Fact-checked and reviewed by Kshitij Shah (BitNine), Chartered Accountant.

In India, individual taxpayers must report and pay taxes on gains from virtual digital assets (VDAs). VDAs include popular cryptocurrencies like Bitcoin or Ethereum as well as other digital assets such as NFTs.

This article breaks down the crypto tax rules in simple terms. The goal is to help you understand and comply with the crypto tax provisions in India…without wading through legal jargon!

So, let’s dive in.

No credit card required

What Qualifies as a Virtual Digital Asset (VDA)?

Under Indian tax law, “Virtual Digital Asset” (VDA) is a broad term introduced in 2022 to classify crypto assets for tax purposes.

According to Section 2(47A) of the Income Tax Act, a VDA essentially means any digital representation of value that is generated through cryptographic means (or otherwise) and can be traded or transferred electronically.

In simple terms, all types of cryptocurrencies, crypto tokens, and non-fungible tokens (NFTs) are considered VDAs. Notably, the definition excludes official fiat currency (like the Indian rupee or foreign currencies). It also excludes certain digital items like gift cards or vouchers.

Flat 30% Tax on Crypto Gains (Section 115BBH)

Profits from the transfer of any VDA (crypto or NFT) are subject to a flat 30% rate in India. This rule was introduced in the Union Budget 2022 via Section 115BBH of the Income Tax Act. It remains in force for FY 2025–26.

The 30% tax applies uniformly to all crypto gains. This is regardless of whether you held the asset for a short term or long term, or whether you’re a casual investor or a professional trader. On top of this, an applicable surcharge (based on your total income slab) and a 4% health & education cess are added.

For high-income individuals, surcharges can range from 10% to 25% or more. So, the effective tax on crypto gains ends up being slightly higher than 30%.

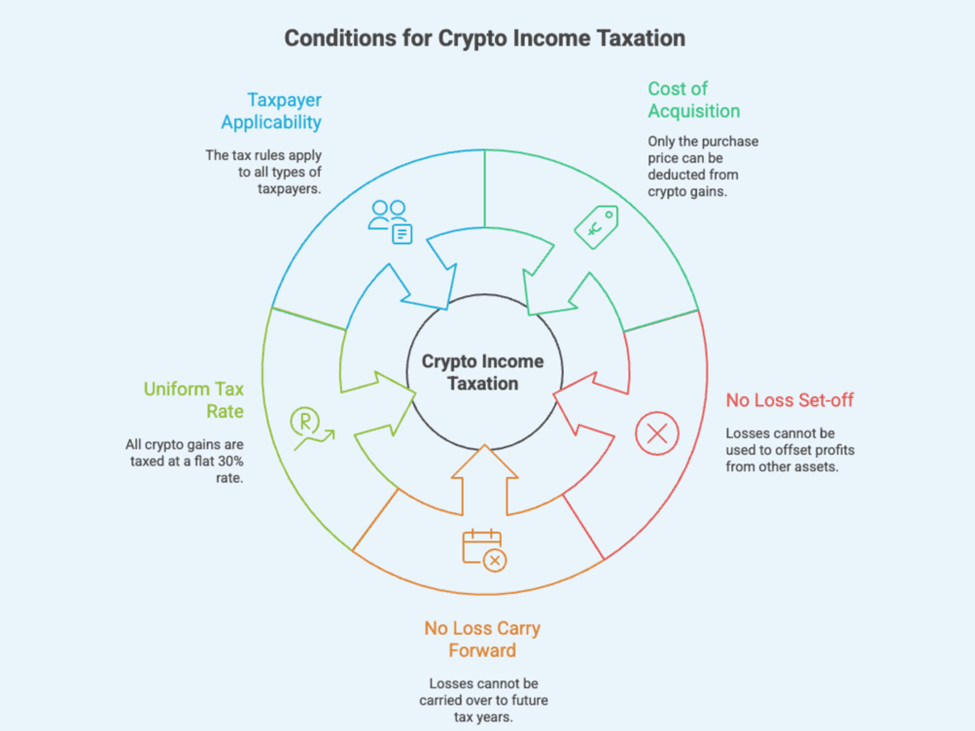

Section 115BBH – Key Conditions for Crypto Income

Section 115BBH also lays out special conditions on deductions and losses for crypto income:

No Deductions Except Cost of Acquisition: When calculating your taxable crypto income, you are only allowed to deduct the cost of acquiring the asset. No other expenses can be deducted. This means costs like exchange fees, broker commissions, transaction charges, mining infrastructure costs, etc. cannot be subtracted from your crypto gains for tax purposes. Essentially, Taxable Income = Selling Price – Purchase Price.

No Set-off of Losses: Incurred a loss on one crypto asset? That loss cannot be set off against profit from another crypto asset or any other income.

No Carry Forward of Losses: Furthermore, a crypto trading loss in a financial year cannot be carried forward to the next year for set-off. Each year’s crypto losses lapse. Only the gains are taxable.

Same Rate for All Holding Periods: Both short-term and long-term gains on crypto are taxed at 30%. There are no indexation benefits or reduced rates even if you held the crypto/NFT for several years.

Applies to All Types of Taxpayers: The 30% crypto tax rule applies whether you treat the income as capital gains or business income. Even businesses or frequent traders pay the same rate on VDA profits.

No Set-off or Carry Forward of Crypto Losses

One of the most crucial rules for crypto investors is the treatment of losses. Under the crypto tax provisions, you cannot offset losses from one VDA against gains from another, nor against any other income. Each crypto trade’s profit is taxed in isolation.

Additionally, crypto (VDA) losses cannot be carried forward to future years. In many cases for other assets, if you can’t use a loss in the same year, you might carry it forward to offset future gains. But crypto losses are fully disregarded for tax purposes beyond the year. They can’t shelter future crypto profits or any income in later years.

1% TDS on Crypto Transactions (Section 194S)

To capture tax at the source and track crypto transactions, the government introduced Section 194S. It imposes a 1% TDS (Tax Deducted at Source) on payments made for the transfer of VDAs.

In practice, whenever you sell or transfer cryptocurrency, the party paying you (often the exchange or buyer) will deduct 1% of the sale consideration as TDS. They then remit it to the government.

This 1% TDS applies only if your total crypto transactions exceed a certain threshold in the financial year. The thresholds are:

₹50,000 per year for “specified persons”, typically meaning individual/HUF taxpayers who are not required to audit their accounts (generally regular individuals).

₹10,000 per year for other taxpayers (such as those with business turnover above certain limits or companies).

Who deducts TDS, and how? If you trade on an Indian crypto exchange, the exchange will usually handle the 1% TDS deduction on your sell orders automatically. For peer-to-peer trades or using foreign exchanges (which may not deduct Indian TDS), the responsibility to deduct 1% lies on the buyer (the person paying).

The TDS is not an additional tax on top of the 30%. Think of it as an advance tax. You can claim the amount of TDS deducted as credit against your final tax liability when you file your income tax return.

Taxation of Crypto Gifts, Airdrops, and Mining Rewards

Cryptocurrency received as a gift or through other means (not purchase) can also attract tax, albeit under different provisions:

Gifts of Crypto/VDAs: If you receive cryptocurrency or NFTs as a gift (for example, someone transfers coins to you for free), it can be taxable in your hands as the recipient.

Under Section 56(2)(x) of the Income Tax Act, gifts from non-relatives exceeding ₹50,000 in a year are taxable as “Income from Other Sources”. The entire fair market value of the crypto gift is counted as income if it crosses the ₹50k threshold. Such crypto gifts are taxed at your normal income tax slab rates (not at the flat 30%, because this is not a gain from transfer).

For instance, if a friend gives you crypto worth ₹1 lakh, you may need to pay tax on ₹1 lakh at your applicable slab rate in that year. (Gifts from specified relatives or on certain occasions like marriage remain exempt, and gifts totaling up to ₹50,000 in a year are ignored for tax).

Airdrops and Mining Income: Airdrops, staking rewards, mining rewards, or crypto earned from providing services are treated similarly to gifts.

These are instances where you acquire coins without paying for them, so the fair market value at the time you receive them is taxable as ordinary income (income from other sources or business income) at your slab rate.

Subsequent Sale of Gifted/Earned Crypto: If you sell or transfer crypto you received as a gift or mining reward, any gain from the sale will be subject to the 30% tax under Section 115BBH. Essentially, there are two stages of taxation.

The first is at receipt (as other income, at slab rates). Next, it’s on any increase in value when you sell (as crypto capital/business income at 30%).

For the purpose of computing the 30% tax when you sell, you can consider the cost of acquisition as the amount that was taxed as gift/income when you received it. So, you’re not double-taxed on the same value. Only the appreciation from that point to the selling price would be taxed 30%.

Crypto Income: Capital Gains vs Business Income

Cryptocurrency transactions by individuals can be classified either as capital gains or business income depending on the nature of activity. Indian tax law allows both treatments for VDA income, but the tax rate outcome remains the same due to Section 115BBH:

Capital Gains: If you invest in crypto as a capital asset, then profits when you sell are treated as Capital Gains. Many individual crypto investors fall into this category. Even though ordinarily we might distinguish between short-term and long-term capital gains (with long-term potentially enjoying lower tax rates for some assets), for crypto the distinction is only nominal. If you have crypto capital gains, you will select capital gain head under Schedule VDA in your tax return.

Business Income: If you are trading cryptocurrencies frequently or your activities resemble a business, you can classify the income under “Profits and Gains from Business or Profession”. This might apply to, say, a day trader in crypto, someone running a crypto trading business, or even crypto miners treating mining as a business.

In such cases, you’d normally prepare a profit and loss account for the crypto trading activity. However, even as business income, the tax rate on VDA profits is mandated at 30%. Also, no business expenses (other than cost of the assets) can be deducted against crypto trading income. However, reporting under Schedule VDA is still mandatory by selecting the Head of income as “Business”.

Other Sources: As noted earlier, if your crypto was received as a gift or via mining/airdrop, at the point of receipt it may fall under “Income from Other Sources”. That is a separate head of income, taxed at slab rates for that initial value.

From a tax filing perspective, the classification affects which ITR form and schedule you use. However, it does not change the tax rate.

If treating crypto profits as capital gains, you should use ITR-2 (provided there is no income from business or profession from other activities) and report the gains under the Schedule VDA (Virtual Digital Assets) in return. If treating them as business income, you should use ITR-3, and report under the Schedule VDA.

For most casual investors who occasionally trade, the capital gains route (ITR-2) is appropriate. On the other hand, heavy traders or those who have registered for a trading business might opt for business income reporting (ITR-3). In all cases, the income details (sales, costs, profits) must be declared and the 30% tax is computed.

Reporting Crypto Income in the Income Tax Return

In recent years, the Indian Income Tax Return forms have been updated to capture crypto transactions separately.

For AY 2025 (FY 2024-25), taxpayers need to report their VDA income in a dedicated schedule in the ITR called “Schedule VDA” (Virtual Digital Assets). This schedule requires details of your crypto gains, similar to how you report stock or property sales, but tailored for VDAs.

Filling the Schedule VDA is straightforward once you have the numbers: list your total sale value, subtract the cost of acquisition (no other costs), and 30% tax gets applied on the resulting profit.

Remember, failure to report crypto income or TDS properly can attract penalties. The tax department is actively using TDS data and other analytics to identify unreported crypto gains.

Choose the Correct ITR Form

If you only had crypto gains (and no business income), you will likely file ITR-2 (since crypto gains are capital gains in this context). If you have crypto income classified as business income or you are a trader/miner with business, use ITR-3.

In both forms, a Schedule VDA is where the crypto details go. Ensure to download the latest ITR form for AY 2025 which includes this schedule.

Provide Details of Each Transfer

You may need to specify for each type of VDA transaction the sale consideration, cost of acquisition, and resulting profit. The Schedule VDA typically asks for such breakdown, possibly segregated by each VDA or each transaction category.

Maintain a summary of your trades to fill this accurately (many people use crypto portfolio trackers or exchange statements to get this info). This is where a tool like cryptact can help you.

Report TDS and Pay Remaining Tax

Include any TDS (1% deductions) in the appropriate TDS schedule of the ITR (often TDS on income other than salary). For example, if ₹5,000 TDS was deducted by exchanges, report that so that it is credited against your tax liability.

After computing your total tax (30% on crypto gains plus tax on any other income), ensure that the TDS credit is subtracted and pay off any balance tax due before filing. The 30% tax on crypto is not a separate tax you must pay later. It gets calculated as part of your total income tax when filing.

Keep Records

Although not part of the return itself, keep records of your crypto purchase and sale dates, values, and receipts of any gifted coins. In case of any scrutiny or mismatch (for example, the tax department does cross-check your reported income with TDS and exchange data), having a paper trail will help.

The government is strengthening reporting requirements and even crypto exchanges will be mandated to report transactions moving forward, so transparency is important.

Conclusion

The crypto tax rules in India for individual taxpayers (AY 2025) can be summarized as a strict, flat regime: 30% tax on any crypto profits, no adjustment for losses, and 1% TDS on transactions to keep a check on compliance.

Virtual Digital Assets like cryptocurrencies and NFTs are firmly under the tax net, treated akin to high-value speculative investments. While the tax rate is high, the rules are now clear-cut. This helps in planning your finances.

To avoid any trouble, ensure you report all crypto-related income in your ITR under the correct sections and pay the due tax. Gifts of crypto and coins earned via mining or airdrops carry their own tax steps (taxed upon receipt, then taxed on sale), so pay attention to those events as well.

Understanding these provisions and keeping good records, you can participate in the crypto market while staying fully compliant with Indian tax laws.