Fact-checked and reviewed by Kshitij Shah (BitNine), Chartered Accountant.

Investing in cryptocurrency, or “Virtual Digital Assets” (VDAs) as they’re called in India, comes with tax rules that can seem complex and overwhelming. To help you navigate this, this article will focus on three fundamental rules every investor should know.

First, there’s a flat 30% tax on all crypto gains, commonly referred to as the 30% crypto tax India. Second, there’s a 1% TDS on most crypto transactions. Third, you have no ability to offset any crypto losses against gains or other income, as specified under the crypto tax section 115BBH.

These rules came into effect from the 2022 fiscal year and remain in force in 2025. In simple terms, the government taxes your crypto profits heavily (similar to lottery or gambling winnings). It then ensures compliance by tracking transactions through TDS.

We’ll break down each component of these rules in an easy, conversational way so you understand how crypto is taxed in India and how to stay compliant. If you want a complete guide to crypto taxes in India, be sure to explore Crypto Tax in India: A Comprehensive Guide.

Read on to find out more.

Table of contents |

No credit card required

Understanding the 30% Crypto Tax India

Let’s start with the most important part. Any profits you make from trading or investing in crypto are taxed at a flat 30% in India. This rate was introduced in the Union Budget 2022 and treats crypto profits akin to winnings from lottery or game shows (which also attract a flat tax).

In other words, the 30% crypto tax in India applies no matter how long you hold your crypto: whether it’s just a day or a whole year. Also, it doesn’t matter what your income bracket is. Any gains you make when you sell or spend your crypto are subject to 30% crypto tax India.

For example, if you bought some crypto for ₹1,00,000 and later sold it for ₹1,50,000, the ₹50,000 profit is taxed at 30%. You would owe ₹15,000 as tax (plus applicable surcharge and 4% health & education cess) on that gain.

Furthermore, there are no slab benefits or long-term rates. Unlike stocks or mutual funds, there is no distinction between short-term and long-term holdings for crypto.

Even if you held crypto for more than 36 months, it doesn’t qualify for any lower tax rate. The gain is still taxed at 30%. The income is not treated as a capital asset gain eligible for reduced rates. In fact, it’s taxed under a special provision (crypto tax Section 115BBH) as “other income” at a flat rate. The government has categorized crypto gains in the same bucket as speculative income.

An additional point to note is about crypto derivatives. While profits generated from derivative trades are taxable in India, the Income Tax Department has not clarified which tax type applies. Such income could fall under the flat 30% regime or be taxed under the progressive income tax brackets. Because of this uncertainty, it is strongly recommended that you consult your own accountants for specific guidance if you engage in crypto derivative trading.

Here’s an important point to remember: only the cost of acquisition is deductible. So, when calculating the taxable crypto gain, you are only allowed to deduct the cost of acquiring the asset (i.e. the purchase price) from the sale price. No other expenses can be deducted, including exchange fees, broker commissions, internet costs, mining expenses, or any other related costs.

For instance, if you spent ₹1,000 in transaction fees while trading, you still cannot subtract those fees from your profit for tax purposes. This rule, specified in crypto tax Section 115BBH, makes the taxable income essentially the full gain. Moreover, it is without any relief for costs apart from buying the asset.

Why a 30% Flat Tax?

A lot of people ask, why crypto taxed at 30% India? The reason crypto gains are taxed at 30% in India is largely policy-driven. The government views crypto trading profits as windfall or speculative gains, similar to lottery wins or betting income, which have a high tax rate. Taxing crypto at a high flat rate, authorities aim to deter reckless speculation and also capture revenue from an activity they consider high-risk.

It’s a strict regime, so how crypto gains are taxed at 30% in India is non-negotiable. Any profit you make in crypto is subject to this rate regardless of circumstances.

Now that you know how the gains are taxed, let’s talk about one of the tougher rules — what happens with your losses.

Can You Offset Crypto Losses Against Gains?

A common question is, can crypto losses offset other income India? Unfortunately, under current Indian tax laws, you cannot do so.

One of the most “tough” rules for investors is the crypto loss set off rule India. As per the rule, you cannot offset crypto losses against crypto gains or any other income. This is outlined in crypto tax Section 115BBH: if you suffer a loss on one VDA (say, one cryptocurrency), that loss cannot reduce the tax on a profit from another VDA.

Each crypto transaction’s result is treated in isolation for tax. So, you pay 30% on profits, and losses are simply disregarded for tax purposes.

Here’s the no loss set off on crypto rule explained with a simple example:

Suppose you made a ₹1,00,000 profit on Bitcoin but in the same financial year you lost ₹50,000 on Ethereum. Normally, one might expect to net these and pay tax on the ₹50,000 net profit.

However, under India’s crypto tax rules, you still have to pay tax on the full ₹1,00,000 profit from Bitcoin and the Ethereum loss is not allowed to offset that gain. You’d owe ₹30,000 (30% of ₹1 lakh) in tax on the Bitcoin profit, and the ₹50k loss on Ethereum won’t save you any tax. It’s essentially not recognized for tax relief, as outlined by the crypto loss set off rule India.

Furthermore, crypto losses cannot be carried forward to the next year either.

In stock trading or other capital gains, if you can’t use a loss in the current year, you often can carry it forward to offset future gains. That’s not allowed with crypto. A loss from crypto trading in FY 2024–25, for example, dies in that year itself, and you can’t use it in later years.

You also cannot offset crypto losses against other income like salary, interest, property income, etc.

All of this means a crypto investor has to “eat” the losses entirely on their own, while still paying taxes on any winners.

What’s the 1% TDS on Crypto Transactions in India?

India’s crypto tax policy also introduced a Tax Deducted at Source (TDS) of 1% on every crypto transaction (above certain thresholds) to help the government track trading activity.

What is this 1% TDS on crypto? In practice, when you sell or trade crypto, 1% of the transaction value is cut as TDS and remitted to the government. This started from July 1, 2022, and applies whether you’re selling crypto for INR or swapping one crypto for another.

Crucially, the 1% TDS is on the total amount of the transaction, not on your profit. Even if you sell at a loss, that 1% still gets deducted on the sale price. For example, if you sell crypto worth ₹1,00,000 (regardless of your gain or loss), ₹1,000 will be taken as TDS. It’s essentially an advance payment for crypto trading tax India 2025.

Who Deducts the TDS?

Typically, if you use an Indian crypto exchange, the exchange will automatically deduct the 1% TDS on your behalf. This will be at the time of transaction. You might have noticed when you sell crypto on an exchange, you receive slightly less than the sale price. That difference includes the TDS being withheld.

If you use a peer-to-peer (P2P) platform or an international exchange, the responsibility to deduct and deposit the 1% TDS technically falls on the buyer (or on you, if you’re the buyer).

In such cases, compliance can be tricky. You would need to file a TDS return (Form 26Q/26QE) and pay that 1% to the government yourself. Many everyday users aren’t aware of this, which is why the government encourages using regulated Indian exchanges which handle TDS automatically. This helps avoid penalties for crypto under-reporting in India.

Thresholds – Small Traders vs Others

To ease the burden on small traders, the law sets certain thresholds for when the 1% TDS applies. This means that not everyone has to worry about TDS on tiny crypto transactions.

For individuals classified as “specified persons” (generally, those with small or no business income in the previous year), 1% TDS is only required if your total crypto trades exceed ₹50,000 in a financial year. But for other taxpayers (including companies or individuals with higher income/business turnover), the threshold is much lower. TDS kicks in once transactions exceed ₹10,000 in a year.

In simpler terms, if you’re a casual salaried person doing modest trading, the 1% TDS might not apply until you cross ₹50k worth of sales in a year. However, most regular crypto investors do cross these limits quickly. As a result, practically almost every sale or trade gets hit by the 1% TDS for active traders.

Also note, if you haven’t been filing your tax returns despite having TDS, the government can increase the TDS rate to 5% under certain conditions as a penalty (per Section 206AB). It’s yet another incentive to stay compliant with crypto trading tax India 2025.

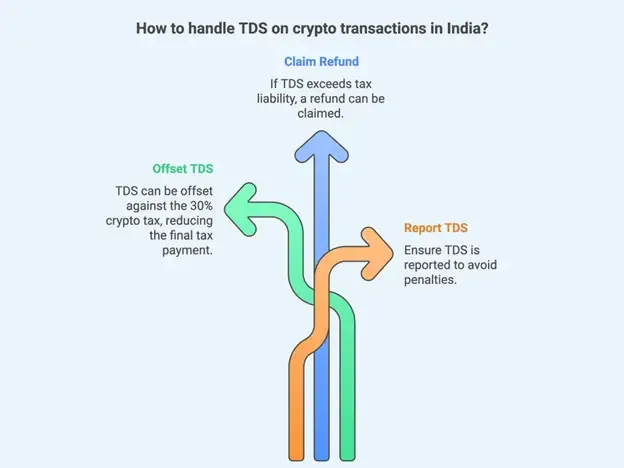

How TDS is Adjustable Against Tax Liability

Many investors wonder, can TDS be offset against 30% crypto tax India? The good news is that the 1% TDS is not an extra tax on top of the 30%. Rather, it’s a prepaid tax that can be offset against your final tax bill. When you file your Income Tax Return, all the 1% TDS amounts that were deducted throughout the year are credited against the total tax you owe.

For example, if over the year you sold various crypto and ₹10,000 was deducted in total TDS, and suppose your 30% tax on your crypto gains comes to ₹50,000, you would only need to pay the remaining ₹40,000 (because ₹10k was already paid via TDS).

So, yes, TDS can be offset against the 30% crypto tax India. It appears in your Form 26AS/Annual Information Statement and you claim that credit. If your total TDS deducted exceeds your tax liability (say you ended up with losses or minimal net gains), you can even get a refund of the excess TDS by filing your tax return. Therefore, make sure to report the TDS in your return to get credit for the 1% TDS and reduce your final tax payment.

Reporting TDS and Compliance

If you are doing P2P trades and responsible for TDS, you must obtain a Tax Deduction Account Number (TAN) and file the required TDS statements (Form 26Q/26QE) on time.

For most people trading on exchanges, the exchange provides TDS certificates or statements. So you can know how much was deducted. Always double-check that these TDS deductions reflect in your Form 26AS (tax credit statement). The tax department is cross-verifying crypto transactions via TDS reports, so it’s important not to ignore this.

You might also ask, what if TDS fails on transactions in India? In such cases, you will have to deduct and report it properly yourself. Unfortunately, if you fail to do so, you will have to face a penalty. Section 271C of the Income Tax Act can impose a penalty equal to the amount of TDS you didn’t deduct.

With that, let’s briefly look at reporting your crypto income in your tax return.

How to Report Your Crypto Income in Your Tax Return

All crypto gains must be reported in your Income Tax Return. For FY 2024-25, individual taxpayers who have crypto transactions will typically use the ITR-2 form (since you have capital gains; ITR-1 cannot be used for crypto gains).

The tax department has introduced a specific Schedule VDA in the ITR forms to declare crypto income in detail. When filing your return, you need to ensure you’re reporting crypto on ITR-2 VDA schedule. You’ll need to check the option for Schedule VDA and enter your crypto transaction details. The schedule may ask for information transaction-wise, such as date of acquisition, date of sale, purchase cost, and sale value for each VDA transaction.

Essentially, the government wants a breakdown of your crypto trading activity to ensure accurate taxation.

How to File Crypto Tax in ITR-2 (FY 2024-25)

The process is integrated into the normal online ITR filing. Once you select ITR-2 and indicate you have income from Virtual Digital Assets, the form will include Schedule VDA. You will list each disposal of crypto assets.

For example, if you sold Bitcoin and Ether during the year, each sale would be a line item with its buy cost and sale price. The form then computes how crypto gains taxed at 30% India apply to the net gains from each transaction. Make a note not to report crypto gains under regular capital gains schedules. They have to go into Schedule VDA specifically (the software/portal usually guides this). If you have multiple trades, it can be a bit tedious to input, but it’s necessary for compliance.

Keep in mind that reporting crypto on ITR-2 VDA schedule is mandatory from AY 2023-24 onwards. The tax department has been sending “nudges” and notices if taxpayers who likely had crypto transactions (as evidenced by TDS or exchange data) fail to report them properly. So ensure you fill out this section.

Also make sure you double-check the figures with your exchange statements. It’s also advisable to use a crypto tax calculator to summarize your trades, since it helps avoid penalties for crypto under-reporting in India.

Cryptact is one such tool. It helps you gather your transaction records and calculate your profits and losses. They also generate detailed tax reports specific to Virtual Digital Assets (VDAs). This makes the often complicated process of crypto tax filing much simpler. This is especially helpful if you’ve traded on multiple exchanges, used DeFi platforms, or made many transactions throughout the year.

For a detailed look at how to file crypto tax ITR-2 FY 2024-25, check out our guide.

Final Thoughts

Crypto taxation in India boils down to this: 30% tax on profits, 1% TDS on transactions, and no breaks for losses under crypto tax Section 115BBH. It’s a tough policy for traders, especially during bear markets or frequent trading, but it’s the law of the land as of 2025.

Make sure you factor in these taxes whenever you trade, or your net returns will be affected. The silver lining is that the rules are clear-cut. Furthermore, if you comply diligently (report in Schedule VDA, keep track of TDS, etc.), you can avoid any issues with the tax authorities.

Always consult with an advisor if you’re unsure, especially if you have significant crypto holdings. Paying 30% crypto tax India on your gains might feel like a lot, but it’s far better than facing 60% tax and heavy crypto tax penalty India for non-compliance.

So stay informed, keep records of your trades, utilize tools such as cryptact, and file those crypto taxes actively. With that, you’ll fulfill your obligations and can focus on your investments with peace of mind.