Fact-checked and reviewed by Kshitij Shah (BitNine), Chartered Accountant.

AIS has made crypto tax reporting in India more visible than it used to be. Many users first notice this when they open the portal and find exchange-related entries, TDS traces, or transaction values that do not neatly match the numbers they planned to show in their return.

That mismatch usually does not mean the tax portal is “wrong” in a simple sense. It often means different systems are reporting different pieces of the same crypto activity. One source may be showing gross transfer value. Another may be showing only a taxable gain. Your own exchange export may include internal transfers, fee deductions, or reversals that AIS does not explain clearly on its own.

This is why crypto AIS mismatch India issues are becoming a real compliance topic. If your AIS, Form 26AS, exchange records, and ITR do not line up, the problem can snowball into a defective return risk, TDS credit mismatch, or unnecessary notice anxiety. The good news is that most mismatches can be understood and cleaned up once you know what AIS is actually showing and where VDA reporting is supposed to sit in the return.

Key takeaways

- AIS is broader than Form 26AS. From AY 2023-24 onward, Form 26AS mainly shows TDS and TCS data, while AIS shows a wider set of financial information.

- Crypto-related entries can appear because the tax department receives transaction-linked information and because TDS under Section 194S leaves a visible trail.

- An AIS mismatch does not automatically mean your return is wrong. It often means the reported value, gross receipt value, and taxable income value are being confused.

- For VDA reporting, the Income Tax Department expects transaction-wise disclosure in Schedule VDA in ITR-2 and ITR-3.

- The department’s defective-return FAQs indicate that the value of sale consideration disclosed in Schedule VDA should not be lower than the gross receipts reflected against TDS under Section 194S in Form 26AS.

- AIS feedback exists for a reason. If the exchange-reported information is duplicated, incomplete, or wrongly attributed, you can submit feedback and AIS will show both reported value and modified value.

Read more: For a full overview of how crypto is taxed in India, see our complete guide to crypto tax in India.

Table of contents |

No credit card required

Why crypto exchange data shows up in AIS

The first thing to understand is that AIS is not just a duplicate of Form 26AS. The Income Tax Department says AIS gives a comprehensive view of taxpayer information, while Form 26AS now mainly shows TDS and TCS related data from AY 2023-24 onward. AIS also lets the taxpayer submit feedback, and it shows both reported value and modified value after feedback is considered.

For crypto users, that matters because exchange-linked data can reach the department through more than one path. The most obvious one is Section 194S. If tax was deducted on a VDA transfer, that TDS footprint can show up in the system and later interact with your return disclosures. The department’s own defective-return FAQ says that where a taxpayer has VDA income, the value of sale consideration shown in Schedule VDA should not be lower than the gross receipts reflected against TDS under Section 194S in Form 26AS.

So if your exchange data appears in AIS, that is usually not random. It is often the system reflecting that some part of your crypto activity has already been reported to the department in a way that can be cross-checked against your ITR.

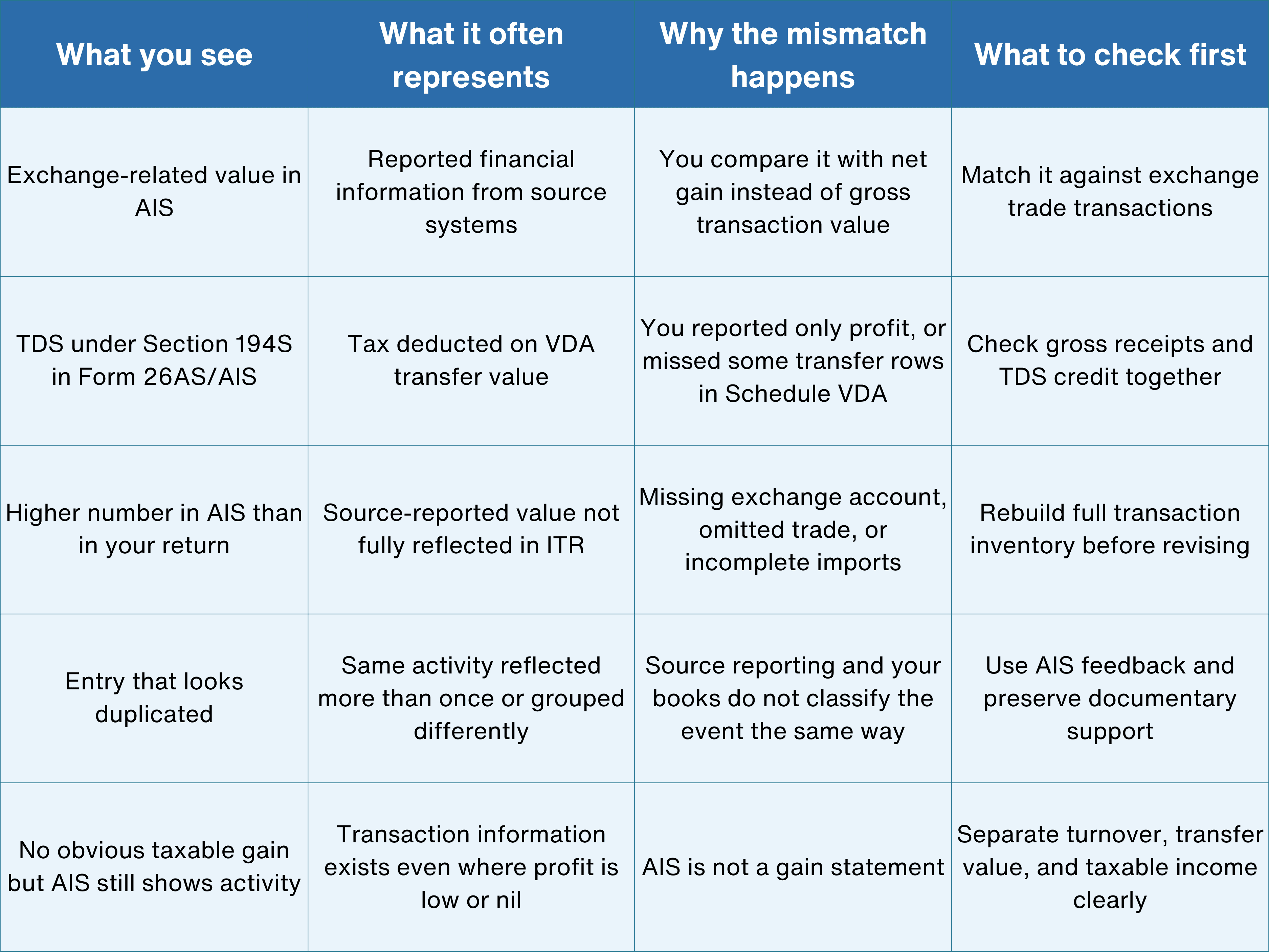

What usually causes an AIS mismatch

In practice, most mismatches happen because taxpayers compare numbers that were never meant to be identical.

A gross transfer value under Section 194S is not the same as taxable profit. A deposit into your exchange account is not the same as income. A sale value is not the same as net gain after cost. Internal wallet movements can also muddy the picture if the exchange statement and the tax return are not being read with the same logic.

The mismatch also gets worse when users rely on one exchange export and ignore the rest of the trail. Crypto tax reporting in India now sits inside a more structured return framework. The department’s ITR-2 FAQ says there is a separate Schedule VDA in ITR-2 and ITR-3 where VDA income is disclosed transaction-wise. Validation rules also tie Schedule VDA to Schedule CG, which means the numbers are expected to reconcile within the return itself.

So the real issue is usually not “AIS versus exchange.” It is “gross reported information versus properly reconciled tax reporting.”

The one table that makes the issue easier to read

That is why AIS mismatch work has to begin with classification. Until you know whether a number is gross receipt, sale consideration, TDS-linked amount, or actual taxable income, you are comparing the wrong things.

How Schedule VDA, AIS, and Section 194S connect

This is the part most users need to get right before they even think about filing.

The Income Tax Department’s ITR-2 FAQ says VDA income is disclosed transaction-wise in Schedule VDA in ITR-2 and ITR-3, and taxed at the special 30% rate under Section 115BBH. The department’s validation materials also say the VDA total in Schedule VDA must tie back to the VDA income shown in Schedule CG.

On top of that, the department’s defective-return FAQ for AY 2024-25 indicates that, in case of a mismatch between the gross receipts or TDS-linked values reflected in Form 26AS and the disclosures made in Schedule VDA, the return may be treated as defective under section 139(9).

That is the key compliance link. AIS and Form 26AS are not replacing your books. They are pressure-testing your books.

A simple example shows why this matters.

- Suppose your exchange deducted TDS under Section 194S on transfers totaling ₹12 lakh during the year.

- Your actual taxable VDA gains after cost may be far lower than ₹12 lakh.

- But if your Schedule VDA sales consideration or related gross receipt trail is incomplete, the system may read your return as under-reporting relative to the TDS footprint.

The answer is not to report ₹12 lakh as taxable gain if that is not the real number. The answer is to make sure your transaction-wise Schedule VDA disclosures and supporting records explain why the sales consideration reflected for VDA reporting and the net taxable income are different.

A practical way to fix mismatches before filing

The cleanest way to fix a mismatch is to work backwards from the portal data, then rebuild the tax file from source records.

Start with these steps:

- download AIS and Form 26AS for the relevant year

- identify the entries that appear crypto-related

- pull complete transaction history from every exchange and wallet used

- isolate gross transfer value, sale consideration, TDS, and actual profit or loss

- reconcile missing trades, duplicate imports, internal transfers, and fee differences

- rebuild Schedule VDA transaction-wise before touching the ITR

This matters because AIS lets you submit feedback, and the official AIS FAQ says that after feedback is submitted, the portal will show both reported value and modified value. It also provides an acknowledgement trail and activity history.

So if a crypto-related AIS line is clearly duplicated, wrongly attributed, or not matching the underlying facts, you should not ignore it. Review it, document the reason, and use the feedback mechanism where appropriate.

What you should not do is this:

- file using only the exchange’s tax summary without checking Form 26AS

- assume AIS equals taxable gain

- assume TDS credit alone proves the return is complete

- ignore small exchanges or old accounts because “the main one is already imported”

What to do if you already filed with wrong numbers

If you have already filed and then notice that AIS, Form 26AS, and your VDA return disclosures do not line up, do not rush straight into a random correction.

First rebuild the correct transaction file. Then compare:

- Schedule VDA sales consideration

- Section 194S TDS reflected in Form 26AS

- AIS reported values

- your claimed TDS credit

- your actual transaction-wise gain computation

Only after that should you decide whether a revised return is needed.

This is especially important because the department’s VDA defective-return guidance is focused on matching the reported income trail to the 194S-linked gross receipts. If the return side is incomplete, the risk is not only a small mismatch. It can also become a formal defect issue.

How cryptact helps

AIS crypto mismatch work is really a reconciliation problem before it becomes an ITR problem.

You may know the law well enough. The difficulty is building one coherent record from exchange data, wallet movements, TDS traces, and transaction-wise VDA reporting. That is where cryptact helps in a practical way. It brings exchange and wallet records together, makes it easier to review gross receipts against actual gains, and helps you prepare cleaner Schedule VDA data before filing.

For Indian users dealing with AIS mismatch issues, the biggest value is usually not “automation” in the abstract. It is having one place to understand why the number in AIS looks different from the number you were about to put into the return.

Conclusion

A good AIS crypto reporting India workflow starts with one simple rule: do not compare raw portal numbers with tax-return numbers until you know what each number actually represents.

AIS may show source-reported information. Form 26AS may show Section 194S TDS. Your ITR needs transaction-wise Schedule VDA disclosure. Those 3 things are connected, but they are not always the same number. Once you separate gross receipts, sale consideration, TDS, and taxable income, most mismatches become easier to fix.

That is where cryptact adds real value. It helps turn scattered exchange records into a usable VDA reporting file, so you can reconcile AIS against your own books, clean up mismatches before filing, and reduce the risk of defective-return issues later.