Fact-checked and reviewed by MetaCounts.co, a Vancouver-based cryptocurrency accounting firm staffed by Chartered Professional Accountants (CPAs)

Cryptocurrency has moved firmly into the Canadian mainstream. In 2025, more Canadians than ever are buying, trading, and even earning digital assets—turning what was once a niche hobby into a significant source of income.

Yet one question still confuses many investors and traders: should the profits from crypto transactions be reported as capital gains or as business income?

In this article, we break down the CRA’s rules on that crucial distinction, clarify which crypto events are taxable (and which are not), and share practical tax-saving strategies you can use to keep more of your hard-earned gains.

Table of contents |

If you are new to crypto tax, read our ultimate crypto tax reporting guide.

No credit card required

Canada Crypto Capital Gains and Tax: The Basics

The Canada Revenue Agency (CRA) treats cryptocurrency as a form of property (commodity) for tax purposes, not as a currency. This means that any income or gains from crypto are generally subject to tax.

How your crypto transactions are taxed depends on their nature:

Capital gains

If your crypto activity is investment-oriented (e.g. buying and holding for appreciation or occasional selling), profits are treated as capital gains. For 2025, only 50% of a capital gain is taxable (the “inclusion rate”).

Example

If you made a $1,000 profit selling Bitcoin, $500 would be added to your taxable income.

| Note: The government is currently planning to raise the inclusion rate to two-thirds for high-value Canada crypto capital gains, but this change won't apply until the 2026 tax year. |

Business income

If your crypto trading is frequent, commercial, or done with a business-like approach, profits may be classified as business income (100% taxable).

In this case, crypto is treated as inventory rather than capital property. All of the profit is taxable as income (no 50% reduction). Related expenses and losses are fully deductible against crypto business income.

Whether your crypto is taxed as a capital gain or business income depends on how you use it. The CRA looks at your trading frequency, holding period, level of effort, and intent to profit. If your position seems unclear, talk to a professional.

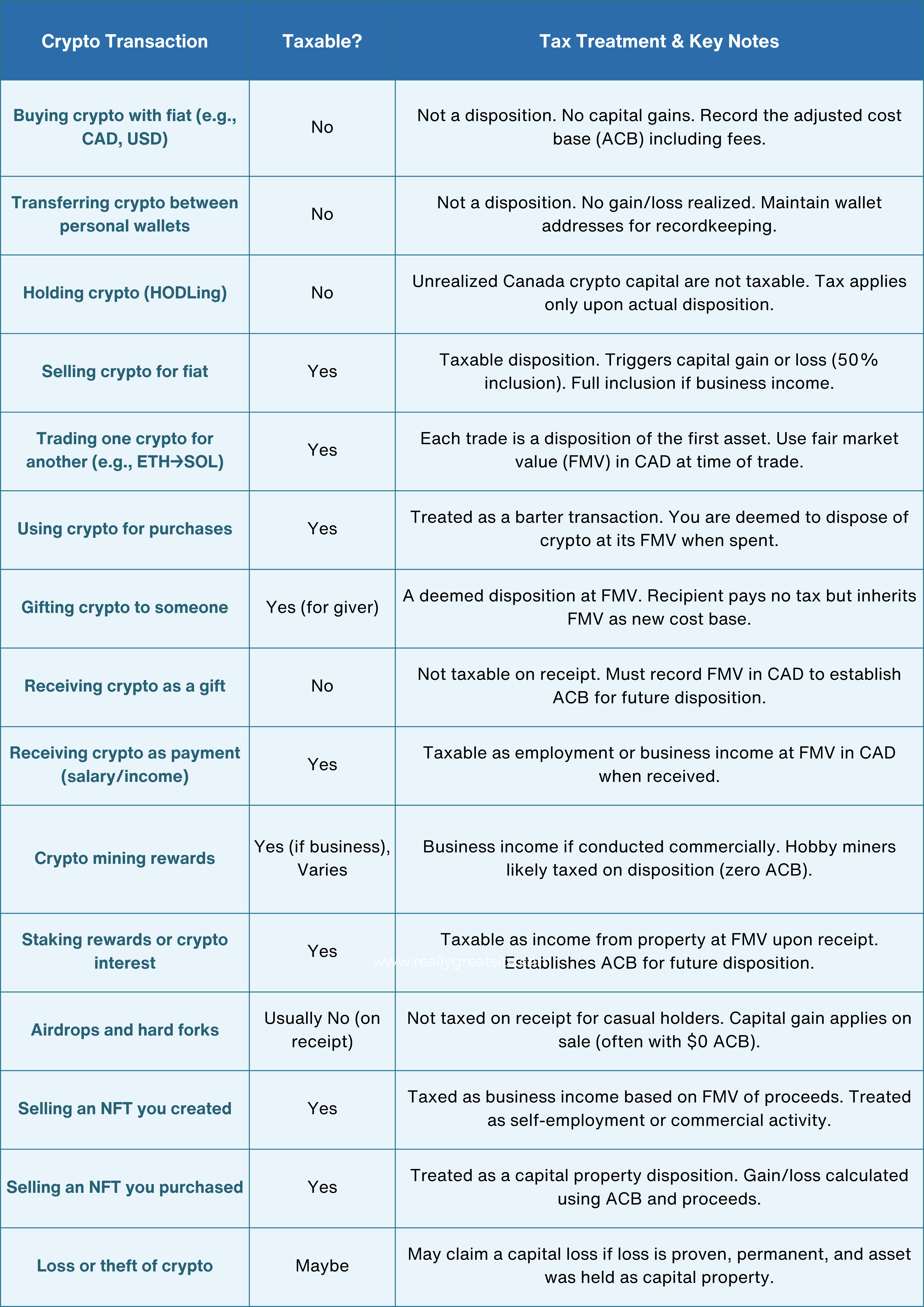

Taxable vs. Non-Taxable Crypto Transactions

Not every crypto transaction triggers taxes. The table below summarizes common crypto events and whether they are taxable under 2025 CRA crypto reporting requirements:

Calculating Capital Gains and Reporting Crypto Transactions

How Capital Gains Are Calculated

You need to calculate your Canada crypto capital gains or losses every time you dispose of your cryptocurrency. A disposal includes selling, trading, or using crypto to buy something.

The basic formula to calculate capital gains or losses in Canada is:

| Capital Gain or Loss = Proceeds of Disposition (in CAD) − Adjusted Cost Base (ACB) − Selling Costs |

The adjusted cost base (ACB) is what you paid to buy the crypto, including any transaction fees. If the result is positive, it's a capital gain. If negative, it's a capital loss.

For 2025, only 50% of capital gains are taxable, and only 50% of capital losses can be used to offset gains. If your losses are more than your gains, you can apply the extra loss to past or future years.

Average Cost Method (Required by CRA)

The CRA requires you to use the average cost method for calculating capital gains on crypto. This means you must calculate the average cost per unit of each type of cryptocurrency you own (e.g. Bitcoin, Ethereum) and update it as you buy more.

Each type of crypto is considered an “identical property”, so you must track the ACB separately for each one. Methods like FIFO or picking specific coins to sell are not allowed.

Example:

If you buy 1 unit of a cryptocurrency for $2,000, then another for $3,000, and a third for $5,000, your total cost is $10,000. The average cost per unit is $3,333. If you sell one unit, you use $3,333 as your cost base.

Always include buying fees in your ACB and deduct any selling costs when you sell.

Superficial Loss Rule

If you sell a cryptocurrency at a loss and then buy the same one back within 30 days, the CRA may deny the loss under the superficial loss rule. This rule also applies if someone affiliated with you, such as your spouse or a company you control, buys back the same asset within that period.

Please note that, as of the time of writing, this rule is not supported in the current implementation of cryptact.

How to Report Crypto Capital Gains in Canada

1. Based on Your Role

For Individuals

If you are an individual investor, you report your Canada crypto capital gains and losses using Schedule 3 of your personal income tax return. This falls under CRA reporting crypto gains Schedule 3 requirements.

You do not need to list every transaction, but you must be able to show how you calculated your totals. Only the taxable portion of your net gain is included in your income.

For Business Activity

If your crypto activity is commercial, your income is reported differently. You must report all crypto-related revenue as business income, which is fully taxable.

Use Form T2125 if you are self-employed or the appropriate corporate forms if you operate through a business. Self-employed individuals have until June 15 to file, although any tax owing must still be paid by April 30. However, note that it is rare for your individual crypto investments to be recognized as a business activity.

2. Based on the Nature of the Crypto Activity

Receiving Crypto as Income:

If you are paid in cryptocurrency, you must report it as income. The amount you report is based on the fair market value of the crypto at the time you received it, in Canadian dollars.

This income can be reported as salary, self-employment income, or other income, depending on your situation.

Non-Resident Considerations:

If you are not a Canadian resident, you are usually not taxed on Canada crypto capital gains.

However, if you operate a crypto-related business from within Canada, such as a mining operation, you may be considered to have a business presence here. You may then owe Canadian taxes. Cross-border CRA crypto tax rules are complex, so it is a good idea to seek advice if this applies to you.

For more information on reporting and a deep-dive into Canada crypto tax, check out Canada Crypto Tax Guide: Everything You Need to Know.

CRA Reporting and Compliance

The CRA is increasing its oversight of crypto activity. Canadian exchanges are already required to report large cash transactions and may be asked to provide customer details.

Beginning in 2026, new rules will require all crypto platforms to report transaction data and account holder information directly to tax authorities. This makes it even more important for individuals to accurately report crypto gains to CRA.

It is best to assume that your crypto activity is visible to the CRA. Failing to report your Canada crypto capital or income can lead to audits, penalties, and interest charges. In serious cases, penalties can reach up to double the tax owed and may include prosecution.

Keeping Records

The CRA has access to KYC information from crypto exchanges and mandates thorough record-keeping. For the 2024 tax year (due April 30, 2025), it's crucial to maintain accurate cost-basis tracking and complete Form T1135 if your foreign crypto holdings exceed CAD 100,000.

This is important especially when reporting Canada crypto capital gains. At a minimum, your records should include:

● The date and time of each transaction

● The type and number of units of cryptocurrency

● The value in Canadian dollars at the time of each transaction

● The purpose of the transaction, such as whether it was a trade, sale, purchase, or payment

● Details about the counterparty if available, such as the name of the exchange or the wallet address

● Wallet balances at the beginning and end of the year

You should also save receipts, trade confirmations, exchange statements, and documentation of any fees you paid. Export your trading history from each exchange regularly and keep backups in a safe place. The CRA requires you to retain all relevant records for at least six years.

Tax-Saving Tips for Crypto Investors (2025)

Although unrealized crypto gains are not taxed in Canada—simply holding your coins is tax-free—you’ll owe capital-gains tax once you sell or otherwise dispose of them. A core tactic, therefore, is to time your sales wisely: spread large disposals over multiple tax years and (where possible) route proceeds through a spousal TFSA or RRSP to stay in lower brackets or defer the tax hit.

With that foundational strategy in mind, here are several additional tips that can further reduce or defer your crypto tax bill:

1. Harvest Losses

Sell underperforming assets to offset gains. Losses can carry back 3 years or forward indefinitely. Just avoid repurchasing within 30 days (CRA’s superficial loss rule).

2. Use TFSA/RRSP

While crypto can't be held directly, crypto ETFs in TFSAs are tax-free; RRSPs defer tax until withdrawal.

3. Donate Crypto

Donations to Canadian charities give tax credits but still trigger capital gains. Long-term holdings may increase the credit amount.

4. Stay Updated

CRA crypto tax rules change often. For complex scenarios like DeFi or NFTs, consult a crypto-savvy tax expert.

5. Track Costs Accurately

Maintain detailed records of all trades and fees. Use crypto tax software to track Adjusted Cost Base (ACB) properly. It plays a key role in determining average crypto capital gains Canada for tax reporting purposes. Tools like cryptact can make things easier.

Want to dive deeper? Read our full guide on crypto tax-saving strategies in Canada to learn how to keep more of your gains while staying compliant.

FAQs

Q1. What counts as crypto capital gains Canada?

Crypto capital gains occur when you sell, trade, or spend crypto for more than you paid. The CRA treats these as taxable dispositions.

Q2. Can offset crypto losses Canada?

Yes. You can use crypto capital losses to offset capital gains. Unused losses can be carried back 3 years or forward indefinitely.

Q3. When to report crypto to CRA?

Report crypto when you sell, trade, earn, or spend it. Under CRA reporting crypto gains Schedule 3 rules, include capital gains on Schedule 3 or report income on the appropriate tax form.

Q4. Is crypto a capital gain Canada?

Crypto itself is not a capital gain, but profits from disposing of it may be taxed as capital gains or business income.

Q5. How much of crypto gains are taxable in Canada?

For individuals wondering how much tax on crypto Canada applies, 50% of capital gains are taxable. If the activity is classified as business income, 100% of the profit is taxable.

Conclusion

Canada’s crypto tax rules in 2025 continue to change, but rest on a familiar framework: crypto is taxed either as a capital gain or as income, depending on how you earn and use it.

Understanding what counts as a taxable event, how to calculate your gains, and how to report them is essential for every crypto investor or business dealing with Canada crypto capital gains.

The CRA is paying close attention to crypto, and with new reporting regimes coming, transparency is increasing. The good news is that with the right knowledge and planning, you can stay fully compliant and take advantage of tax-saving opportunities like loss harvesting and tax-sheltered accounts to keep more of your crypto profits.

Moreover, platforms like cryptact can assist in maintaining comprehensive records of your crypto transactions and estimating taxes across various exchanges. This is especially valuable when operating across multiple jurisdictions. Still, it's important to remember that automated tools should not replace professional tax advice.

No credit card required