Fact-checked and reviewed by MetaCounts.co, a Vancouver-based cryptocurrency accounting firm staffed by Chartered Professional Accountants (CPAs)

Crypto is normal in Canadian portfolios now. For CRA, though, it is not a special new asset. Crypto is treated as property (a commodity) and falls under regular income tax rules. Earnings are either capital gains or business income, depending on how you use it.

Most people who land on CRA tax on crypto want to understand three things:

- Which crypto transactions are taxable

- Whether their profits are capital gains or business income

- Which forms and records CRA expects for 2026

This guide answers those questions and ends with a step-by-step CRA crypto tax checklist and where cryptact fits into an organized setup.

Table of contents |

No credit card required

How CRA treats cryptocurrency in 2026

Start with CRA’s basic position. If you understand that clearly, the rest is just applying it.

CRA guidance says cryptocurrencies, tokens and NFTs are commodities for income taxes. They are not legal currency. Any gain or loss from trading or using them is taxed in the same way as other property.

Key points:

- Holding crypto by itself is not taxable

- Disposals and crypto income are what matter

- Crypto falls under the same capital gain and business income rules as shares or other assets

So when you think about crypto tax CRA questions, always ask: did I dispose of an asset, or did I earn income from it this year.

Which crypto transactions are taxable

Not every wallet movement is a tax event. CRA’s crypto pages and capital gains guide list the events that count as a disposition and must go in your return.

Two big buckets:

1. Taxable disposals

These usually feed into capital gains (or business income if you trade as a business):

- Selling crypto for Canadian dollars

- Swapping one coin or token for another

- Spending crypto on goods or services

- Selling NFTs or game tokens for value

Guide T4037 makes it clear that swapping one crypto asset for another is a disposition. You must convert the value you receive into CAD and compare it with your adjusted cost base for that asset.

This answers CRA taxes on crypto in one line. Yes. If you sell, swap or spend, that gain or loss belongs on your return.

2. Crypto income

Some crypto shows up as income rather than a trade:

- Payment for freelance work or salary in crypto

- Staking rewards credited to your wallet

- Liquidity pool or yield farming rewards

- Referral bonuses or platform rewards

CRA and Canadian tax firms treat these as income when you receive them, valued in CAD at that time. Whether that income is business or property income depends on scale and intent.

3. Non-taxable movements

These do not trigger tax but still need records:

- Buying crypto with CAD and holding it

- Moving coins between your wallets

- Moving tokens into or out of your cold storage

Tax advisors repeat the same rule: no tax for just holding, tax when you use, exchange, convert or gift crypto assets.

So “do you get taxed for buying crypto CRA” has a simple answer. The buy is not taxed. The later sale or swap is.

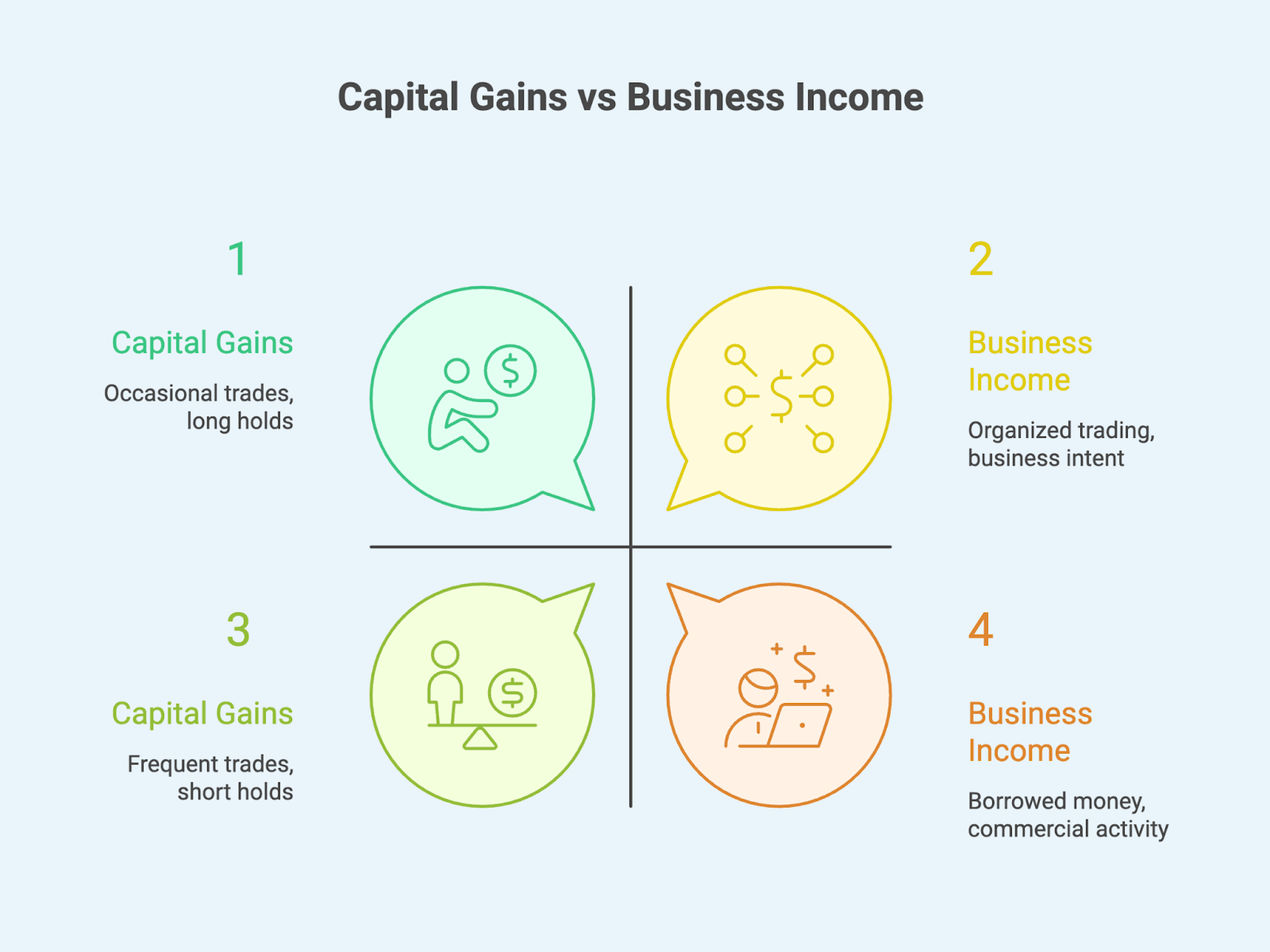

Capital gains vs business income

For most retail users asking about CRA tax crypto rules, crypto gains will be capital gains. For others, especially high-volume traders, CRA may see gains as business income.

CRA’s own tips and outside guidance describe the usual factors:

- Frequency of trades

- Length of holding periods

- Use of borrowed money

- How organised and commercial your activity is

- Whether you promote yourself as a trader or run a crypto business

If your activity looks like investment (occasional trades, long holds, no business setup), CRA usually taxes gains under capital rules. You include 50 % of net capital gains in income. If your activity looks like a commercial operation, CRA treats the full profit as business income.

Table at a glance:

| Pattern | CRA view | Inclusion rate |

| Occasional trades, long-term focus | Capital gains side | 50% of net gain |

| High volume, organised trading, business intent | Business income side | 100% of profit |

If you sit on the line between the two, talk to a tax professional, not just a crypto tax calculator CRA style tool.

Records CRA expects you to keep

By 2026 CRA expects detailed crypto records, not only yearly totals. The crypto asset guidance says you must keep records of every transaction and keep them even if a platform closes.

Minimum data per transaction:

- Date and time

- Type (buy, sell, swap, income, transfer)

- Asset and quantity

- Value in CAD at that time

- Fees in CAD

- Wallet addresses and platform names

You also have to keep records for foreign exchanges and platforms. T1135 rules can apply if your foreign crypto and other specified property cost more than CAD 100,000 at any time in the year.

Law firms and advisors are already warning that CRA uses blockchain analytics and other digital tools to match reported income with real activity. Clean records are your safety net.

CRA crypto tax checklist for 2026

This is the practical part. You can walk through it at tax time or use it as a mid-year health check for CRA crypto taxes.

1. Map your platforms and wallets

- List every exchange, wallet, DeFi app and NFT market you used

- Mark which are Canadian and which are foreign

2. Export complete histories

- Download CSV exports from each platform for the full year

- Include NFT sales and DeFi events that led to income or disposals

- Make sure you can get price data in CAD for each date

3. Classify each transaction

- Tag buys, sells, swaps, income and transfers

- Separate taxable disposals from non-taxable internal moves

- Decide if you are on capital account or business account overall

4. Calculate gains, losses and income

- Use adjusted cost base for each asset, as set out in Guide T4037

- For each disposal, compute proceeds in CAD minus ACB and fees

- Sum total capital gains and capital losses

- Add income from staking, rewards and payments received

5. Check GST / HST if you run a business

- If you accept crypto as payment in a registered business, GST or HST still applies to the underlying sale based on its CAD value

- Some mining situations have separate GST rules and need advice

6. Complete and file the right forms

We cover the forms next, but keep this checkpoint in mind:

- T1 personal return

- Schedule 3 for capital gains from crypto and other property

- T2125 if you have crypto business income

- T1135 if foreign holdings cross CAD 100,000 cost threshold

If you follow this checklist, you have answered most CRA tax on crypto expectations before CRA ever asks.

Forms, deadlines and new reporting rules

The normal personal filing deadline stays around 30 April for most individuals, with later dates if you or your spouse carry on business, but any balance is still due by the usual payment date.

Core forms that handle CRA crypto tax form questions:

- T1 General – main personal return

- Schedule 3 – capital gains and losses, including crypto disposals

- T2125 – business or professional income if CRA treats your crypto activity as business

- T1135 – foreign income verification if your foreign specified property cost exceeds CAD 100,000 at any time

From 2026 onward, you also need to be aware of the crypto asset reporting framework (CARF). Canada has started the process to implement OECD CARF rules. These rules will require Canadian crypto asset service providers to collect and report user details and transaction data to CRA, then CRA will exchange that information with other tax authorities.

Law firms are already flagging that from 2026 and 2027, CRA visibility into crypto accounts and high-value transfers will increase. The days when you could rely on platforms not talking to CRA are ending.

Using cryptact in a CRA compliant workflow

You asked not to reuse old cryptact blog content, so this section stays high-level and non-repetitive.

If you trade on more than one exchange or use DeFi and NFTs, manual spreadsheets become fragile fast. A tool like cryptact helps by acting as the middle layer between all your CSV exports and your tax return.

You can:

- Import data from multiple exchanges and wallets in one place

- See gains, losses and income in CAD across the year

- Separate taxable disposals from transfers

- Pull a report that lines up with what you need for Schedule 3 and your own records

Think of as a tracking and calculation engine. You still decide with your accountant whether your profile is capital or business, and you still file through CRA approved channels, but you are not guessing your numbers.

If you want deeper detail on capital gains or DeFi treatment, you can always link out to earlier cryptact guides from this article. The key is that this 2026 checklist stays focused on CRA’s latest rules, while cryptact handles the heavy lifting of turning your raw transaction history into clean, CRA ready figures.