Fact-checked and reviewed by Kshitij Shah (BitNine), Chartered Accountant.

Crypto in India now sits under three layers of tax: a 30% flat tax on gains from virtual digital assets, 1% TDS on many transfers, and 18% GST on a wide range of platform and service fees. From 2025 onward, crypto GST is no longer a vague idea. Indian exchanges clearly charge GST on their fees, and several offshore platforms that target Indian users have also started adding 18% GST for them.

This article is a detailed GST guide for cryptocurrency users in India. It explains how GST looks at crypto, where it actually applies in your day-to-day activity, what the current GST rate on crypto in India means in practice, and how you can stay compliant without turning this into a full-time commitment.

Read more: For a full overview of how crypto is taxed in India, see our complete guide to crypto tax in India.

Table of contents |

Where GST Places Crypto Today

The first question many people ask is: “is crypto under GST in India or only under income tax?"

Under the Income Tax Act, virtual digital assets (VDAs) are a separate asset class. They are not Indian or foreign currency, but they are recognised as property that can be bought, sold and taxed. That definition includes cryptocurrencies, many tokens and certain NFTs. For GST, money and securities sit outside the tax base. Since VDAs are not money and not securities, most tax writers now treat GST on virtual digital assets as falling under normal rules for goods and online services.

In simple terms:

- Tokens themselves are treated like movable or intangible property when supplied by a business.

- Services around tokens – exchange platforms, broker apps, wallets, staking or lending platforms are treated as online services that attract 18% GST on their fees.

So, GST rules for cryptocurrency in India do not tax the act of holding coins in your wallet. GST appears when there is a supply of a service or when a GST-registered person supplies tokens as part of their business activity.

How GST Applies to Common Crypto Activities

If you want to understand how GST applies to cryptocurrency in India, it is easier to break it down by activity than by sections of law.

Common activities and GST treatment

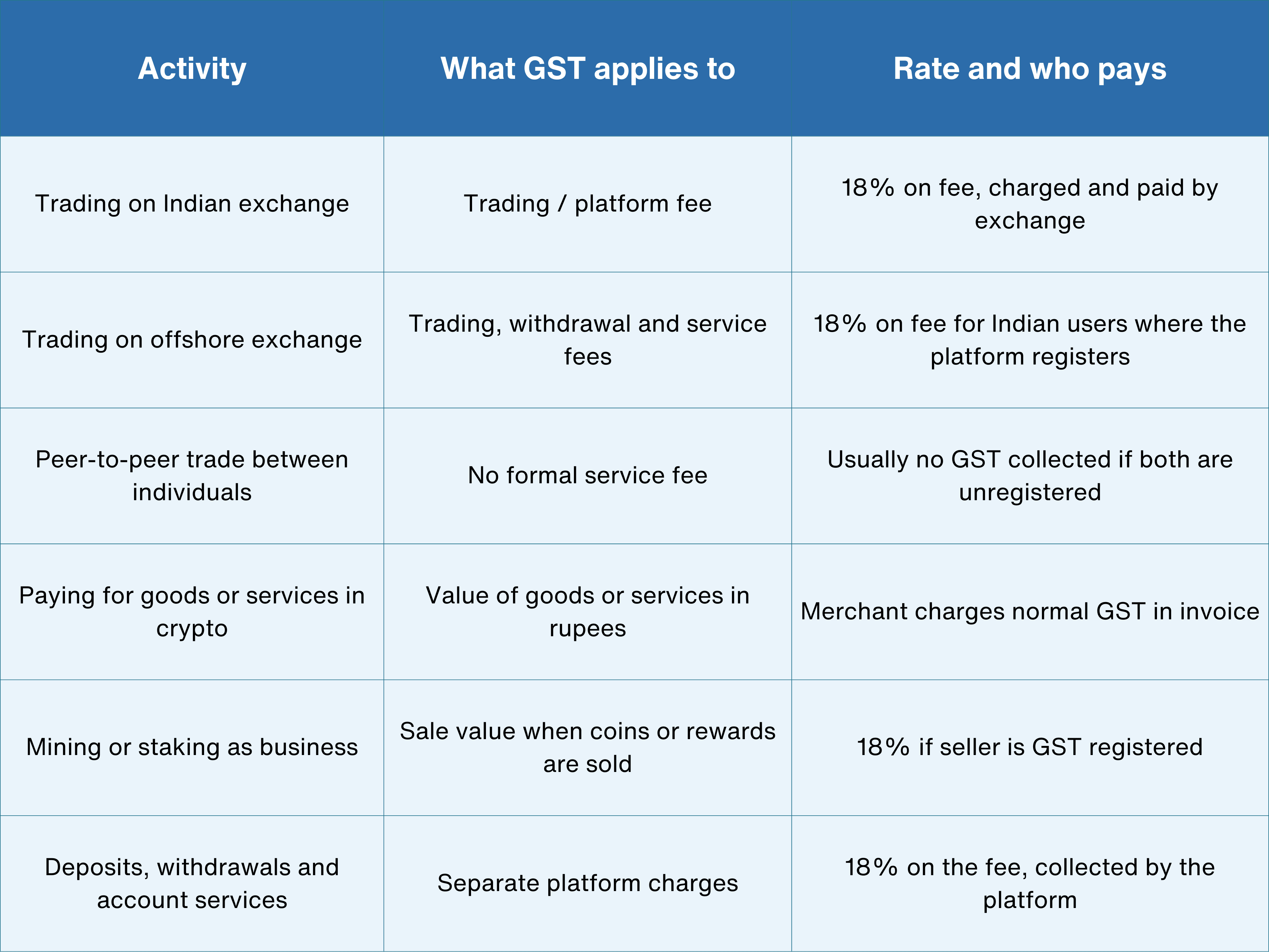

Trading on Indian Exchanges

For most users, GST on crypto trading shows up first in the trading fee. If you are on an Indian exchange, trading, withdrawals, and account fees are treated as taxable online services. 18% GST applies to the fee amount. You pay the fee plus GST to the exchange, and the exchange files and pays that GST in its returns.

For example: You sell coins worth ₹1,00,000. The exchange fee is 0.2%, or ₹200. GST at 18% on the fee is ₹36. You pay ₹236 total as charges. The exchange books ₹200 as revenue and ₹36 as GST liability.

The crypto itself that moves between you and another user does not have a separate GST line if both of you are private individuals trading on your own.

Trading on Offshore Exchanges

Many Indian users also use global platforms. When a foreign exchange or app registers for Indian GST and charges fees to Indian users, those fees also carry 18% GST. That is why you may now see a separate tax line on some foreign platforms – this is still GST on cryptocurrency in India, just collected by an overseas company that has registered for India.

If a foreign platform has not registered but you are a GST-registered business using it, reverse charge rules can apply on those imported services. Retail investors who are not registered do not usually deal with this, but businesses do.

Peer-to-Peer Trades

In pure wallet-to-wallet P2P transfers (you send crypto directly to another person and no platform/escrow fee is charged), there is usually no separate ‘service fee’ supply being made for consideration. GST is generally triggered when there is a supply for consideration in the course or furtherance of business. So, a one-off transfer between individuals (not acting as a business) typically does not create a GST invoice event by itself.

However, the moment a platform is involved (P2P marketplace, escrow, matching, brokerage, custody) and it charges a commission/convenience fee, that fee is treated as a taxable service, and platforms commonly levy 18% GST on the fee component (not on the crypto value).

If the fee is paid to a foreign platform, it can fall under import of services concepts; GST responsibility depends on the recipient profile and the specific rules for cross-border online services.

The risk starts when volumes and behaviour begin to look like a business. If someone runs an informal OTC desk, does high-frequency sales and crosses the turnover threshold, authorities can argue that they should have registered and treated those sales as taxable supplies.

Paying for Goods or Services in Crypto

If you pay a designer, consultant or store in Bitcoin or another coin, the tax question is how GST treats that payment. For the seller, nothing changes in their duty. They still issue an invoice in rupees for the product or service and charge GST at the normal rate for that item. Crypto is just the mode of payment. The sale does not fall outside GST simply because you used coins.

For example:A consultant charges ₹20,000 plus 18% GST for a project, so the invoice total is ₹23,600. You pay the rupee equivalent in crypto. The consultant still reports ₹20,000 as taxable value and ₹3,600 as GST in their returns.

Mining and Staking

When you mine coins or earn staking rewards, there is usually no identifiable recipient paying you at that moment and no clear consideration being paid by a customer for a specific supply. Under GST, tax generally hinges on a supply for consideration in the course or furtherance of business. That is why the receipt of block rewards/staking rewards is commonly viewed as outside GST in many retail scenarios.

GST becomes more relevant when you are clearly providing a service for a fee, such as staking-as-a-service, validator services for others, mining hosting, custody, brokerage, or platform facilitation (where a commission/service fee is charged). In those cases, the fee/commission portion is typically treated as a taxable service and often taxed at 18%.

For the sale of the mined/staked crypto itself, GST treatment can vary depending on whether the activity is treated as a business supply and how the asset/service is classified, so it should be framed as fact-specific rather than a flat 18% applies.

Deposits, Withdrawals and Extras

Many platforms charge separate fees for deposits, withdrawals, or special account services. Those charges sit inside GST on crypto service fees and GST on crypto deposits and withdrawals in India. They are straightforward online services, and 18% GST applies to the fee part, either shown separately or included in the price.

GST Rate and Who Carries the Burden

There is no special slab that only applies to crypto. Right now, the working GST rate on crypto in India is:

- 18% on services from exchanges, brokers, wallets and similar platforms

- 18% on taxable token sales by GST-registered sellers, treated as supply of goods or digital assets

In other words, GST for crypto exchanges uses the same 18% rate that applies to many other online services. The economic burden sits with users through slightly higher costs, but the legal duty to collect and remit that GST sits with the exchange or business that issues the invoice.

For a normal investor, crypto GST tax in India is 1 more line in the cost structure, along with the 30% income tax on net gains and the 1% TDS on many transfers. GST is baked into the fee; you normally do not file a separate GST return only because you traded on your personal account.

Compliance Basics for Users and Exchanges

Exchanges and Platforms

On the platform side, GST applicability on crypto is now very real. Indian exchanges are expected to register under GST, charge 18% on eligible fees, and keep clean records of what they charged, what GST they collected, and what they paid to the government. Enforcement actions against both Indian and foreign-linked exchanges in the last few years show that GST on crypto services is being actively monitored, not just discussed.

Because many exchanges are also registered as reporting entities under anti-money-laundering rules, their data can be compared across GST, income tax and FIU systems. That makes under-reporting harder to hide.

Users, Traders and Businesses

For users, the question does GST applies to crypto transactions in India depends on your role.

- If you are a retail investor trading with your own money, you do not register for GST simply because you hold or trade crypto. Your GST exposure is mostly in the platform fees that already include tax.

- If you run an OTC desk, project, or structured trading business, your rupee turnover from selling tokens can count toward GST registration thresholds. In that case, there can be GST on those token sales as well.

- If your business accepts crypto as a form of payment for services or goods, you still raise invoices in rupees and charge GST at the regular rate for those supplies.

- If you are already GST-registered and you pay large fees to offshore platforms, reverse charge may apply on those imported online services.

Best Practices for 2025 and Simple Planning for 2026

You cannot control tax policy, but you can control how organised you are. A few simple habits make GST on crypto in India much easier to live with.

- Treat GST as one more column in your tax sheetWhen you track your activity, keep GST on fees in the same sheet as your gains, losses and TDS. That stops GST from feeling like a separate universe and makes GST part of the same story as income tax.

- Separate Indian and foreign platforms in your recordsTag which trades were on Indian exchanges and which were on offshore platforms. This helps you and your CA see which fees already had GST charged by the platform and where questions might arise for imported services.

- Save invoices and statements on a fixed scheduleDownload fee invoices and trade history from each exchange at least once a quarter. Many platforms already show the GST part of their fee. If you ever need to explain GST on crypto service fees in India or demonstrate how much tax was already collected through platforms, you have the documents ready.

- Watch your own turnover if you trade as a businessIf your activity starts to look less like investing and more like running a desk – repeated sales, clients, or a fixed spread, keep an eye on your rupee turnover. If you cross the registration limit, your own token sales may trigger GST, not just platform services.

For example: A person who casually buys and sells a few lakhs of crypto a year for themselves does not hit turnover thresholds. A person who runs an OTC group and moves ₹60–70 lakh of tokens a year, collecting spreads as income, is much closer to being seen as a business for GST. - Use one clear system to track all trades and feesIf you only have a few trades, a simple spreadsheet is enough. Once you are active on multiple exchanges, a proper tool saves time and mistakes. A portfolio and tax tool like cryptact can pull trades from different exchanges, keep them in rupees, and generate reports that match what you need for Schedule VDA. The same export gives your CA a clean view of trades, fees and platforms when thinking about GST for crypto trading, reverse charge questions, or whether your activity looks like a business.

- Plan for 2026 as “more clarity, more data”As 2026 starts, you can expect more clarification around edge cases, not a complete rewrite of the system. The 30% tax on VDAs, 1% TDS, and 18% GST on platform services are already in place. The safest move is to assume they will continue, keep your records clean, and be ready for more questions, not fewer.

Final Thoughts

By 2026, GST is likely to stay part of how India deals with virtual digital assets, even if the finer points keep changing. The broad message from policy so far is simple: treat crypto activity as part of the formal economy, not as something separate from regular tax rules.

For anyone who trades or builds products in this space, the sensible response is to make tax impact part of the basic checklist, along with liquidity, spreads and platform risk. If you know how much GST is built into your fees and which of your activities might look like a business supply, it becomes easier to decide which trades or services are actually worth doing.

A tool like cryptact helps here because it keeps all your trades and fees in one place instead of leaving them scattered across exchanges. When your history is already organised, adjusting to new GST clarifications or reporting formats becomes a matter of updating your approach, not rebuilding everything from scratch.

Disclaimer

GST treatment for cryptocurrency remains an evolving area under Indian tax law with limited official clarifications, circulars, or rulings from the Government or GST Council. Businesses and individuals should consult qualified GST professionals for case-specific advice, as interpretations may change with future notifications. This blog provides general information only and does not constitute legal or tax advice.