usually the weighted average cost for crypto-assets.

Example 1: ETH to USDT tax Canada calculation

Let’s use a simple example to illustrate how Ethereum-to-USDT swaps are taxed in Canada.

You hold ETH as an investment.

- Your ACB for 1.5 ETH = CAD 3,600 total

- You swap 1 ETH for 4,200 USDT

- At the trade time, 1 ETH = CAD 4,250

- Trading fee = CAD 25

Capital gain on ETH disposed:

- Proceeds = CAD 4,250

- Minus ACB of 1 ETH = CAD 2,400 (assuming your weighted average ACB works out to CAD 2,400 per ETH)

- Minus fee = CAD 25

- Capital gain = CAD 1,825

Taxable capital gain (50%) = CAD 912.50

You then record the received USDT with a cost base tied to the trade value and fees based on your records method. Keep the exact exchange export, timestamp, and CAD value in case CRA asks for support. It asks for date/time, CAD value, transaction description, wallet addresses, and ledgers.

Example 2: BTC to altcoin tax Canada pair trade

This example answers the common bitcoin to altcoin tax canada question.

- You swap 0.05 BTC into an altcoin pair

- CAD value of 0.05 BTC at execution = CAD 5,000

- Your ACB for that 0.05 BTC = CAD 4,100

- Fee = CAD 15

Capital gain = 5,000 − 4,100 − 15 = CAD 885

Taxable capital gain = CAD 442.50

You also create the initial cost basis for the altcoin you acquired. If you later sell or swap that altcoin, your next calculation starts from that recorded cost.

Stablecoin swaps still need records

People often assume stablecoin swaps tax Canada rules create no tax because price moves look small. Price movement might stay small, but the trade can still trigger a disposition. If you swap one stablecoin for another or swap crypto into a stablecoin, run the same process and log the trade. Small gains or losses still count in your records and annual totals.

How to report crypto-to-crypto trades to CRA

Many readers ask how to report crypto-to-crypto trades under CRA rules in practical filing terms. The answer depends on whether the agency would view your activity as capital or business.

Capital account reporting (most retail investors)

CRA says that if you dispose of crypto-assets on account of capital, you include half of capital gains in income. The 2024 crypto tax tip points taxpayers to the “Bonds, debentures, promissory notes, crypto-assets, and other similar properties” section of T1 Schedule 3 for reporting capital gains or losses from crypto-asset transactions.

CRA’s Schedule 3 guidance for the 2025 tax year (filed in 2026) says you calculate taxable capital gains on Schedule 3 and report the amount on line 12700 of your return.

In practice, that means you should prepare an annual summary from your transaction-level records:

- Total proceeds from taxable dispositions

- Total ACB for disposed units

- Fees and outlays

- Net capital gain or net capital loss in CAD

Business income reporting (if your activity looks like trading business activity)

If CRA treats your crypto activity as business income, you need to report the full profit or loss from dispositions in your tax return. CRA also provides Form T2125 to report business or professional income and expenses.

This route often applies when your conduct looks like an active trading business, not a personal investment approach. CRA lists factors, and it reviews all facts together. Frequency alone does not settle the issue, but it can carry weight.

Common mistakes that create crypto tax reporting errors

Crypto swap reporting breaks down in a few predictable places. These mistakes show up in retail records across CEX accounts, DEX wallets, and wallet-to-wallet movements.

1) Treating only CAD cash-outs as taxable

This mistake creates missing crypto transaction tax problems right away. A swap, conversion, or pair trade can create a taxable disposition even without fiat. CRA’s own example on trading one crypto-asset for another makes this clear.

2) Ignoring fees in gain or loss calculations

Fees can change your gain or loss and your ongoing cost basis. If you ignore fees across hundreds of trades, your final number can drift a lot.

3) Breaking ACB when you trade across multiple platforms

ACB tracking issues increase in Canada when people calculate cost basis per exchange instead of across their full holdings of the same asset. If you hold BTC on 3 exchanges and 2 wallets, your records still need a clean aggregate ACB trail for the units you dispose of under your reporting approach.

4) Marking internal wallet transfers as taxable

CRA says a transfer between wallets that you own does not create a taxable disposition. You still need strong records to prove ownership and to match deposits and withdrawals.

5) Keeping incomplete records and waiting until filing season

CRA asks taxpayers to keep detailed books and records, including date and time, CAD value, wallet addresses, trade ledgers, transfer ledgers, and beginning/ending balances. It also says you must keep required records for at least 6 years and encourages electronic recordkeeping with regular exports.

How cryptact helps with crypto trading cost basis in Canada

Crypto-to-crypto reporting gets messy fast because each trade changes two things at once. You create a disposal for the coin you gave up, and you create a new cost basis trail for the coin you received. That complexity grows across spot exchanges, wallet conversions, and pair trades.

This is where cryptact helps in a practical way. cryptact lets you consolidate trades across exchanges and wallets, classify transactions, and keep a cleaner transaction history for swaps, conversions, and transfers. It helps you calculate gains and losses under Canadian rules, including ACB-based tracking needs for capital reporting, and it gives you tax reports and records that you can use when you prepare your CRA filing.

It also helps you reduce one of the biggest filing risks in crypto taxes, multi-exchange workflows, which is reconciliation drift. When you keep transfers, swaps, and fees in one system, you can spot missing rows before they turn into a wrong Schedule 3 total or a broken audit trail.

Conclusion

Crypto-to-crypto trades in Canada can trigger tax even when you never sell into cash. CRA looks at dispositions, so swaps, conversions, and pair trades can create gains or losses at the moment you exchange one asset for another. The core job stays simple in theory and demanding in practice: record the CAD fair market value, calculate the gain or loss on the asset you disposed of, and keep your ACB records clean for the next trade.

If you want to file with fewer surprises, start with complete records and a repeatable workflow. cryptact helps you pull together exchange and wallet data, track gains and losses for crypto swaps and conversions, maintain cleaner ACB records across pair trades, and generate reports you can use for CRA reporting. That gives you a stronger base for accurate filing and much less stress at tax time.