Fact-checked and reviewed by MetaCounts.co, a Vancouver-based cryptocurrency accounting firm staffed by Chartered Professional Accountants (CPAs).

If you trade on two or more exchanges, your tax risk usually comes from record gaps, not just from gains. Most people file something, but many files break when deposits, withdrawals, swaps, and wallet transfers do not match across platforms.

This guide focuses on the practical side of multi-exchange crypto tax reporting in Canada. It shows what often triggers CRA questions, how to clean up crypto tax reconciliation, and how cryptact helps you build a file you can defend.

Key takeaways

- The CRA treats many crypto actions as dispositions, including crypto-to-crypto trades, and it expects records in CAD with clear transaction details.

- Transfers between wallets you own usually do not create a taxable disposition, but bad transfer matching often creates crypto tax reporting errors.

- Multi-exchange traders need clean ACB tracking in Canada across all holdings of the same asset, not exchange-by-exchange guesswork.

- CRA may treat high-frequency or profit-driven trading as business income, not capital gains. That shifts the inclusion rate and the reporting forms.

- The CRA asks taxpayers to keep detailed records, export exchange histories regularly, and keep records for at least 6 years.

- Canada has signaled a crypto reporting transparency push through CARF, starting with the 2026 reporting year and first information exchanges expected in 2027. CRA and Finance still shape administrative details.

No credit card required

Why multi-exchange crypto tax reporting gets harder in 2026

Canada already taxes crypto under existing income tax rules, and the CRA keeps expanding and updating public crypto guidance. The practical problem for retail traders starts when activity spreads across several exchanges and wallets. One platform shows a buy, another shows a deposit, and your wallet shows a transfer fee. If you file from only one export, your return can be processed quickly.

The CRA also expects records in Canadian dollars and asks you to use a reasonable method to determine fair market value in CAD at the time of each transaction, then apply that method consistently year over year. That means you need more than screenshots and rough memory. You need transaction-level data, timestamps, wallet addresses, and a repeatable pricing approach.

This matters more in 2026 because Canada has already signaled tighter crypto tax transparency. Budget 2024 announced Canada’s intention to implement the OECD Crypto-Asset Reporting Framework, with new obligations for crypto-asset service providers starting for the 2026 reporting year and first reporting to the CRA expected in 2027.

You can also see how broad crypto participation has become in Canada. The CSA 2024 Investor Index report says 33% of investors under 35 reported holding crypto-assets, with lower rates in older groups. More users means more filings, more mismatches, and more scrutiny on basic record quality.

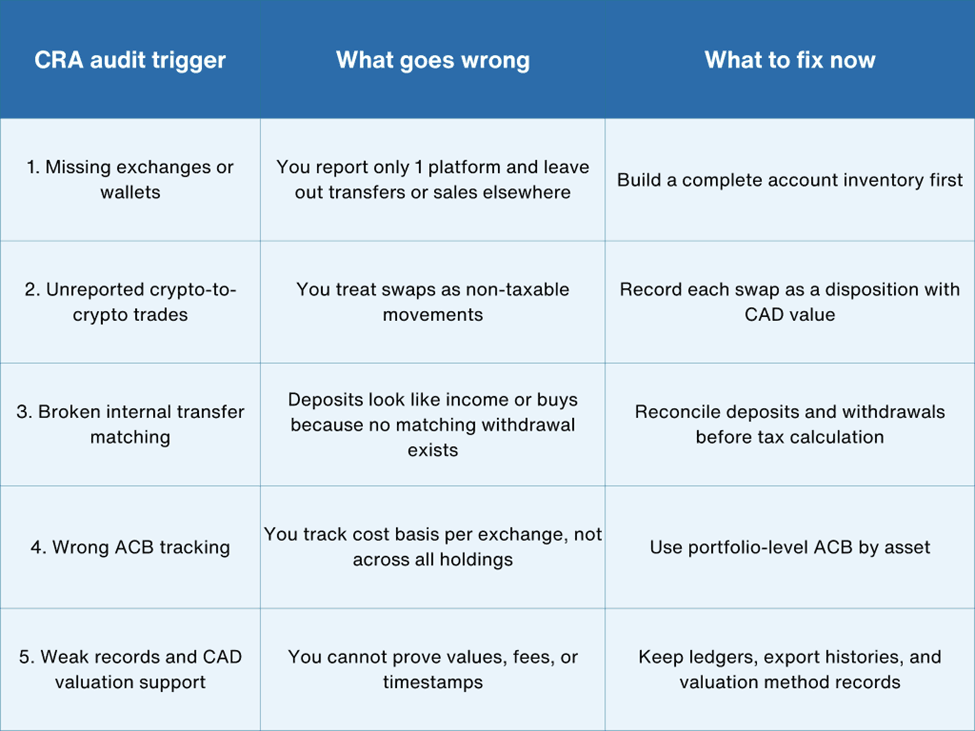

What triggers CRA crypto audit reviews in multi-exchange cases

Most CRA crypto audit stress starts with documentation gaps, classification mistakes, or broken math. In multi-exchange setups, small mistakes stack up fast because every platform exports data differently.

The table below gives you a quick view of the five biggest audit triggers in this type of file. You will see the same issues with DeFi protocols, DEX trades, bridges, and NFT platforms, not only with centralized exchanges.

1) Missing exchanges, wallets, or older accounts in your filing

This is the most common multi-exchange crypto tax problem. People report the exchange they use today and forget the one they used in January, the exchange they left after a delisting, or the wallet they used for DeFi access.

The CRA’s books and records guidance asks you to keep wallet addresses, transaction dates and times, transaction values in CAD, and beginning and ending balances by crypto asset, along with exchange trade ledgers and transfer ledgers. CRA runs the 6-year retention period from the end of the last tax year these records relate to, so you may need to keep crypto data longer than 6 calendar years.

Example (CAD):

You bought SOL on Exchange A for CAD 4,000, transferred it to Exchange B, and sold part of it there for CAD 6,100. If you report only Exchange A exports, your sale never appears. If you report only Exchange B exports, the deposit may look like an unexplained acquisition.

2) Treating crypto-to-crypto trades as non-taxable

Many traders still assume a swap only changes coins and does not create tax until they cash out to CAD. CRA guidance does not take that view.

The CRA lists trading one crypto asset for another as a disposition event. The CRA also gives a crypto-to-crypto example that calculates gain using fair market value and adjusted cost base.

The CRA’s books and records guidance asks you to keep wallet addresses, transaction dates and times, transaction values in CAD, and beginning and ending balances by crypto asset, along with exchange trade ledgers and transfer ledgers. CRA runs the 6-year retention period from the end of the last tax year these records relate to, so you may need to keep crypto data longer than 6 calendar years.

Example (CAD):

You swap BTC worth CAD 12,500 for ETH. Your ACB for the BTC you disposed of equals CAD 9,800. You likely created a capital gain of CAD 2,700 before fees and classification issues. You cannot wait until a later CAD sale to report that gain.

3) Mislabeling wallet transfers and creating fake gains or fake income

The CRA says some transactions do not result in a taxable disposition, including transfers of crypto-assets between wallets you own. This non-taxable transfer rule assumes you keep beneficial ownership. If you send coins to someone else or give up beneficial ownership through a structure, CRA can treat the transfer as a disposition. This rule helps traders, but only if your records prove both sides of the movement.

In practice, broken imports create a huge issue here. A withdrawal leaves Exchange A, then a deposit lands in Wallet B with a different token symbol format, missing hash, or timezone mismatch. Tax software or manual spreadsheets may treat that deposit as new income.

This issue drives many cases of missing crypto transactions tax confusion. The trader thinks they filed everything, but the file contains duplicate acquisitions or unexplained deposits.

Example (CAD):

You move 2 ETH from your wallet to an exchange. The exchange import shows a CAD 7,200 deposit, but your wallet export failed for that date. Your file may treat the deposit as income or a zero-cost acquisition. That error can inflate taxable gains later.

4) Tracking ACB per exchange instead of across your full holdings

ACB tracking in Canada breaks when people run separate cost basis sheets for each exchange. Canadian crypto cost basis rules do not reward platform-by-platform tracking if you hold the same asset across multiple places.

CRA crypto guidance explains capital gains using adjusted cost base, and CRA valuation guidance also stresses consistent fair market value methods in CAD.

For a retail investor on capital account, you usually need asset-level tracking across your total holdings, not just the exchange where the sale happened. CRA expects pooled ACB across identical coins regardless of platform. A per-exchange FIFO or lot-picking method will not match CRA’s pooled ACB approach for identical properties. If you split your ACB by platform, you can overstate gains on one platform and understate gains on another.

Example (CAD):

- Exchange A: Buy 1 BTC for CAD 40,000

- Exchange B: Buy 1 BTC for CAD 50,000

- Later sale on Exchange B: Sell 1 BTC for CAD 55,000

If you use Exchange B cost alone, you report a CAD 5,000 gain. If your combined ACB for 2 BTC equals CAD 90,000, your average cost per BTC equals CAD 45,000, and your gain becomes CAD 10,000 before fees. That difference matters.

5) Weak records, no exchange history exports, and no CAD valuation trail

Even a correct tax result can fail under review if you cannot support it. The CRA asks for detailed books and records and encourages electronic records. It also recommends exporting transaction records regularly because platforms can stop operating, exit Canada, restrict access, or lock you out, and waiting until tax time can mean the data is gone.

The CRA also asks you to determine values when transactions occur and use a reasonable method consistently. If you change pricing sources every month without a record, your numbers become hard to defend.

This trigger often causes crypto tax reporting errors even when the trader acts honestly. The fix starts with process, not guesswork.

How to report crypto from multiple exchanges in Canada

A clean multi-exchange filing needs a workflow. Most crypto taxes and multiple exchange problems come from doing tax calculations first and reconciliation later. Reverse that order.

Step 1) Gather your exchange transaction history for tax reporting

Start with a complete source list before you calculate anything.

Collect:

- Every exchange account you used during the year

- Every wallet you controlled

- CSV exports and API pulls for trades, deposits, withdrawals, and fees

- Records for closed accounts if you can still access them

The CRA specifically mentions trade ledgers and transfer ledgers for exchange users, plus wallet addresses and transaction details.

Step 2) Reconcile crypto deposits and withdrawals before tax math

This step answers the practical question many users ask, which is how to reconcile crypto deposits and withdrawals across platforms.

Match every outgoing transaction to an incoming transaction where possible. Use amount, asset, date/time, transaction hash, and fee differences. You will not get perfect one-click matches in every case, especially after chain bridges or exchange batching, so review exceptions manually.

Do not skip this step. It directly reduces false income entries, duplicate buys, and fake disposals.

Step 3) Classify taxable and non-taxable movements correctly

Next, label events before you calculate gain.

A common rule set for retail traders looks like this:

- Taxable dispositions often include selling for fiat, spending crypto, gifting, and crypto-to-crypto swaps.

- Non-taxable movements usually include internal wallet transfers you own, if you document both sides.

This step also answers another frequent question, which is whether crypto-to-crypto trades are taxable in Canada. In many cases, yes, CRA treats the trade as a disposition.

This step also clears up the wallet transfer tax confusion in Canada. The transfer itself may not create tax, but poor records can make it look taxable.

Step 4) Track ACB across multiple exchanges in Canada

Now calculate gains only after you complete reconciliation and classification.

Use CAD values at the transaction time and apply a reasonable method to determine fair market value in CAD for each transaction, then apply it consistently year over year.

For many retail investors, this means you track ACB by asset across your total holdings. If you sell a coin at a loss and buy the same coin again soon after, superficial loss rules can deny the loss in some cases, so track repurchases carefully. You do not isolate ETH on Exchange A from ETH on Exchange B just because the platforms differ.

This step sits at the core of crypto tax reconciliation and multi-exchange crypto tax accuracy.

Step 5) Review for common crypto tax reporting errors before filing

Run a final review before you file:

- Check for negative balances

- Check for deposits with no source

- Check for large disposals with zero or tiny cost base

- Check for duplicate imports

- Check that CAD values exist for all taxable events

Then file based on your final classification. CRA guidance says crypto dispositions can produce capital gains or business income, and the CRA decides that question case by case using facts like frequency, holding period, time spent, financing, and conduct.

What to do if you already filed with errors or missing transactions

Many traders find problems after filing. That does not always mean disaster. It does mean you should act fast and keep your records ready.

Fix the return before the problem grows

Canada’s “Change your return” page says you can request changes online or by mail, and it lists online options through your CRA account or certified tax software (ReFILE), depending on your situation.

If you discover missing crypto transactions, duplicate deposits, or ACB mistakes, rebuild the full reconciliation and ACB first. Then file one comprehensive Change your return request with supporting schedules and records, rather than sending multiple partial adjustments in separate rounds.

If a CRA crypto reassessment arrives

A CRA crypto reassessment usually means the CRA changed your assessed return after review. In practice, that can happen after data mismatches, missing support, or classification disputes.

If that happens:

- Read the reassessment details line by line

- Compare them with your transaction-level records

- Rebuild your reconciliation and ACB calculations

- Respond with organized support, not screenshots only

A clean audit trail helps more than long explanations.

How cryptact helps with crypto tax reconciliation in Canada

Multi-exchange reporting gets hard because each platform exports data differently. cryptact helps by pulling trades and transfers from multiple exchanges and wallets into one place, so you can review the full timeline before filing.

That matters for crypto tax reconciliation because you need more than a gain number. You need a defensible record flow. cryptact helps users:

- consolidate multi-exchange and wallet data

- review deposits and withdrawals to reduce transfer mismatches

- calculate gains and losses under Canadian rules using ACB logic

- keep records organized for CRA filing support

- generate tax reports you can review before filing

For people who trade often, the biggest value usually comes from clean reconciliation and consistent calculations. That lowers the chance of crypto tax reporting errors and makes corrections easier if you need to amend a return later.

Conclusion

A complete guide to multi-exchange crypto taxes in Canada starts with one rule that many traders miss. Reconciliation comes first and tax calculation comes next. If you skip account inventory, transfer matching, CAD valuation support, or ACB tracking across all platforms, you raise your CRA audit risk even when your final tax number looks close.

cryptact helps you build the file the right way. It brings together exchange and wallet activity, supports Canadian ACB-based gain calculations, and helps you generate clear records for CRA reporting. That gives you a cleaner return today and a much stronger position if the CRA asks questions later.