Fact-checked and reviewed by MetaCounts.co, a Vancouver-based cryptocurrency accounting firm staffed by Chartered Professional Accountants (CPAs)

If you're new to crypto or have been holding coins for years, it can be complicated to determine which activities will get you a tax bill and which won't. In Canada, cryptocurrency is taxed like property or a commodity, which is similar to how stocks are taxed.

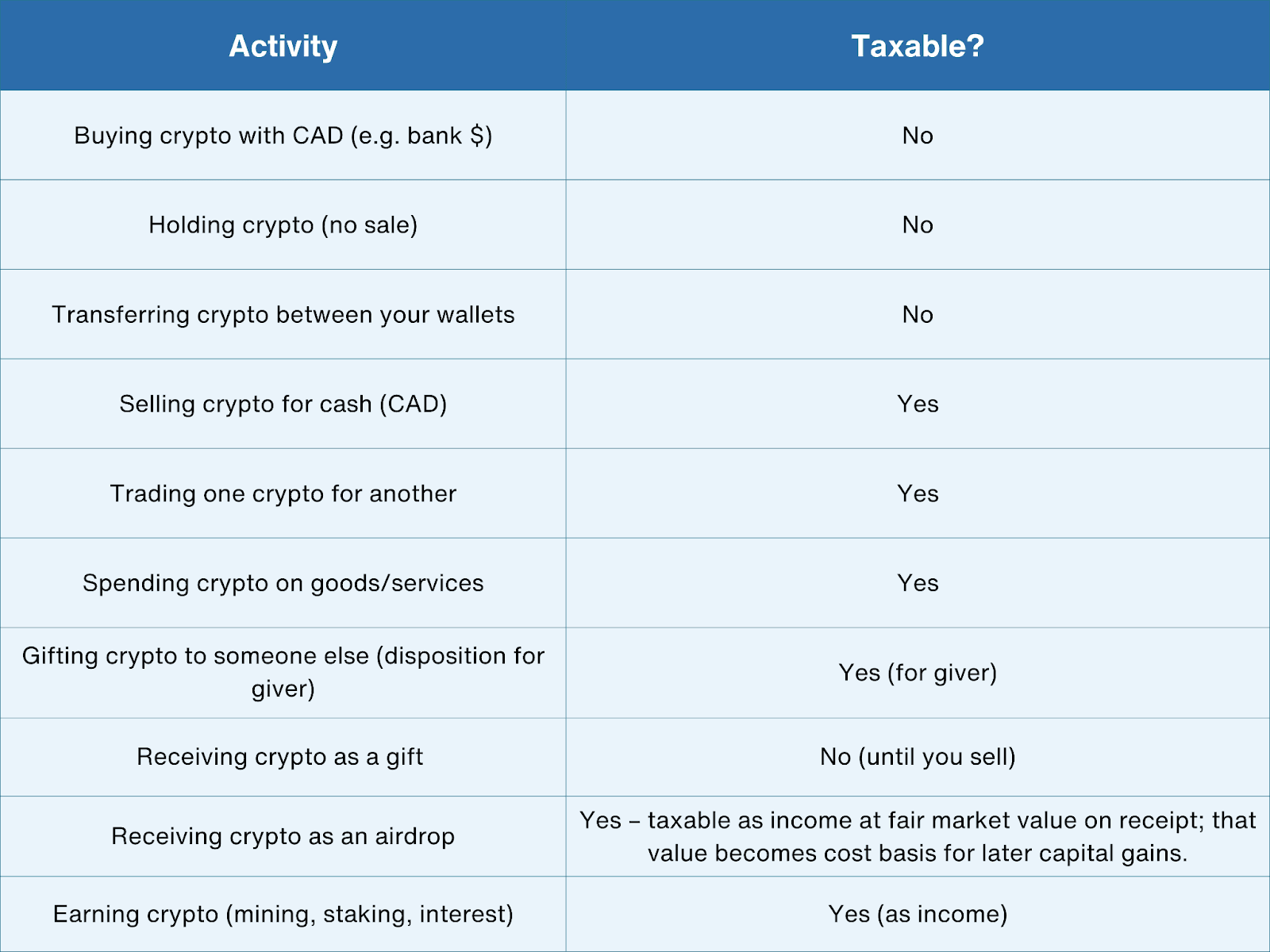

That means you usually only have to pay taxes when you dispose of your crypto. For instance, you could sell it, trade it for another coin, or use it to buy something. The CRA calls these events dispositions.

By contrast, moves that aren’t dispositions are usually not taxable. For example, just buying crypto with Canadian dollars or holding it doesn't automatically mean you have to pay taxes. If you don't sell, you don't have to pay taxes, that's all there is to it. If you know these rules, you won't be caught off guard and you'll make sure you report correctly. Let's keep reading!

No credit card required

Quick Summary

Buying and Holding Crypto (Non-Taxable Event)

When you buy crypto with Canadian dollars (CAD), you’re simply converting one asset (cash) into another (crypto). The CRA does not count that as a disposition. In other words, purchasing crypto by itself is not taxed.

Likewise, if you just hold your coins and don’t sell them, no tax is due. The CRA makes it clear that holding crypto without disposing of it is “tax-free”. Just remember to keep good records of your purchases. The cost in CAD becomes your adjusted cost base for future tax calculations.

Let’s say you buy 0.5 Bitcoin for $10,000 CAD in 2025 and then just let it sit in your wallet. You don’t sell it, trade it, or use it for anything during the year. In this case, there’s no tax to worry about. Since you didn’t dispose of the crypto, nothing is taxable. That $10,000 simply becomes your cost base for whenever you decide to sell in the future.

Transferring Crypto Between Your Own Wallets (Non-Taxable Event)

Moving crypto around between accounts or wallets you own. For example, sending coins from one exchange to another, or from an exchange to your personal hardware wallet, is not considered a sale or disposition.

The CRA explicitly says that transfers between wallets you own “do not result in a taxable disposition”. In plain terms, you still own the same crypto; you’ve just changed its location. This move is not taxed. Of course, if you pay any network fee in crypto when moving it, that small “fee” technically is a disposal of that tiny amount, but in practice it’s usually trivial.

Imagine you move 1 Ethereum from an exchange to your personal hardware wallet because you want better security. Both wallets are yours. You haven’t sold anything or traded it for something else. You’ve just changed where the crypto is stored. Because of that, there’s no tax to report. It’s still the same Ethereum, and you still own it.

Selling or Trading Crypto (Taxable Events)

When you sell crypto for Canadian dollars (or another fiat currency), or swap one cryptocurrency for another, that is a disposition. This triggers a taxable event. In CRA terms, you realise a capital gain (or loss) if the proceeds exceed your cost base.

Trading one coin for another (say Bitcoin for Ethereum) is treated the same way. CRA sees it as if you sold the first coin at its fair market value and then used the proceeds to buy the second. For most personal investors, these profits are reported as capital gains, which means only 50% of the gain is included in taxable income.

In some cases, though, CRA can treat your crypto activity as a business rather than investing. That depends on factors such as:

- How frequently you trade (for example, you are in and out of positions many times a month)

- How much time you devote to trading and tracking markets

- Your level of sophistication, use of strategies, tools or bots

- Whether your main intention is short term profit rather than long term holding

If your pattern looks more like running a trading operation than investing, profits can be taxed as business income, which means the full amount is taxable (not just 50% of the gain).

Example

Suppose you bought 2 Ethereum a few years ago for $3,000 CAD. In 2025, you decide it’s a good time to sell and you get $8,000 CAD. You have a $5,000 profit.

- If this is on capital account, only half of that gain, $2,500, is added to your taxable income.

- If CRA views your trading pattern as a business, the full $5,000 could be treated as business income.

If instead of selling for cash you traded that Ethereum for Bitcoin worth $8,000 CAD, the tax result would be the same. From CRA’s perspective, you still disposed of the Ethereum and realised a gain or loss at that point.

Spending Crypto on Goods or Services (Taxable Event)

Using crypto to buy things like goods, services, or even rent is also a disposition. For tax purposes, paying with crypto is like trading because it is not money that the government issues. In practice, it means you have effectively “sold” your crypto for the value of what you purchased, and you have to compute any gain or loss as if you sold the coin at that moment.

Example

Let’s say you use Bitcoin worth $500 CAD to buy a new laptop. You originally paid $300 CAD for that Bitcoin. For tax purposes, this is the same as getting $500 CAD for the Bitcoin and then paying the store.

- Proceeds of disposition: $500

- Cost base: $300

- Capital gain: $200

You report a $200 profit, even though you never received cash in your bank account.

The same logic applies to gas or network fees:

- Any crypto you use to pay gas is also being disposed of.

- The value of the crypto used as a fee at that moment is a small taxable event (usually a small capital gain or loss).

Most people ignore gas fees because the amounts are small, but technically every bit of crypto you spend whether on a laptop, a service, or gas counts as a disposal for tax purposes.

Gifting Crypto (Taxable for Giver, Not for Recipient)

The CRA sees giving away crypto as the same thing as selling it for its fair market value. If you give crypto to a friend, you'll have to pay taxes on any money you make from it. You can figure out how much that is by looking at the base of the receiver. But the person who gets the crypto doesn't have to pay taxes.They will only have to pay taxes when they sell it themselves.

Think about giving a friend $10,000 CAD worth of crypto. You paid $6,000 for it at first. The CRA acts like you sold the crypto, even though it was a gift and not a sale. That means you made $4,000 in capital gains, and you have to pay taxes on $2,000 of that.

Your friend, on the other hand, doesn't have to pay taxes on the gift when they get it. They don't have to worry about taxes until they sell or trade the crypto.

Free Crypto: Airdrops and Forks (Taxable on Receipt)

You might get free crypto from an airdrop or a hard fork. For airdrops, the safer approach is to treat the value you receive as income at fair market value when the tokens hit your wallet. That amount is added to your income for the year, and it becomes your cost base for capital gains when you later sell or spend those tokens. Some people treat unsolicited airdrops as having a zero cost base and only tax them on sale, but here we follow the more conservative “taxable on receipt” view.

Forked coins are different. When a chain splits and you receive new coins because you held the old chain, many investors and advisors treat the new coins as capital property with a low or zero cost base, and tax only arises when you later dispose of them.

Example

One day you open your wallet and see 200 new tokens from an airdrop. At that time, each token is worth $3. You report $600 as income, and $600 becomes your total cost base. Later, you sell all 200 tokens for $4 each and receive $800 CAD. Your capital gain is $200 ($800 proceeds minus $600 cost base). If this is on capital account, half of that $200 is taxable.

Mining, Staking, and Other Crypto Income (Taxable)

In contrast to the above, earning crypto as income is usually taxable. If you mine coins or earn staking rewards, the CRA normally sees that as business income (especially if it’s on a commercial scale). You would include the fair market value of coins at the time you received them as income in that year.

Similarly, any crypto you receive as payment for goods or services you provide is included in income (just like being paid in CAD). When you sell those coins, that's when capital gain rules kick in. In most cases, getting paid in crypto or mining crypto is not tax-free. You report it as income when you get it, and then you treat future sales as capital gains.

The CRA looks at crypto that you earn through mining or staking in a different way. For instance, let's say you get $2,000 CAD in staking rewards over the course of the year. You need to report that $2,000 as income. If you later sell those same coins for $2,500, the extra $500 is treated as a capital gain and taxed separately. So first it’s income when you earn it, then capital gains when you sell it.

Wrap-up and Action Steps

In summary, the CRA only taxes crypto when you dispose of it. Buying crypto with cash, keeping it, or just moving coins between your own wallets isn’t a taxable event. Anything else, like selling, trading, spending, gifting (for the giver), or earning crypto, will generally create a taxable event under CRA rules.

To follow these rules, you need to keep detailed records of every transaction, including what you bought or sold, when you did it, the CAD values, and the transfers.

Stay organized and know when taxes apply so you can enjoy crypto without worry. It's important to remember that having the right software and keeping accurate records can help you avoid problems during tax season. Take a few minutes right now to write down what you've bought, sold, and moved. You might want to think about using a crypto tax tool like cryptact to help you with your taxes.That way you’ll be ready when the deadline rolls around…and you’ll only pay the taxes you truly owe!