Did you trade cryptocurrency this year? Sold some Bitcoin for a profit? If yes, you likely owe taxes on those crypto transactions. How to file crypto taxes might sound complicated at first. But you can handle it step by step. This crypto tax filing guide will walk you through filing crypto taxes in simple terms.

Filing crypto taxes means tracking each transaction and calculating gains or income from your cryptocurrency activities. Many tax authorities treat crypto like property, so selling or earning crypto can trigger taxes.

Table of contents |

When Do You Owe Crypto Taxes?

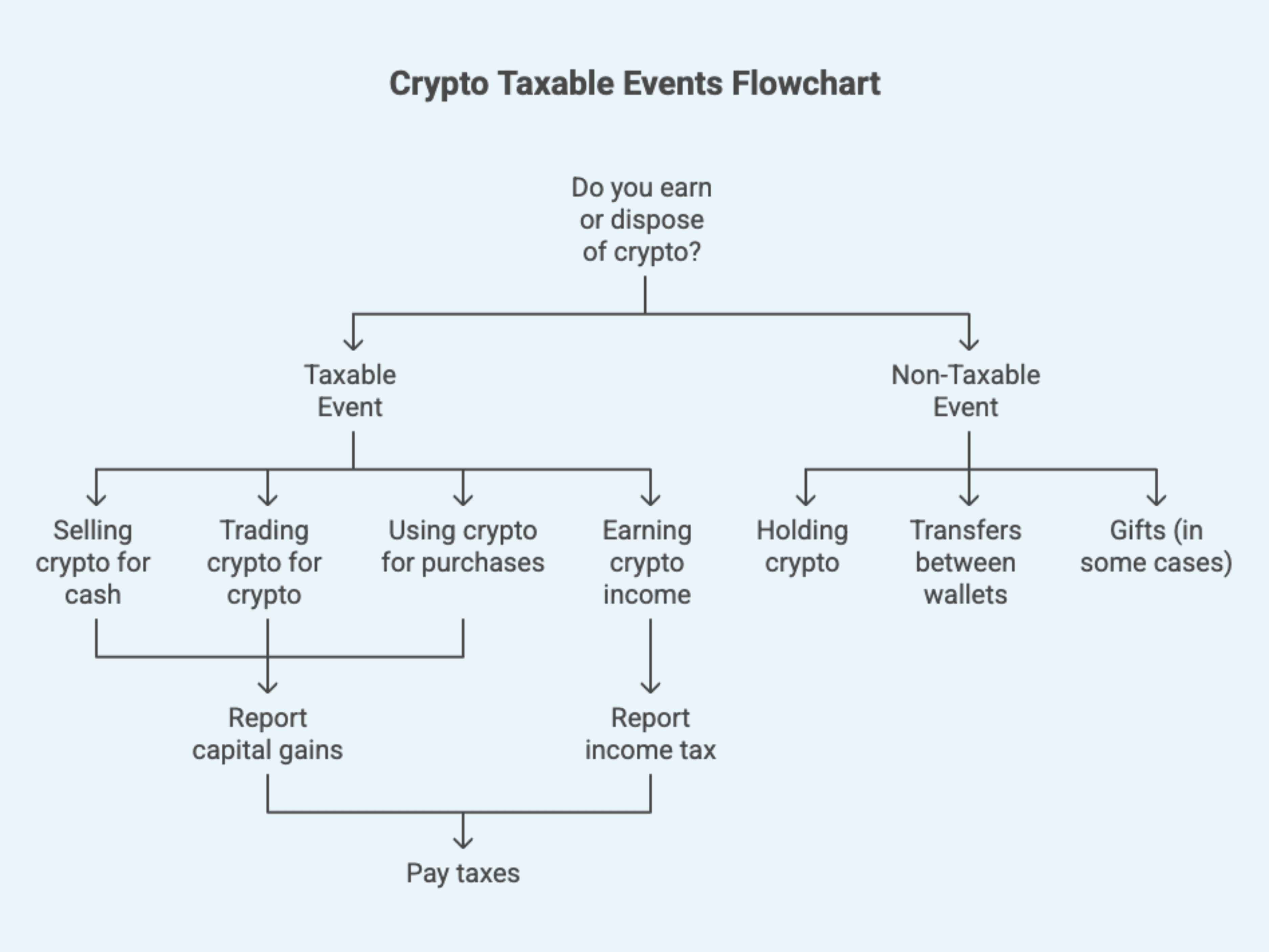

You need to pay taxes on crypto when certain events happen. Any time you earn crypto or dispose of it, it counts as a taxable event. In other words, when you receive new coins as income or when you sell, trade, or spend your crypto, you may owe tax. Here are common taxable events in crypto:

- Selling cryptocurrency for cash: If you sell crypto for your local currency, any profit is a capital gain that you must report.

- Trading one crypto for another: Swapping Bitcoin for Ethereum (for example) is treated like selling one asset and buying another. This triggers a taxable gain or loss.

- Using crypto to buy goods or services: Spending crypto on a purchase (like buying a gift card or a car with Bitcoin) is also a disposal. It creates a gain or loss based on the change in value since you got that crypto.

- Earning crypto income: If you mine cryptocurrency, stake coins, receive airdrops, or get paid in crypto, it’s taxed as income. You owe income tax on the value of the coins at the time you received them.

Not every crypto move is taxed. Some activities are not taxable:

- Holding crypto: Simply buying crypto with fiat and holding it doesn’t trigger taxes by itself. You only pay tax when you sell or use it.

- Transfers between your own wallets: Moving your coins between exchanges or wallets you own is not taxable. There’s no sale or income; it’s just a transfer.

- Gifts (in some cases): Giving crypto as a gift generally isn’t taxable to the giver. The receiver might have to consider tax when they eventually sell it.

Why is crypto taxed?

In many countries, including the U.S., crypto is treated as property or an investment asset for tax purposes. This means governments tax crypto profits similar to stocks.

You pay capital gains tax when you sell at a profit, and you pay income tax if you earned crypto by working or staking. Most countries follow this approach, though details can vary. Always check your local crypto tax rules, but the general ideas are usually the same worldwide.

Step-by-Step Crypto Tax Filing Guide

Here’s a step by step crypto tax filing breakdown. Follow these steps to file crypto taxes accurately and confidently.

Step 1: Gather All Your Crypto Records

Collect a complete record of every crypto transaction you made during the year. This includes every time you bought, sold, traded, spent, or earned crypto. Good record-keeping is the foundation of accurate tax filing. Make a list or spreadsheet of all transactions with dates, amounts, coin type, what you paid (cost), what you got in return, and any fees.

Many exchanges let you download a transaction history. If you used multiple exchanges or wallets, gather data from all of them. Don’t leave anything out, since missing records can lead to mistakes on your taxes.

If you’re learning how to file crypto taxes manually, this part is essential. You’ll need every transaction detail before you move on.

Step 2: Calculate Your Crypto Gains and Losses

Now figure out your capital gains or losses for each taxable crypto event. For every sale, trade, or spending of crypto, determine if you made a profit or a loss. You can calculate this by taking the selling price (or value when spent) minus your cost basis (what you originally paid for that crypto, including fees).

If the result is positive, you have a gain. If negative, you have a loss. For example, if you bought 1 ETH for $2,000 and later sold it for $3,000, your gain is $1,000. If you bought at $2,000 and sold at $1,500, you have a $500 loss.

Add up all your individual gains and losses to get your total for the year. In many countries, losses can offset your gains and reduce your taxable amount. If your losses exceed your gains, you might even be able to deduct some extra loss against other income.

Also note how long you held each crypto before selling. Many tax systems have different rules for short-term versus long-term holdings. Short-term (under one year) gains are taxed at your normal rate. Long-term gains often get a lower rate. Check your local rules before filing.

Step 3: Calculate and Report Crypto Income

Next, account for any crypto you earned as income. This could be from mining, staking rewards, referral bonuses, airdrops, or payments in crypto. For each instance where you received crypto, find out its value at the time you got it. That value is your income amount. You owe income tax on it, just like you would for a paycheck.

If you’re unsure how to report crypto taxes correctly, list every crypto income event with the value on the day received. Keep these records separate from your trading transactions to avoid confusion.

Step 4: Fill Out Your Tax Forms

Now that you have all your totals, it’s time to fill in the actual tax paperwork. The exact forms depend on your country, but the process is similar everywhere.

Report your capital gains and losses using the appropriate form. In the U.S., that’s Form 8949 and Schedule D. You’ll list every taxable crypto sale or trade with its details: date, cost, proceeds, and gain or loss.

Report any crypto income in the relevant section of your return. In some cases, you’ll add it to your employment income or under “other income.” Label it clearly as cryptocurrency income.

Prefer doing it by hand? Then follow how to file crypto taxes without software. Calculate your totals manually, enter them on the forms, and attach your records.

Step 5: File and Pay Your Taxes

Finally, submit your return by the official deadline in your country. Make sure you pay any tax owed on time to avoid penalties. Keep a copy of your tax return and all crypto transaction records for several years.

If you prefer a digital tool, try trusted crypto taxes filing software options like cryptact. They simplify the math and generate compliant reports.

But if you’re confident about how to file crypto taxes manually, you can prepare the report yourself for free. Or use government-provided e-filing portals for how to file crypto taxes for free.

If you follow this crypto tax filing guide, you’ll be able to file accurately whether you’re using a tool or doing it manually.

Tools to Simplify Crypto Tax Filing

Crypto tax tools can save you a lot of time and effort. These are software platforms that automatically aggregate your transactions and calculate your taxes for you. If you are exploring how to file crypto taxes, these tools fit neatly into any crypto tax filing guide.

Instead of doing all calculations by hand, you can connect your exchanges and wallets to these tools and let them generate your tax reports. They help ensure accuracy and can even point out ways to save on taxes. This is useful whether you plan to file crypto taxes using software or you prefer how to file crypto taxes without software.

Here are a few popular crypto tax tools for individuals:

- cryptact: A professional-grade crypto taxes filing software built for accuracy and regulatory compliance. cryptact automatically aggregates exchange and wallet data, tracks portfolio performance, and produces jurisdiction-specific tax reports. It handles complex crypto activities such as DeFi, margin trading, and NFT transactions with precision. Designed for both individuals and professionals, cryptact helps users maintain full transparency and confidence in their filings.

- Koinly: A tool that tracks transactions across exchanges and wallets. Koinly calculates your gains and generates tax reports. It supports multiple countries’ tax systems.

- CoinTracker: A portfolio tracker and tax calculator. It generates tax reports and integrates with exchanges for data pulls. It supports multiple jurisdictions.

- CoinLedger: A crypto tax platform that supports DeFi and NFT activity. It imports transactions and produces tax forms for common use cases.

- CryptoTaxCalculator: Aimed at advanced users with complex activities like DeFi, margin trading, and yield farming.

Most crypto tax tools allow you to connect your accounts by API keys or upload CSV files from exchanges and wallets. They can calculate every gain, loss, and income event and generate a report that you can use to file crypto taxes.

While many tools provide these basic features, cryptact goes further by delivering professional-grade accuracy and country-specific compliance, even for complex transactions like DeFi and margin trading.

If you want to avoid paid plans, you can export summaries and use government portals for how to file crypto taxes for free.

Tips for Filing Crypto Taxes

Filing crypto taxes for the first time? These practical tips pair well with any crypto tax filing guide or step by step crypto tax filing checklist:

- Stay Organized Year-Round: Keep a live log or spreadsheet of all transactions. Portfolio trackers like cryptact’s integrated dashboard help too. Good records make filing crypto taxes faster and more accurate and support anything you submit when you file crypto taxes.

- Use a Consistent Accounting Method: If your country allows ACB, FIFO, LIFO, HIFO, or specific identification, choose one and stick to it. Consistency makes it easier when you decide how to report crypto taxes across years.

- Take Advantage of Losses: Report losing trades to offset gains. Using a reliable tool like cryptact can make this process far easier and more accurate than manual filing. .

- Hold Longer When Feasible: Longer holding periods can qualify for better rates in many places. This strategy fits both software users and those choosing how to file crypto taxes without software.

- Do Not Rely Only on Exchange Reports: If you move coins between platforms, some reports may miss cost basis data. Cross-check before you file crypto taxes, even if a tool is connected.

- Check Your Country’s Specific Rules: Local forms and rates vary. Read local guidance so your filing crypto taxes approach matches your jurisdiction. Tools like cryptact provide country-specific tax reporting to help you stay compliant.

- Consider Professional Advice for Complex Cases: If you used DeFi, NFTs, yield strategies, cryptact’s advanced reporting can handle these complexities with precision. For very large portfolios, a crypto-savvy accountant can still provide an extra layer of review before submission.

- Use Crypto for Charitable Donations (Optional): Donating to qualified charities can reduce taxes in some countries. Confirm rules locally, then include it correctly when you file crypto taxes.

Endnotes

Filing crypto taxes becomes manageable when you stay organized, use reliable tools, and follow a clear plan. Whether you use TurboTax, government portals, or manual spreadsheets, accuracy is what matters most. But for effortless, compliant, and accurate results, cryptact stands out.

cryptact simplifies every step of crypto tax filing. It automatically tracks transactions, calculates gains and losses, and generates compliant reports you can trust. Stay confident, accurate, and audit-ready with cryptact—the smarter way to handle crypto taxes. Choose a tool like cryptact and make your tax filing journey simpler!