Fact-checked and reviewed by MetaCounts.co, a Vancouver-based cryptocurrency accounting firm staffed by Chartered Professional Accountants (CPAs)

If you have earned money from cryptocurrency in Canada, it is important to understand how those earnings are taxed. The Canada Revenue Agency (CRA) treats cryptocurrency as a commodity under the Income Tax Act. This means that any income you earn from disposing of crypto, whether through selling, trading, or using it for goods or services, is taxable.

For most individuals, these profits are classified as crypto capital gains. In this case in Canada, only half of the profit is taxable at your regular income tax rate. For example, if you bought Bitcoin for 1,000 dollars and sold it for 1,500 dollars, your gain is 500 dollars, and 250 dollars would be added to your taxable income.

If your crypto activity is frequent or structured like a business, such as regular trading, mining, or staking, the CRA may consider it business income. In that situation, the entire amount is taxable as income instead of capital gains.

Understanding whether your crypto activity results in capital gains or business income is the first step toward filing your crypto taxes correctly and avoiding penalties.

Let’s dive deep into this below.

Table of contents |

No credit card required

Capital Gains vs. Business Income

So, do you pay capital gains on crypto in Canada? The answer is yes, crypto profits are taxable. The CRA looks at what you do with crypto to decide how to tax it.

If you only buy and hold cryptocurrency, it is not taxable until you dispose of it. Disposing means selling, trading, or using the crypto for goods or services. Occasional sales are generally treated as capital gains, so only half of the profit is taxable.

However, if you trade frequently, mine or stake crypto, or operate in a way that resembles a business, the CRA may treat your profits as business income. In that case, the full amount is taxable.

In other words, occasional crypto sales are treated as capital gains, but operating as a business means all gains are fully taxable.

Crypto Capital Gains Tax Rate in Canada

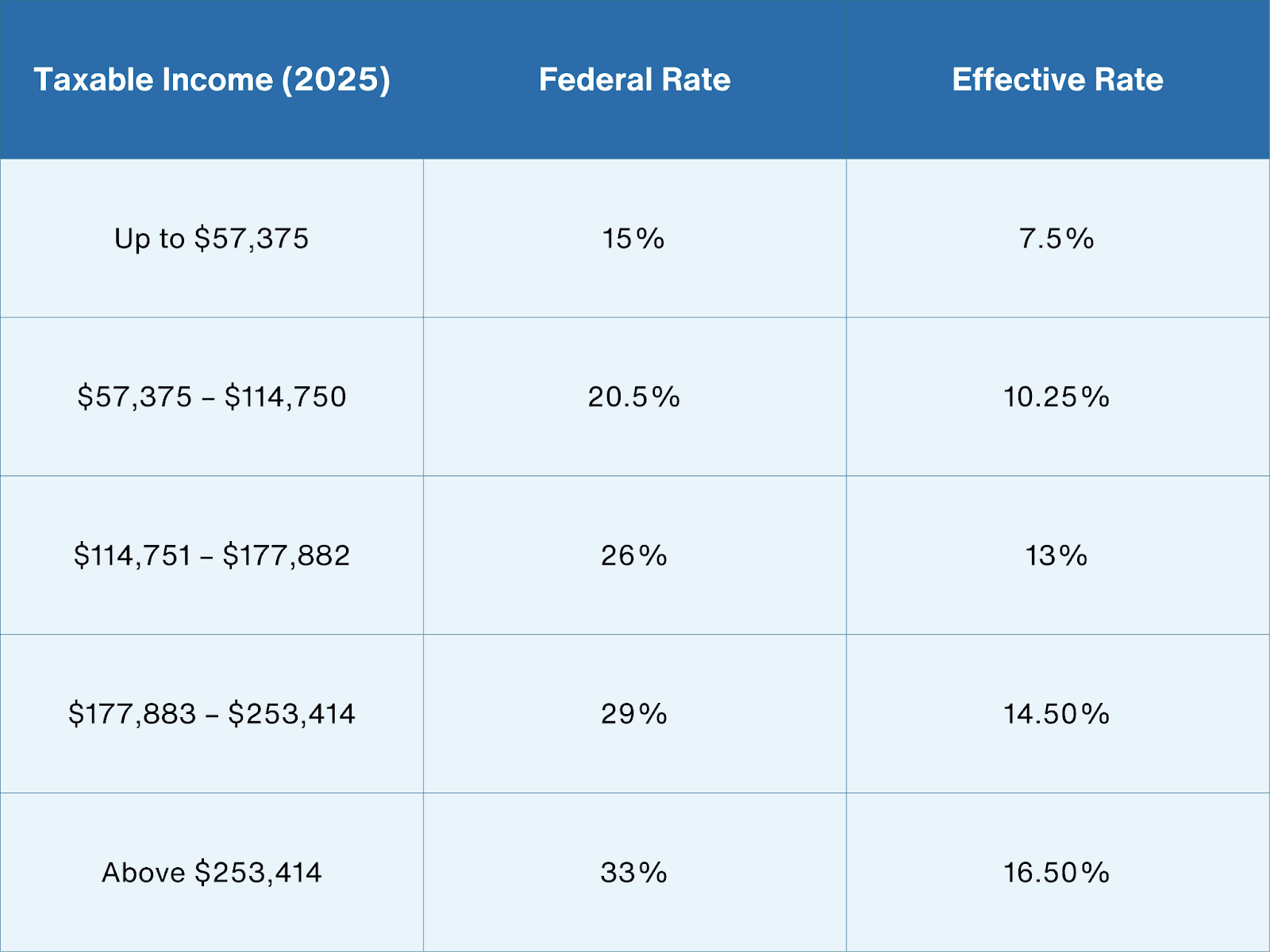

How much is the Canadian capital gains tax on crypto? There’s no special “crypto tax rate”. Crypto gains use the normal tax rates, but only half of the gain counts. The CRA confirms that the crypto capital gains are taxed at the same rates as other investments, with a 50% inclusion rate.

In 2025 the federal brackets are 15%, 20.5%, 26%, 29% and 33% based on your income. Because only half of your gain is taxable, the effective tax rate on a capital gain is half your income tax bracket. For example, in the lowest bracket (15%), you effectively pay 7.5% on your gain. The table below shows federal rates and the effective rate of crypto capital gains tax in Canada:

(Federal crypto capital gains Canada rates for 2025, from CRA guidance. Provincial tax rates add on top of federal rates. Combined marginal rates typically range from 20% to 54% depending on province and income level.)

How to Calculate Crypto Capital Gains in Canada

Now, you must be wondering how to calculate crypto capital gains. To figure your tax, start with your gains or losses. Calculate your cost base: what you paid in CAD for the crypto, plus any fees. Then subtract that from your sale price in CAD. In Canada, you need to calculate your cost base by Adjusted Cost Basis (ACB), which averages the cost of identical properties. With cryptact , the calculation by ACB is automated.

The result is your capital gains (if positive) or losses (if negative). Only realized gains count—meaning you sold, traded, or spent the crypto.

For example, suppose you live in Vancouver and earn $60,000. You made a $15,000 profit from selling crypto. Only half ($7,500) is taxable. If your combined federal and provincial rate is 28.2%, you owe about 28.2% of $7,500 = $2,115 in tax.

In short, the math is: Taxable gain = (Sale price – Cost base) × 50%. If the crypto loses value, you have a capital loss, and you can deduct half of that loss against gains later (see below).

Always record the date, amount and fair value in CAD for each crypto transaction so you can calculate this properly.

How to Report Crypto Capital Gains in Canada

When you report crypto on your regular tax return, the CRA requires you to use Schedule 3 (Capital Gains) of the T1 form. On Schedule 3, use the line for “crypto-assets” or “other property” to enter your gains and losses.

If you earned crypto as a business, use the income forms (for example, T1-Professional income or T2125) instead. If you are preparing for the 2025 income year, which will be filed in 2026, check the Canada Revenue Agency website for the latest information on tax brackets and capital gains rules before you submit your return.

The CRA requires you to report all crypto capital gains, losses, and income by that deadline. Don’t wait until the last minute, and gather your records and file on time.

For accuracy and ease, many investors use tools like cryptact to track all crypto transactions, calculate gains in CAD, and generate reports ready for CRA filing.

Offsetting Losses

Are you wondering “Can I offset crypto losses against gains in Canada?” Yes, losses can cut your tax! The CRA calls them “allowable capital losses.” If you sold crypto for less than you paid, you have a capital loss. You can deduct half of that loss against other capital gains.

For example, a $1,000 loss allows a $500 deduction against gains. You cannot deduct crypto losses from your wage income, it’s only against crypto capital gains. If your allowable losses exceed your gains in a year, you carry the net loss back three years or forward indefinitely to offset future gains.

In other words, keeping track of losses can lower your taxes in future years.

Common Crypto Tax Mistakes

- Not reporting all crypto activity. You must report any sale, trade or use of crypto. Even crypto-to-crypto trades and spending crypto on goods count as dispositions. Many assume “I didn’t cash out, so it’s not taxable,” but the CRA says any profit on a disposal is taxed.

- Ignoring crypto income. For example, staking and mining rewards are taxed at fair market value on the date received. This amount becomes your adjusted cost base when you later sell.

- Lack of records. Not keeping dates, CAD values, and wallet details for each transaction leads to errors. The CRA specifically tells you to track every crypto transaction (number of coins, date/time, CAD value, fees, etc.). Without good records, you can’t calculate crypto capital gains properly.

- Misclassifying activity. If you trade crypto often or run a crypto “business,” CRA may treat your gains as business income. In that case you pay tax on 100% of profit instead of 50%. Be clear about your intent and keep records of frequency.

- Not using losses. Forgetting to claim allowable capital losses is a missed opportunity. You can deduct half your crypto losses against gains. Always report losses so you can use them to reduce taxes.

- Missing forms or deadlines. Use Schedule 3 for crypto capital gains and file by April 30. Late or missing forms can lead to penalties in Canada.

Staying organized helps you avoid these errors. For any confusion, CRA’s guides and reputable tax software like cryptact can help.

Example: Suppose you bought Ethereum for $500 and later sold it for $1,000. Your gain is $500. You only pay tax on half, i.e. $250. If your tax rate is 20%, you owe $50 in tax on that sale (20% of $250). It may seem small, but adding up many trades can be a big bill.

Conclusion

Dealing with crypto taxes in Canada can feel daunting, but understanding the rules for capital gains and business income is key to staying compliant. Keep detailed records of every transaction, including dates, CAD values, and fees, to accurately calculate gains and losses.

Crypto tax tools like cryptact make this process much easier by automatically tracking trades, calculating taxable amounts, and generating reports ready for CRA filing. Staying organized and proactive ensures you pay the correct tax and gives you peace of mind during tax season.