Fact-checked and reviewed by MetaCounts.co, a Vancouver-based cryptocurrency accounting firm staffed by Chartered Professional Accountants (CPAs)

Understanding how tax rules affect your crypto trades can save you money and headaches! When you sell an investment at a loss, tax rules may stop you from buying it back right away just to claim that loss. In the United States, this is called the wash sale rule. It blocks a loss deduction when you sell a stock or security and then buy the same one within a short window of time.

So, does the wash sale rule apply to crypto in Canada? Well, Canada uses a different system. The Canada Revenue Agency (CRA) generally treats crypto as property. Depending on your facts (for example, the frequency and nature of trading), gains and losses may be treated as capital or as business income. When treated as capital, the superficial loss rule applied. This rule could deny a loss if you buy the same crypto within 30 days before or after the sale and you still hold it 30 days later. There is no separate crypto wash sale rule. The same capital rules apply across all property, including digital assets.

In Canada, what many investors refer to as the “wash sale rule” or “crypto wash sale” is actually governed by the CRA’s superficial loss rule. Throughout this article, we use these common terms for clarity, but the tax treatment is based on Canada’s superficial loss provisions.

Canadian investors must track their gains and losses using the adjusted cost base (ACB) method. This method averages the cost of all units you hold for each crypto asset. Each time you buy or sell, your average cost updates.

The wash sale crypto rule 2025 may sound complicated, but don’t worry. This guide will break down for you. Read on!

Table of contents |

How the Superficial Loss Rule Works

Knowing when a loss is allowed or denied is the foundation of smart tax planning. Canada’s superficial loss rule plays a role similar to a wash sale rule. It prevents you from claiming a capital loss if you quickly rebuy the same crypto.

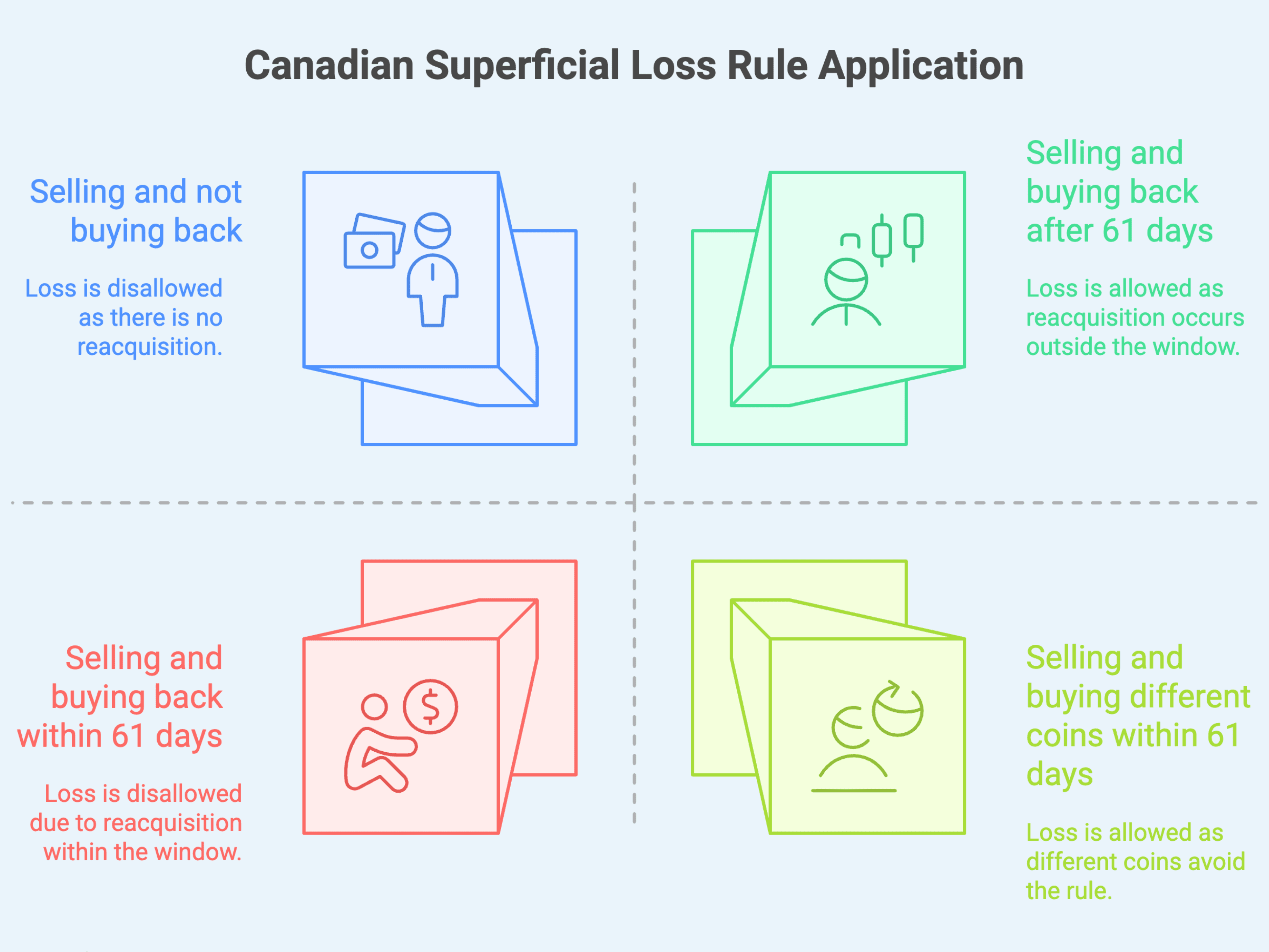

The rule says that if you or an affiliated person buy the same or identical cryptocurrency within 30 days before or after you sold it at a loss and still own it 30 days after the sale, then you cannot deduct the loss on your tax return.

An affiliated person includes you and your spouse or common-law partner. It can also include a corporation you or your spouse controls, a trust where you or your spouse is a majority beneficiary (such as an RRSP or RRIF), and a partnership where you own a majority interest. Trades involving these parties can trigger the superficial loss rule.

Instead, the denied loss amount is added to the adjusted cost base of the coin you repurchased.

Key Points of the Canadian Superficial Loss Rule

It applies to identical coins or tokens. (Buying a different cryptocurrency generally avoids the rule.)

The 61-day window runs from 30 days before the sale to 30 days after the sale. If you or an affiliated person buys the same cryptocurrency during this period and still owns it at the end of the 30th day after the sale (that is, on day 31), the capital loss is considered superficial and is denied.

If triggered, the capital loss is disallowed for tax purposes. Instead, that loss is tacked onto your new coin’s cost base. (You effectively get the benefit later, when you finally sell the new coin.)

For example, if you sell 1 BTC at a $1,000 loss (originally purchased for $11,000, sold for $10,000) and buy it back 10 days later for $10,000, the CRA denies the $1,000 loss. However, the $1,000 is added to your new Bitcoin's adjusted cost base (ACB), making your new cost basis $11,000 (not $10,000). Later, when you sell this Bitcoin for $15,000, your capital gain will be $4,000 ($15,000 - $11,000), not $5,000. The key point: the superficial loss isn't permanently lost. It's deferred until you eventually dispose of the cryptocurrency.

Avoiding Superficial Losses

To legitimately claim a loss, don’t repurchase the same crypto too soon. The simplest approach is to wait 31 days before rebuying the same coin. If you need market exposure sooner, you can buy a different asset in the meantime.

For example, sell Bitcoin and buy Ethereum or a stablecoin. As long as it’s not the same cryptocurrency, you won’t trigger the rule. After the 30-day period, you can buy back the original coin if you wish, to account for any Bitcoin wash sale rules (the CRA’s superficial loss rule).

Additionally, bear in mind that crypto wash trading is different from superficial losses or wash-sale tracking. Wash trading involves repeatedly buying and selling the same crypto to manipulate prices or trading volume, and it may be illegal.

Lastly, remember the CRA requires you to keep detailed records of every crypto transaction (dates, amounts, CAD values, etc.). They may ask for proof of your reported gains or losses.

Adjusted Cost Base (ACB) and Record-Keeping

As you know now, tracking every purchase and sale accurately is crucial to stay compliant. You must include all purchase fees and recalculate the average cost with each buy.

For example, if you bought 3 ADA over time for a total of $3,000, your ACB per ADA would be $1,000. Selling one would use that $1,000 cost base to determine the gain or loss. Using proper tracking helps you avoid wash sale crypto issues and ensures compliance with the crypto wash rule (the CRA’s superficial loss rule). The CRA expects your capital gains on Schedule 3 to be calculated based on this ACB method.

Maintaining ACB by hand can be tedious, especially if you trade often on multiple platforms. This is where crypto tax tools can help. Crypto portfolio and tax software can import your transaction history from all exchanges and wallets and compute gains/losses automatically.

For instance, cryptact is a leading tool that pulls data from all your exchanges and wallets into one platform, then calculates your ACB and profit/loss. Using such a tool, you can quickly see realized gains and losses, track your running cost base, and even spot suspicious patterns (like potential wash/superficial trades).

Tips for record-keeping and tracking

Log every trade: Keep a spreadsheet or use software to record dates, crypto type, amounts, CAD value, and transaction fees for each buy/sell.

Consolidate data: If you have multiple wallets/exchanges, consider a portfolio tracker or tax tool. These can import CSVs or connect APIs to gather all your crypto transactions in one place

Watch the 30-day rule: Flag the trades which fall within the superficial-loss window. Review your trades before filing.

Save documentation: Keep receipts, exchange statements, and records of fees for at least six years, as CRA requires. Failure to do so might result in a wash sale penalty on crypto.

Keeping up with multiple wallets and trades can get complicated without the right help. So, using a crypto tax platform can greatly reduce errors and save time.

For example, cryptact’s free plan supports average cost and can aggregate up to 100,000 transactions. Automating calculations, these tools help ensure your cost basis and superficial-loss adjustments are handled correctly, which is especially valuable if you trade frequently.

Planning Your Trades Around Superficial Losses

Smart planning can help you maximize deductions while staying within the rules.

Canadian crypto investors can use capital losses to offset gains (but remember only 50% of the loss is deductible, matching the 50% inclusion rate for gains). Losses can be carried back up to three years or carried forward indefinitely on your tax return. However, don’t let “gotcha” rules slip through: if you sell to harvest a loss, avoid rebuying the same crypto for 30 days, or switch into a non-identical asset during that period.

In summary: the superficial loss rule means you might have to adjust your tactics when doing tax-loss harvesting. Ensure you genuinely dispose of the asset for the loss to count. Keep in mind that any denied loss will simply inflate your ACB, so you eventually recoup it when you sell again (albeit later).

Conclusion

Is there a wash sale rule for crypto? In Canada, crypto investors need to remember that while there is no special crypto wash sale rule, losses are still governed by the superficial loss rule. Selling a token at a loss and buying it back within 30 days before or after the sale (by you or an affiliate) disallows the loss and adds it to your new cost base. Careful timing is very important. So, wait 31 days after the sale or switch to a different asset to capture losses properly.

Thorough record-keeping is essential to comply with CRA rules, especially for tracking your adjusted cost base. Many investors use cryptact, which can automate profit/loss tracking, flag potential wash sale crypto situations, and simplify calculations of gains and losses. With cryptact, Canadian crypto traders can easily manage their portfolios, avoid wash sale crypto issues (i.e., superficial loss issues), and stay organized for accurate reporting.