Fact-checked and reviewed by Kshitij Shah (BitNine), Chartered Accountant.

Crypto is now a regular asset in Indian portfolios. For the Income Tax Department, it lives in a special bucket called Virtual Digital Assets (VDAs) and is taxed through a dedicated section, 115BBH, at a flat 30% on income from transfer. On many transfers there is also 1% TDS under section 194S, which creates a clear trail in Form 26AS and AIS.

Most problems do not come from the rate itself. They come from where and how you report crypto in ITR. If AIS or exchange data shows active VDA trading and your return has no Schedule VDA or VDA income in Schedule CG, you stand out for the wrong reasons. Recent media coverage on tax action against crypto traders shows that the department is already using these trails to raise notices when gains are not reported under section 115BBH.

This guide focuses on crypto tax reporting in India for AY 2026–27 (FY 2025–26). We will use the structure of the current ITR 2 and ITR 3 (AY 2025–26) as the base, since they already have a detailed Schedule VDA and the department has said that gains from VDAs must be reported there and taxed at 30%. You should always cross-check the final notified forms for AY 2026–27, but the logic and flow are not expected to change.

Read more: For a full overview of how crypto is taxed in India, see our complete guide to crypto tax in India.

VDA tax basics for AY 2026–27

The starting point for VDA reporting in income tax return is section 115BBH. It says that when your total income includes income from the transfer of any virtual digital asset, that part is taxed at 30%, separate from your normal slab income. Only the cost of acquisition is allowed as a deduction. No other expenses, no exemptions under capital gain sections and no set-off or carry-forward of VDA losses.

On the compliance side, section 194S brings in 1% TDS on most VDA transfers above ₹10,000 in a year (₹50,000 for specified persons). Official tutorials from the department and updated guides on section 194S repeat the same basic pattern.

Putting it together for crypto tax reporting AY 2026–27:

- Income from transfer of VDAs is taxed at 30% under section 115BBH

- VDA losses are locked inside that bucket and do not reduce other income

- Many transfers leave a 1% TDS footprint under section 194S, visible to the department

The aim of your ITR is to reflect this reality clearly through Schedule VDA and linked schedules.

Which ITR form to use if you have crypto

The choice of form is the first point where people make mistakes in crypto ITR filing India.

The ITR 2 FAQ on the official portal answers the VDA question directly. It says there is a separate schedule “Schedule VDA” in ITR 2 and ITR 3 where you disclose VDA income transaction-wise and that this income is taxed at 30% under section 115BBH.

Recent guidance from tax platforms and notices explained in the media also make this clear:

- ITR 1 and ITR 4 are meant for simple situations and cannot be used when you have income from crypto or NFTs

- ITR 2 is suitable when you treat VDAs as investments and report gains as capital gains

- ITR 3 is required when your trading pattern looks like a business with high volume or organised activity

Unless CBDT announces a different structure for AY 2026–27, you can plan on this:

- Use ITR 2 when you have VDA gains as part of your capital gains and no business income

- Use ITR 3 when you have business or professional income, or you treat your crypto activity as business trading

Both forms give you access to Schedule VDA, which is where crypto tax reporting India really starts.

Where crypto and VDA income sit inside the ITR

When people search where to report crypto income in ITR, they are really asking how Schedule VDA interacts with the rest of the form.

The ITR 2 online manual explains this in one line. In Schedule VDA you add the income from transfer of virtual digital assets for each transaction. That income then auto-populates Schedule CG in item C2 – Income from transfer of Virtual Digital Assets.

Validation rules for the current ITRs reinforce the link: the total income from VDAs in Schedule CG must equal the total VDA income shown in Schedule VDA.

The flow is:

- Schedule VDA holds transaction-level details of each taxable transfer

- Schedule CG shows the total VDA income at 30% under section 115BBH

- The rest of the ITR (salary, business, other sources) handles how you first received the asset

Where do other crypto-linked flows sit?

- Salary paid in crypto still appears in Schedule Salary, based on your Form 16. The later sale of those coins appears in Schedule VDA as a transfer.

- If you run a trading desk or another crypto business, that profit is part of business schedules in ITR 3, while every disposal of a VDA is still captured in Schedule VDA.

- Gifts and airdrops above the section 56(2)(x) threshold can appear in Other Sources on receipt, and the later sale again runs through Schedule VDA.

So VDA reporting in income tax return has a simple rule: any time you dispose of a VDA for value, that disposal lives in Schedule VDA, no matter how you got the asset.

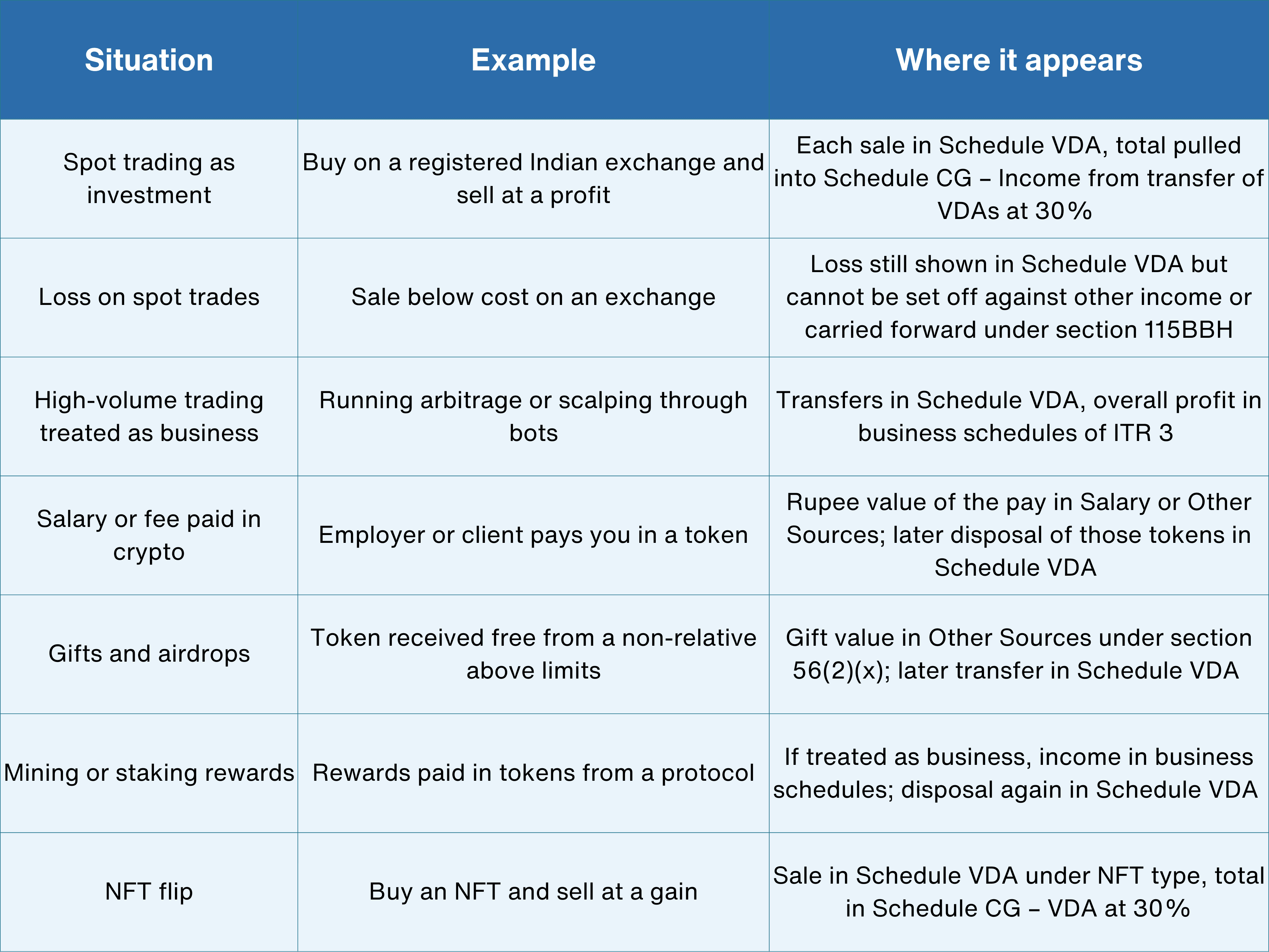

ITR schedules for common crypto situations

This table gives you a fast map of ITR schedule for crypto income in India. It reflects the AY 2025–26 design, which will likely carry into AY 2026–27 with minor updates.

It is advisable to discuss the Tax treatment with the Professional CA, but this layout keeps crypto and NFT disposals inside the VDA rail where the law expects them.

Step by step: how to report crypto trades in ITR

This is the practical flow for crypto tax reporting in India for AY 2026–27, based on the current ITR utilities and guidance.

- Collect every transaction

Export full-year CSVs from each exchange and wallet you used for FY 2025–26. Make sure you have dates, quantities, trading pairs, and INR values. Keep any TDS under section 194S handy so you can match it with Form 26AS and AIS. - Pick ITR 2 or ITR 3 on the e-filing portal

When you start the online ITR, indicate that you have income from VDAs. This step is important because it activates Schedule VDA in the form, as shown in the ITR 2 online user manual. - Fill Schedule VDA correctly

For each group of transfers, enter type of VDA, date of buy, date of sale, cost of acquisition, sale consideration and resulting income. The manual and the AY 2025–26 form layout show these exact columns. - Match TDS under section 194S

Make sure that every disposal of a virtual digital asset where 1% TDS was deducted by the exchange or the buyer is properly reflected in Schedule VDA of your return. Cross‑verify that the corresponding TDS credit is visible in both Form 26AS and the Annual Information Statement (AIS). The Income Tax Department has emphasized this linkage in its official tutorial and subsequent clarifications on Section 194S. - Review Schedule CG

Once Schedule VDA is filled, go to Schedule CG and confirm that the total under the line for “Income from transfer of VDAs” exactly equals the income total from Schedule VDA. Validation rules now treat a mismatch here as an error you must fix before filing. - Place other crypto-related income correctly

Salary, business, gifts and reward income still sit under their normal heads. Only the disposal side of any VDA based asset runs through Schedule VDA and into the 30% block. - Do a last cross-check

Compare the total VDA income in your own working file or tool with the figure in Schedule CG. This single check reduces the chance of a later notice where the department’s view of your profits under section 115BBH differs from what you filed.

For most retail traders, once this flow is clear, how to report crypto trades in ITR becomes a record-keeping problem, not a form design problem.

What if you do not disclose crypto income in ITR

Questions about what happens if you skip reporting crypto in your ITR or what penalties you might face are no longer theoretical. Recent guidance makes it clear that if you have VDA activity and leave Schedule VDA empty or incomplete, your return can be marked defective, which in practice is treated almost like not filing at all until you correct and resubmit it.

Coverage of tax action against VDA traders shows the department using exchange and bank data to find cases where traders used bots and did not disclose profits under section 115BBH or tried to offset those gains against other losses. Notices are being prepared in such cases.

On top of the tax and interest, general penalty provisions in the Act allow penalties that can go up to double the tax avoided in serious concealment cases. Independent explainers on crypto tax notices highlight this risk, especially when the form used was ITR 1 or ITR 4 even though there was clear VDA activity.

So if you have VDA trades or income:

- Do not leave Schedule VDA blank

- Do not hide VDA income inside generic capital gains without using the VDA fields

- Do not use ITR 1 or ITR 4 once crypto becomes material in your finances

It is far cheaper and safer to disclose correctly than to argue later.

Using cryptact to make ITR crypto reporting easier

All of this depends on good data. If you trade on multiple exchanges, use DeFi or move coins between wallets, keeping your own spreadsheet aligned with reality is the hardest part of crypto tax reporting AY 2026–27.

That is where cryptact comes in. cryptact is a crypto tax and portfolio tool that already supports Indian rules for VDA income and gives you a single view of trades and disposals across platforms. You can import exchange CSVs or use integrations, let cryptact classify trades and transfers, and then pull a clean report of realised gains and income in rupees.

Used this way, cryptact helps you:

- See which transactions are true disposals that must go into Schedule VDA

- Get cost, sale value and profit in INR for each disposal without manual math

- Check that the sum of your reported VDA income matches the totals in your own records before you file

That means your ITR work becomes structured: first, make sure cryptact has every trade, then fill out Schedule VDA and the rest of the form based on that output, and finally match it with the TDS and AIS view. For AY 2026–27, the safest approach for Indian crypto users is to treat VDAs as a separate 30% track, keep that track clean all year, and let tools like cryptact turn raw transaction history into numbers the Income Tax Department already expects to see.

No credit card required