Fact-checked and reviewed by MetaCounts.co, a Vancouver-based cryptocurrency accounting firm staffed by Chartered Professional Accountants (CPAs).

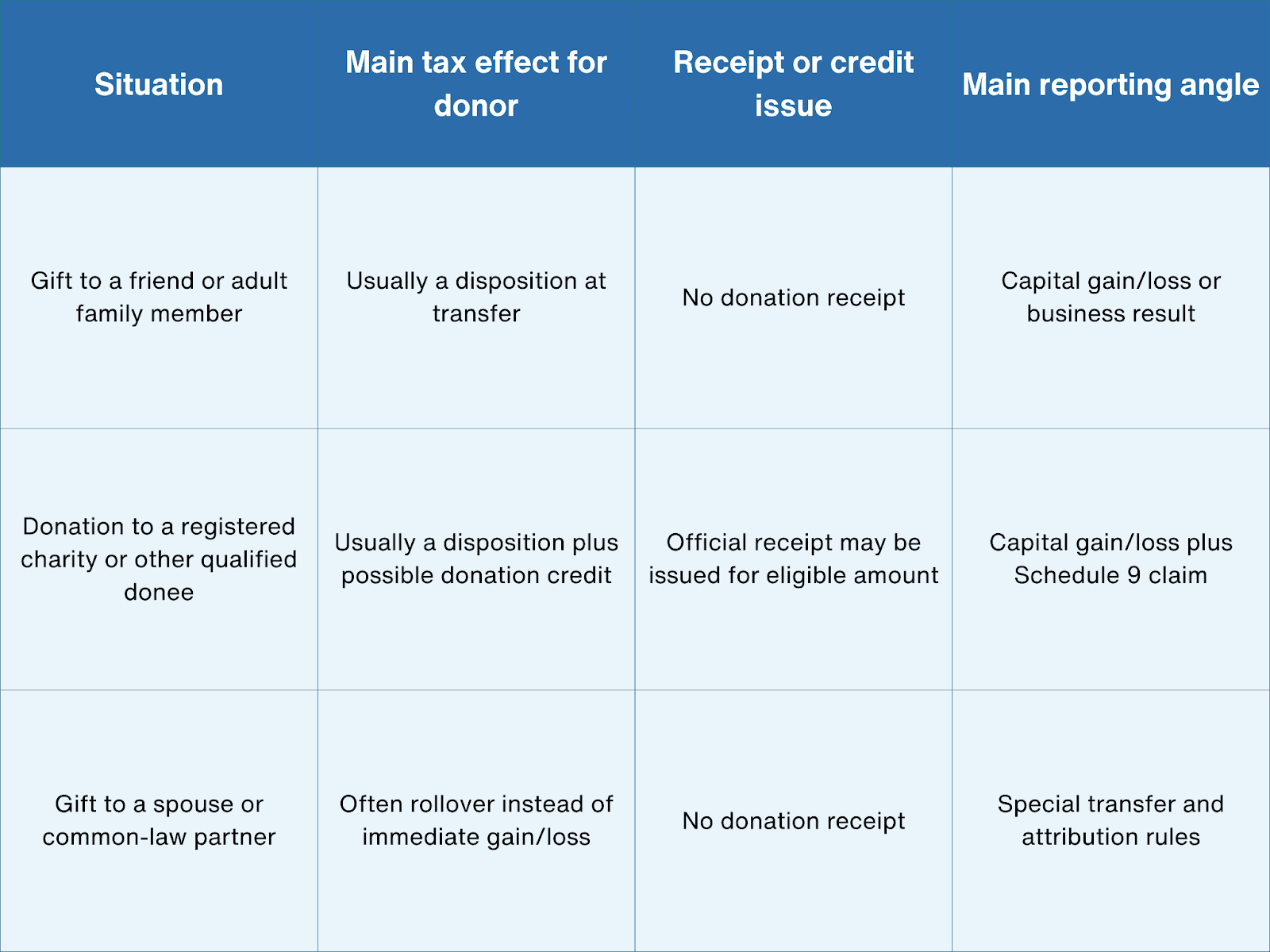

Giving crypto away sounds simple. In practice, it can create very different tax results depending on who receives it. A transfer to a friend or family member is not the same as a donation to a registered charity. A gift to a spouse can follow a different rule again. The tax treatment changes because CRA looks at the legal nature of the transfer, not just the fact that you no longer hold the coin.

That is why questions about crypto gift tax in Canada and crypto donations tax in Canada often get mixed together. In CRA's framework, both gifts and donations can be dispositions of crypto, though a donation to a qualified donee may also create a donation tax credit if the receipting rules are met. The real work is in distinguishing the scenario, valuing the crypto properly, and reporting the right numbers in the right place.

Key takeaways

- CRA says a disposition of a crypto-asset may occur when you transfer ownership by way of gift or donation.

- A gift to a registered charity or other qualified donee can also create a donation tax credit if an official receipt is issued for the eligible amount.

- For gifts of capital property to a qualified donee, you are generally considered to have disposed of the property at fair market value.

- Crypto is not on CRA's list of property eligible for the zero inclusion rate that applies to certain donated securities and ecological gifts.

- Donation claims generally flow through Schedule 9 and then line 34900, and they can usually be claimed up to 75% of net income, with limited exceptions allowing up to 100% in specific cases, along with carryforwards of up to 5 years.

- If you give capital property to your spouse or common-law partner, a rollover rule often applies instead of an immediate capital gain or loss, though later attribution rules may matter.

No credit card required

Gifts and donations are not the same thing

The first distinction is the most important one. If you give crypto to another individual, CRA generally treats the transfer as a disposition if ownership changed. If you donate crypto to a qualified donee such as a registered charity, CRA still treats the transfer as a gift of property, though the charitable donation rules can now come into play as well. That second category is where official receipts, eligible amount, Schedule 9, and donation credits become relevant.

A useful way to frame the issue is this:

That is the real backbone of a CRA reporting guide here. The transfer may look similar on-chain, though the tax outcome can be very different.

How CRA usually treats a crypto gift to another person

CRA's crypto guidance says a disposition may occur when you transfer ownership of a crypto-asset by way of gift or donation. If your crypto is on capital account, that means you usually need to compare the transfer value with your adjusted cost base to work out whether you have a capital gain or capital loss. If the activity is on business account, the full profit or loss is reported as business income or loss instead.

This is the part many people miss. Giving away crypto does not mean CRA ignores the accrued gain. If you bought BTC for C$8,000 and later gifted it when it was worth C$13,000, you have not sold it for cash, though you may still have a disposition for tax purposes. The fact that the recipient is a friend or relative does not automatically erase the donor-side tax result.

A simple way to think about a personal crypto gift is:

- determine the coin and quantity transferred

- determine the fair market value at the transfer date

- compare that value with your ACB

- report the resulting gain or loss if the asset was capital property

If you are gifting crypto instead of donating it to a qualified donee, there is no charitable receipt to soften the result. That is why plain family gifting and charitable donations should never be lumped together in the same paragraph or spreadsheet line.

How crypto donations to charities work

A donation to a charity follows a different path because the donee may issue an official donation receipt, but only if it is a qualified donee under CRA rules. CRA's qualified donee guidance includes registered charities and certain other listed organizations that can issue official receipts. If the recipient is not a qualified donee, you do not get the donation-credit side of the story even if the transfer felt charitable in substance.

For non-cash gifts, CRA treats the transfer as a gift in kind. P113 says that if you donate capital property, you are generally considered to have disposed of it for proceeds equal to the fair market value of the property, and you must report any resulting capital gain in the year of donation. At the same time, the charity can generally issue an official receipt based on the eligible amount of the gift, subject to the receipting rules.

That is what makes crypto donations tax reporting in Canada different from an ordinary gift to a person. You may have:

- a donor-side capital gain or loss

- an official receipt from the qualified donee

- a donation tax credit claim based on the eligible amount

A short example makes the split clearer. Suppose you donate ETH to a registered charity. Your ACB is C$2,500 and the ETH is worth C$4,000 when transferred. On a basic reading, you may have a capital gain based on that increase in value, and you may also receive a receipt if the charity issues one properly. Those are two separate tax consequences from the same transfer.

Valuation and receipting issues that trip people up

Valuation matters because a donation receipt is based on fair market value at the time of the gift, not what the donor assumes. CRA's receipting rules for non-cash gifts focus on this value when determining the eligible amount.

There is also a technical trap here. P113 also includes special rules where the fair market value of gifted property may be limited to cost in certain situations, such as property acquired through gifting arrangements or specific types of transfers. These rules do not apply to all crypto purchases, so they should not be assumed in ordinary donation cases.

Another detail that matters is that crypto does not appear on CRA's list of gifted property eligible for the zero capital-gains inclusion rule. That list covers certain publicly listed securities, mutual fund units, prescribed debt obligations, and certain ecological gifts. For ordinary crypto donations, you should not assume the same special treatment that applies to donated public shares.

How to report crypto gifts and donations to CRA

If the transfer created a capital gain or loss, that side of the transaction follows the usual capital-gains route. CRA's crypto guidance and capital-gains pages point taxpayers to Schedule 3 for capital dispositions and line 12700 for the resulting taxable capital gain. If the crypto activity is business income instead, the full profit or loss is reported under the ordinary business-income route.

If the transfer was a donation to a qualified donee and you received a valid official receipt, the donation-credit side generally runs through Schedule 9 and then line 34900. CRA says you can generally claim all or part of the eligible amount of your gifts up to 75% of net income, and you can usually carry forward unclaimed amounts for up to 5 years. CRA also says gifts of capital property can increase the donation limit in some cases, up to 100% of net income.

For practical reporting, your file should include:

- the wallet and TXID showing the transfer

- the fair market value in CAD on the transfer date

- your ACB in the donated or gifted crypto

- any official donation receipt

- proof that the recipient was a qualified donee if you are claiming the credit

- records showing whether any advantage was received

That last point matters because the eligible amount of the gift is reduced by the value of any advantage, and in some cases no receipt can be issued if the advantage is too large.

Where the spouse exception changes the result

A gift to a spouse or common-law partner is one of the biggest exceptions to the ordinary "gift equals disposition" framework. CRA's transfers-of-capital-property page says you generally do not have a capital gain or loss if you give capital property to your spouse or common-law partner, because a rollover rule usually applies. That means the donor does not typically crystallize an immediate capital gain or loss at the time of transfer.

That said, the tax issue does not disappear entirely. CRA also says that if the spouse later sells the property during your lifetime, attribution rules can make the original transferor report the capital gain or loss in many cases. So the spouse gift is softer at the transfer date, but it can still create complexity later. This is one of the clearest examples of why a "crypto gift" article cannot stop at the blockchain transfer itself.

How cryptact helps

Crypto gifts and donations create a record problem before they create a filing problem. You need to know what left the wallet, what it was worth in CAD at that moment, what the donor's ACB was, and whether the transfer was a personal gift, a spouse rollover, or a donation to a qualified donee.

That is where cryptact helps in a practical way. It brings exchange and wallet data into one place, helps preserve transaction history around the transfer date, and makes it easier to support capital-gain calculations with cleaner records. For users handling gifting, charitable transfers, or mixed wallet activity, that structure can make the difference between a clean donation file and a year-end scramble.

Conclusion

A strong crypto gift tax Canada analysis starts by asking one question: who received the crypto. If the answer is a friend or family member, you are usually looking at a gift-side disposition analysis. If the answer is a registered charity or other qualified donee, you may also have a donation credit claim. If the answer is a spouse, rollover and attribution rules may change the timing completely.

That is why crypto donation tax reporting in Canada is really about classification first, valuation second, and forms third. Once you know which bucket the transfer falls into, the rest becomes much easier to map: fair market value, ACB, receipt eligibility, Schedule 3, Schedule 9, and line 34900 where relevant. cryptact helps make that process workable by keeping the transfer history and value trail clear enough to support the result.